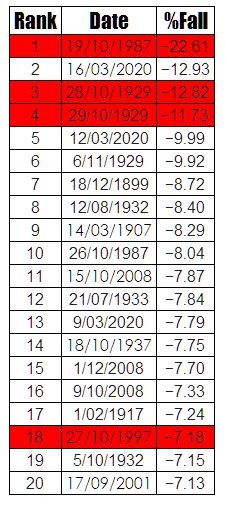

As October approaches once again we begin to see in the press the usual moaning and wailing about the impending implosion of the market and not doubt as October gets closer and closer this gnashing of teeth will reach a crescendo. October occupies a singular fascination for the ill-informed courtesy of two events – the crashes of 1929 and 1987. In fact, the fascination revolves around three trading periods only, what is even more intriguing is that people base their trading philosophy and emotional state on these three outlier trading days. In the table below I have highlighted the worst single-day percentage losses experienced by the Dow.

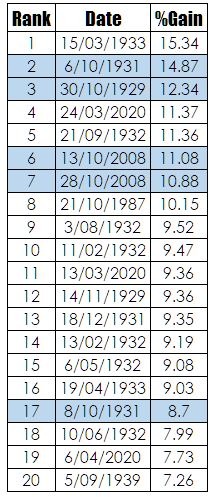

As you can see four of the top 20 worst days performances were in October and three of the worst days appear at the top of the table. It is these days that traders base their expectations for October upon. However, there is also more than one side to the data you generate. Below are the best day performances of the Dow.

Two of the top three performing days occurred in October and 20% of all top-performing days are in October. The focus upon the worst performing days says a lot about both trader psychology and the emotional lack of preparation that traders have for the fact that markets sometimes go down. Since I had Excel open I thought it would be interesting to actually have a look at what the monthly returns going back 100 years are for the Dow. You will notice that I have switched focus from daily moves to monthly. I have done this for two reasons. If your trading is dependant upon a single day then you don’t have a trading system and trading is an on average over time profession. That means it takes time.

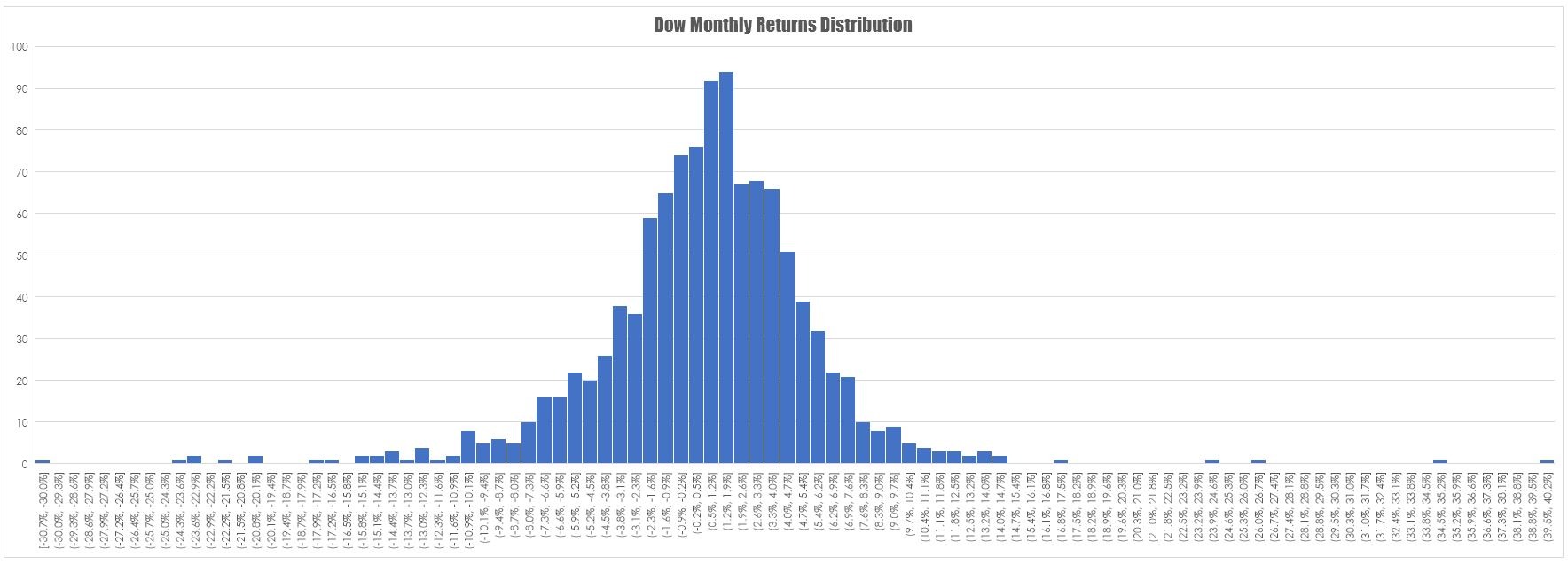

The distribution of monthly returns for the Dow is shown below.

