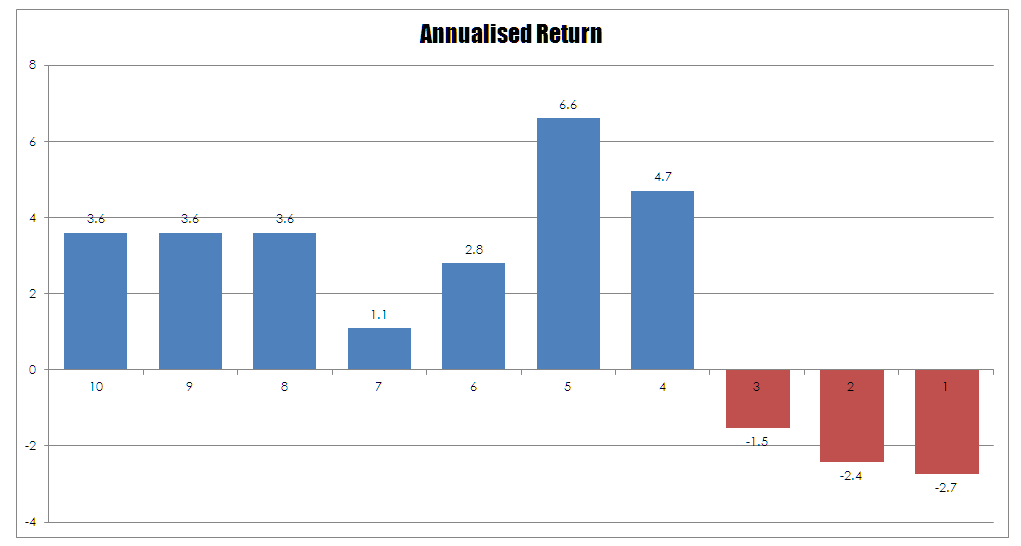

When I was banging on about EFT’s last week I made the point in passing that when you are looking at trading systems that the start date is everything and it is the point at which most of the fudging of results occurs. As an example I took a hypothetical passive system and began to change the starting date of the system to highlight this problem. The chart below shows a series of start dates counting down from ten years ago to today. So if I had started this system and traded it for ten years its annualised return would be 3.6%. Whereas if I had started the system seven years ago my annualised return would only be 1.1%. As you can see changing the start date changes the annualised return that is generated by the system. The worst returns have occurred in recent times with the best being five years ago. It doesn’t take much to work out which you might include in your marketing material if you wanted to cast yourself in the best light. This problem can occur on even shorter time frames such as moving the start date from one month to another.

As you can see changing the start date changes the annualised return that is generated by the system. The worst returns have occurred in recent times with the best being five years ago. It doesn’t take much to work out which you might include in your marketing material if you wanted to cast yourself in the best light. This problem can occur on even shorter time frames such as moving the start date from one month to another.

The problem is also has nuance that catches the unwary; annualised returns are simply a nonsense measure when viewed in isolation because of problems with the construction of averages. For example imagine you invest $100,000 in a fund that in the first year generates a 100% return and then in the second year losses 50%. How much have you made, if you were to a look at the yearly average return you would calculate that 100%-50%/2 = 25% and the fund manager could rightly claim to make this average figure. However, your true return which is the only one that matters is zero.

True returns are given by an equity curve with as much data as possible – this gives you some idea of the trajectory of an account under a variety of conditions. This is then supplemented by looking at the drawdown curve of the system to give you an idea of how rough the ride. So for our hypothetical system above if I take the start date of 10 years ago I get an annualised return of 3.6% but a maximum drawdown of 44.5% because the system is caught by the GFC and being passive it takes no defensive action. Yet if I take our preferred kick off date of five years ago I get a drawdown of only 20.8%. So my system at this point has nearly twice the annualised return and half the drawdown. Yet the ten year figure is the more complete since it also includes a global shock so it shows the true performance of the system whilst under pressure.

This leaves us with the problem of how to deal with this in a real world situation where this data might not be forth coming. Fortunately we can reduce this problem to a simple rule. If a system does not immediately show a drawdown or has a smooth equity curve something is not right.