I find the notion of being a persistent short seller to be an interesting one. It is interesting because of the following reasons.

- Equity markets in particular have an upward bias.

- Short selling offers very limited profitability but theoretically unlimited risk. In this respect, it is similar to writing options.

- In times when short selling may offer above average profitability, it is often banned by regulators who mistakenly seek to lower overall market volatility.

- All the big money is made on the upside eg GME 52 week range $3.77 to $175.22

What is interesting is that despite all these factors against it traders and in particular professional traders persist in trading against the trend. This is why I found this quote particularly interesting.

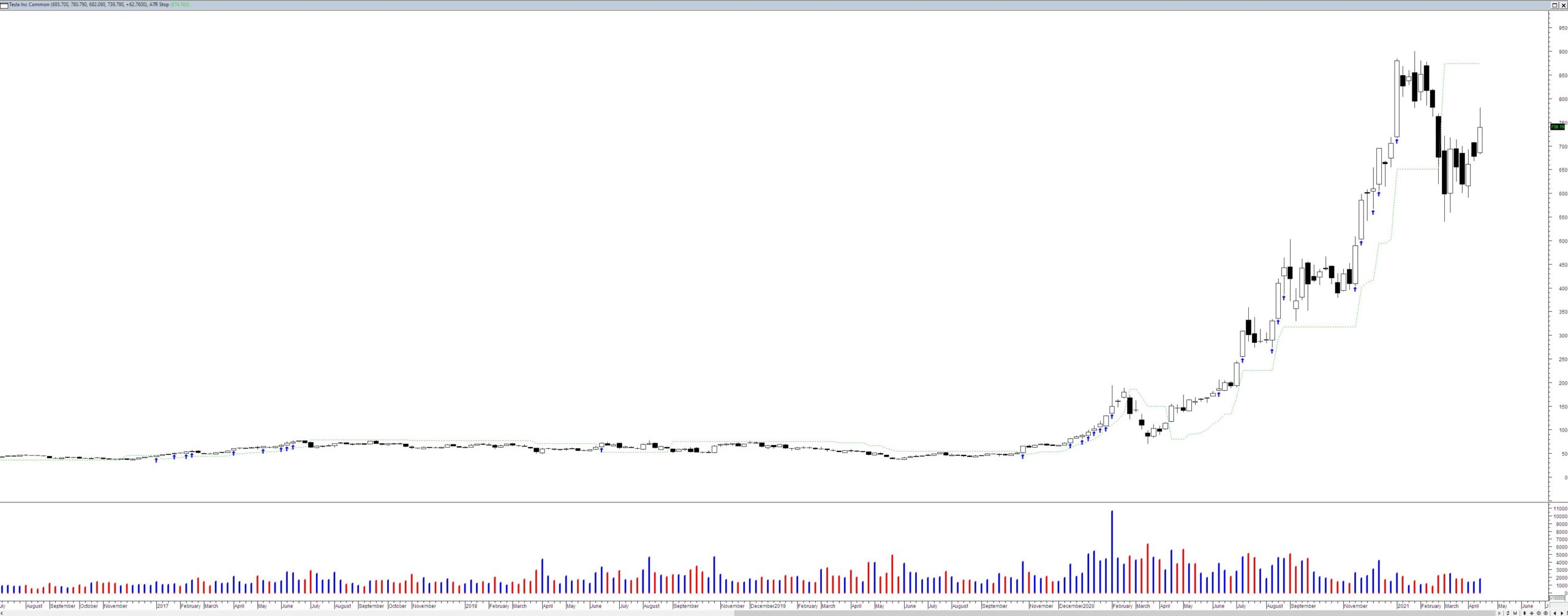

That said, last year Chanos’s most notable loss was his Tesla short. Elon Musk’s electric car company skyrocketed by more than 700 percent last year, and Chanos — long a Tesla foe — had to scramble.

In January he told CNBC the firm had transformed his short into puts — a common strategy when short sellers are forced to cover their stock shorts. (This year, Tesla is down, but by just 3 percent.)

Source – Institutional Investor

What this sort of thing reinforces in me is that trading is a psychological endeavor and little more than that – this notion of an ego-based concentration bet is interesting. It doesn’t matter what your personal opinion of TSLA is – you may think it is little more than a Ponzo Scheme that makes pretty ordinary cars but it is necessary to separate personal opinion from the utility of an investment for profit. I think the majority of crypto’s are absolute rubbish designed to separate idiots from their cash but it doesn’t stop me from appreciating the utility of a good trend.

And for those who dont follow TSLA below is a chart that covers the last five years. My guess is that Chanos shorted as it was rocketing up.