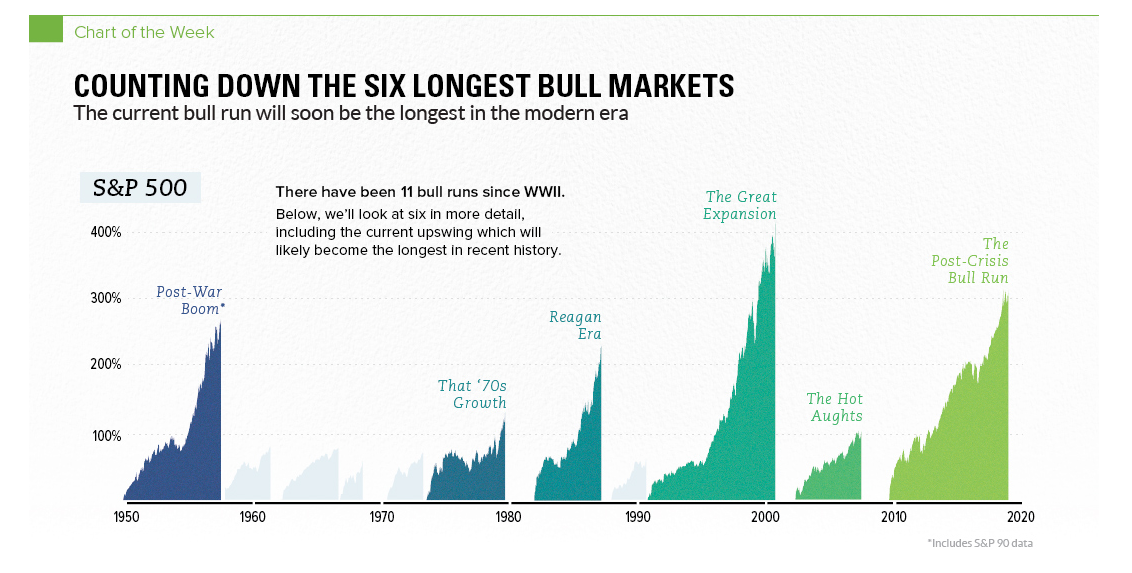

One of the things that has always fascinated me about technical analysis is the capacity of people to argue over the irrelevant. I am quite certain there are blokes in little clubs all over the world arguing that the RSI should be set to 12 and not 9 because that makes all the difference. It is as if such minutia was relevant to anyone at all – it is obviously relevant to them but this raises the accessory question of do they matter and who really cares. On this theme I have noticed that the current argument going on seems to revolve around the age of the US bull market. This argument is centred around where you nominate the bull market to have started. Part of the catalyst for such as argument are charts like the one below by Visual Capitalist which attempts to put the current run into some form of historical context. I have only snipped out part of the graphic since it is huge, if you want to rest click here.

If I were to summarise the arguments around defining the starting point of a run they seem to fall into three camps. Some argue that the run begins the moment the previous bear market ends. Sounds logical but you only know that in hindsight. Others argue that it only begins when the market has advanced 20% from the low established by the previous bear market. Who decided that 20% was the benchmark, why not 10% or 19%. The final argument seems to rely upon the previous high before the bear market being surpassed before declaring it a bull market – this seems to leave an awful lot on the table before you get your arse into gear.

