As we weather the COVID-19 storm thoughts invariably turn to what life will look like after the storm passes and as luck would have it there is no shortage of economists to tell us what life will be like. Most of their prognostications seem to fall somewhere between being the last person on the Titanic or rewind of the Great Depression. Either alternative sounds mighty unpalatable. However, before being overwhelmed by the emotional contagion that these sorts of scenarios are bound to generate let’s consider the forecasting ability of people involved in the finance industry. As the often overused quote by economists Paul Samuelson goes – the stockmarket has predicted 9 of the past 5 recessions. My guess is that the finance industry, in general, would kill for such accuracy. My experience has been that the majority of financial predictions of any sort over any market and any time scale are profoundly inaccurate, in fact, a lack of accuracy is the default position.

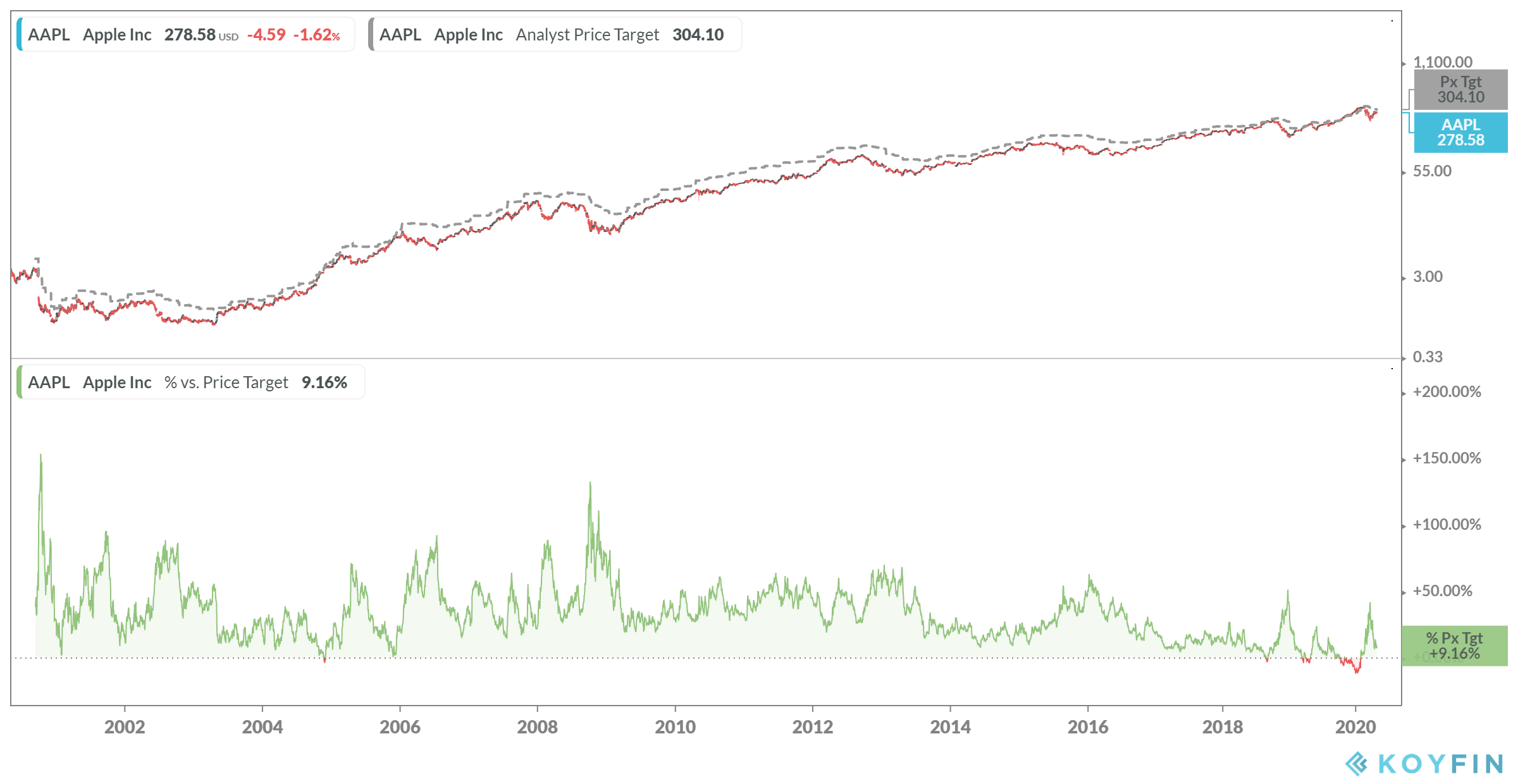

As a micro example consider how stock analysts do in their predictions of such mundane things as price targets. The chart below shows the consensus price targets generated by analysts for Apple – I chose Apple because it is probably the worlds most widely covered stock. Thousands of analysts around the world pore over every detail of the company as such you would think that this level of detail combined with the now somewhat mythical wisdom of the crowds would do a reasonable job at predicting the stock price. You would, of course, be wrong.

You will note that the targets are generally wildly optimistic – very rarely do they undershoot the actual price. This feature demonstrates two important things about what a forecast represents. As a first-order consideration it represents the internal bias of the people making the forecast. My guess is that your average Apple analyst is a fanboi or girl who slobbers over every new thing that the company produces and views every single thing about the company through rose coloured glasses. Predictions are generally a function of bias, not data. This highlights the fact that data is not some robotically generated consideration – information flow is lumpy it is not frictionless it is therefore imperfect.

You will note that the targets are generally wildly optimistic – very rarely do they undershoot the actual price. This feature demonstrates two important things about what a forecast represents. As a first-order consideration it represents the internal bias of the people making the forecast. My guess is that your average Apple analyst is a fanboi or girl who slobbers over every new thing that the company produces and views every single thing about the company through rose coloured glasses. Predictions are generally a function of bias, not data. This highlights the fact that data is not some robotically generated consideration – information flow is lumpy it is not frictionless it is therefore imperfect.

This places the notion that economists know what will happen post COVID-19 into some form of context – the context being that they don’t have a clue. My perception is that no one will know until we get a clear view of post lockdown life in the rear vision mirror – hindsight is the prefect prediction tool. Until then the only guide you have is what is actually happening not ideas about what should happen. And as the quote often attributed to Niels Bohr the Nobel Prize winning physicist goes – Prediction is very difficult, especially if it’s about the future.

But Mark Twain is also attributed with saying “history doesn’t repeat itself but it often rhymes”. There are definitely things to be learned from the past, but defining which and what they are remains an overarching impossibility. HIndsight renders my vision perfect. And Philip Tetlock has completely reprogrammed my thinking about forecasting. Thanks for that recommendation Chris.

In terms of trading a stock index such as the XJO, the best compromise is to use a reactive real-time relatively simple trend following method. It could be a 9 and 21-EMA dual crossover system on a daily chart. Such a system would have told the trader to exit the XJO on February 26, 2020, and stay in cash until the next crossover buy signal is indicated. This simple trading system completely does away for any media news, COVID-19 data, or analyst forecasts. Always taking the chart signals when presented is the key to success. The stock market always looks forward, and this is reflected on a share price chart.

Excellent Chris.

Thanks

Classic Tate. Love it.