As you would expect you get a very familiar looking curve with values clustered around -2% and +2% return for any given month. Outliers are few and far between yet it is the outliers that traders anchor to. It is worth looking into the nature of negative returns to see if there is actually any evidence of October being a bogey month as opposed to simply three bad trading sessions. In the table below I have collected the top 10% of poor monthly trading sessions on the Dow dating back to 1914. I have highlighted the Octobers in red.

As you would expect you get a very familiar looking curve with values clustered around -2% and +2% return for any given month. Outliers are few and far between yet it is the outliers that traders anchor to. It is worth looking into the nature of negative returns to see if there is actually any evidence of October being a bogey month as opposed to simply three bad trading sessions. In the table below I have collected the top 10% of poor monthly trading sessions on the Dow dating back to 1914. I have highlighted the Octobers in red.

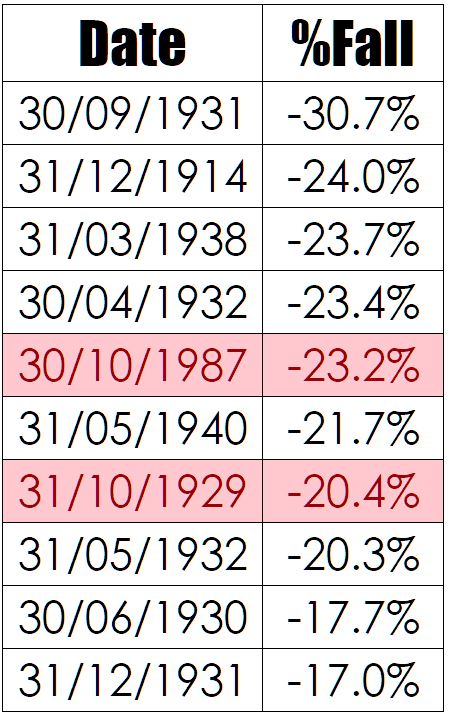

At first glance, it seems as if there is a lot of red in the table thereby confirming the original bias that October is a poor month for markets. However, all I have done is highlight dates and not the quanta of the actual move. A slightly different picture arises when I mark up the data for all falls over 10% as per the table below. In the table below those falls over 10% that occur in October are still marked in red, those falls over 10% that occur in other months are marked in yellow.

At first glance, it seems as if there is a lot of red in the table thereby confirming the original bias that October is a poor month for markets. However, all I have done is highlight dates and not the quanta of the actual move. A slightly different picture arises when I mark up the data for all falls over 10% as per the table below. In the table below those falls over 10% that occur in October are still marked in red, those falls over 10% that occur in other months are marked in yellow.

The intensity of the first chart begins to fade when the size of the fall in any given month is included. Interestingly when I looked at the most frequently occurring month in the top 10% of all down months that I had available it was September. I decided to further slice the data just to see what the top 10 drops were and got the following table.

The intensity of the first chart begins to fade when the size of the fall in any given month is included. Interestingly when I looked at the most frequently occurring month in the top 10% of all down months that I had available it was September. I decided to further slice the data just to see what the top 10 drops were and got the following table.

The astute will notice that October occurs twice in this list but so too does May and December but nobody gets themselves into a twist about those two months. My feeling about October is one of total ambivalence in part because I don’t see anything special about it in the data as opposed to the superstition and it is just another trading period that I have no control over whatsoever. The market will do what it wants to do with or without me involved. But there is a final point I want to repeat and that is that trading is an on average over time profession. I come back to the statement that if you base your trading philosophy or career on three outlier periods in history then you will probably find this job quite stressful and unrewarding.

The astute will notice that October occurs twice in this list but so too does May and December but nobody gets themselves into a twist about those two months. My feeling about October is one of total ambivalence in part because I don’t see anything special about it in the data as opposed to the superstition and it is just another trading period that I have no control over whatsoever. The market will do what it wants to do with or without me involved. But there is a final point I want to repeat and that is that trading is an on average over time profession. I come back to the statement that if you base your trading philosophy or career on three outlier periods in history then you will probably find this job quite stressful and unrewarding.