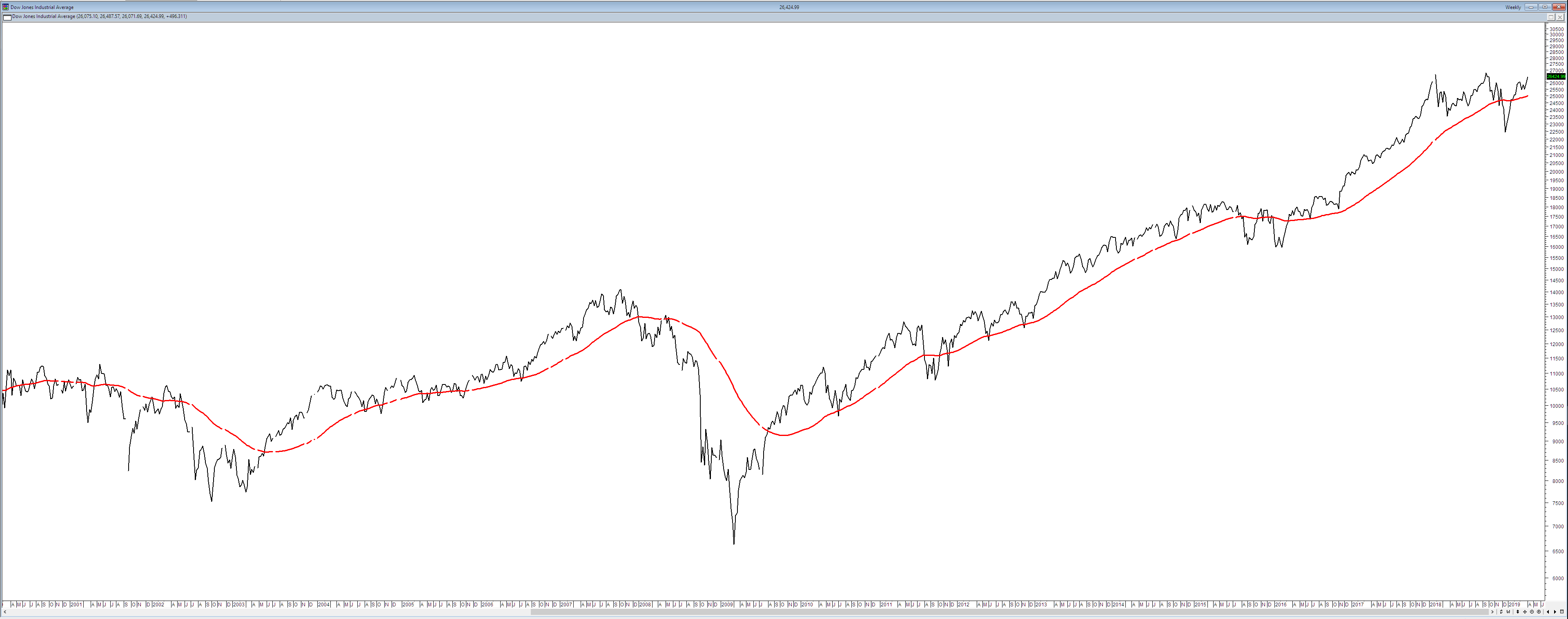

My point to all of this would be who cares when it began surely the salient point is to have a mechanism that tells when the trend has changed and whether that trend has widespread investor support. The rest is simply old men arguing over the irrelevant. As a simple mechanism consider the chart of the Dow below –

With the benefit of over a decade of hindsight it appears obvious that the market reversed in the period I have highlighted. But trading doesnt grant you the luxury of looking at charts and then making a decision about what you should have done ten years ago. I have already discussed at length the idiocy of such approaches. We cannot magically transport ourselves back int time and become a buyer of US ETF;s during that period and then just hang on a rake in the cash. The central problem to be solved is how to denote a change in trend – when do we know that the bears are now in charge?

The chart below has been converted to a line chart to remove some of the extraneous information from it and on it I have plotted a longer term moving average. Nothing magic, nothing proprietary – all I am attempting to do is to smooth out the information about the trend. Its not rocket science nor is it very innovative.

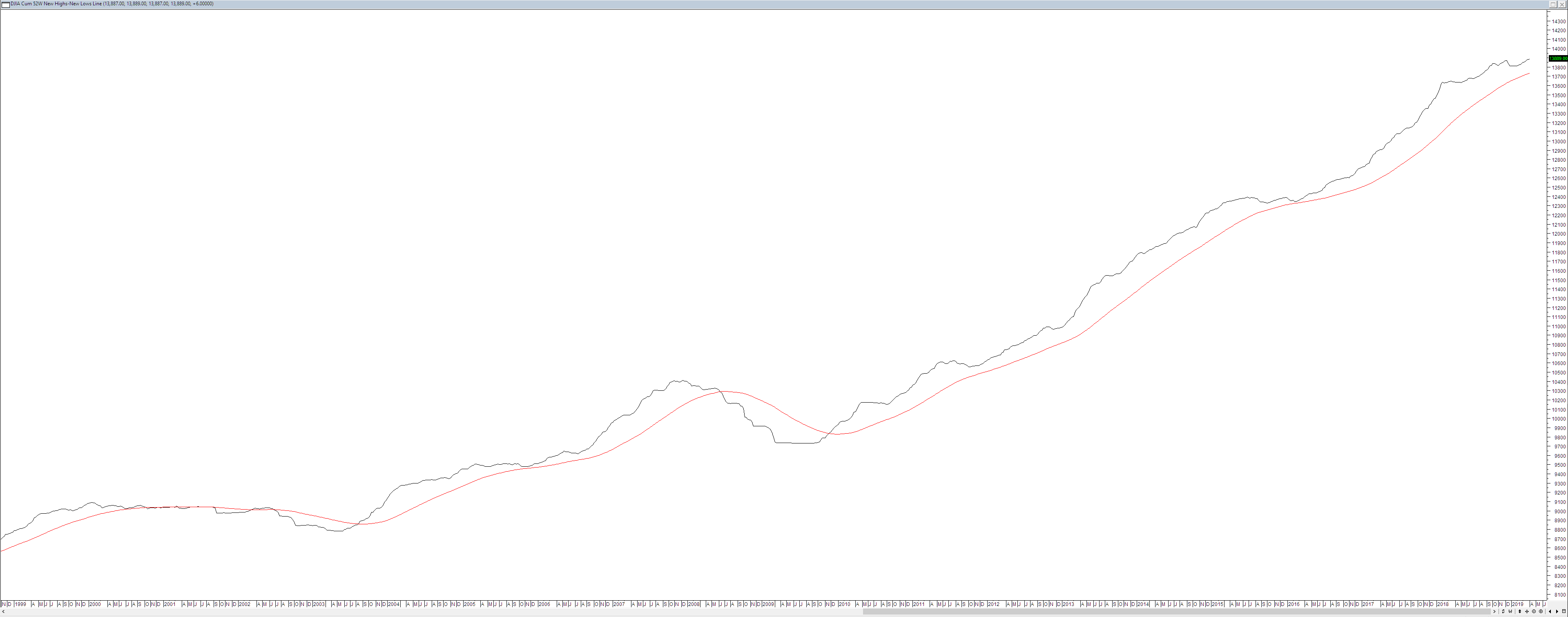

By reducing the amount of information we are receiving and removing our own judgement we now have a mechanism of defining whether the market is trending up or trending down. Note – it is not a mechanism for determining whether we are or are not in a bull market because I regard such arguments as simply stupid and irrelevant. It is nice for investor comfort to know that you have friends in the market but in reality it in no way should alter your decision making. We can try and make an estimation of the strength of this trend by looking at the number of stocks making new 52 week highs. This metric has long been accepted as a measure of strength and it does stand to reason that if the market is strong then you will have a lot of stocks making new highs. as shown below.

Interestingly it looks like a smoothed version of the price only chart and this is only logical. From this you can see when the market is perceived to be strong and by definition trending up.

If we have such metrics available and they are freely available, then why do we have people arguing over the irrelevancy of when the bull market began. I think there are a few reasons for this. First and foremost is that traders take comfort from labels – if you believe that we are in a bull market then all sorts of psychological pressure are relieved. In part you believe your job will be easier because there will be widespread investor involvement therefore there is greater perceived probability of things going up. If we can define things then we can understand them. There is also the belief that in bull markets making money is easier – a task most fund managers seem to fail at for a multitude of reasons. Finally because trading is an isolating profession I think people want to be part of a group and if you are participating in a bull market you are part of a group – there will be others to talk to and there will be an upswing in interest in your profession. All of sudden you are popular. However, these are just my guesses and I am not certain they are all that good. In reality I think people argue over the timing of the beginning of bull market for the same reason they argue over all things to do with the market. They cannot see the bigger picture nor understand the irrelevancy of themselves or their arguments. If you spend your day on internet forums arguing about certain indicators or tools or trying to generate the magic zero lag moving average (actually thats price but some people cannot be convinced of that) then you have missed the bigger question which is what reason do you have for being in the market. The question is quite simple are the conditions right for you to invest? When or if we are in a bull market is an irrelevancy.

Love your rants CT

They continue to demystify what you really need to understand about the markets to be able to trade (successfully). Removing the anal analysis from the decision making then gives the mental space to deal with the 80% factor of trading…which is our psychology