Apparently Australian Stock Report is circulating a petition to ban short selling. The rationale for this is as follows –

Recently, we have seen billions of dollars wiped from global and Australian equities markets in part due to the practice of Short Selling. This predatory trading technique is often executed in conjunction with algorithmic “bot trading” and has lead to the destruction of the hard earned savings of everyday investors, self managed super funds and retirees.

In particular, the big four banks (ANZ, CBA, NAB, WBC) have had their shares savaged by offshore short sellers which has directly impacted the large amount of Australian investors currently holding these companies.

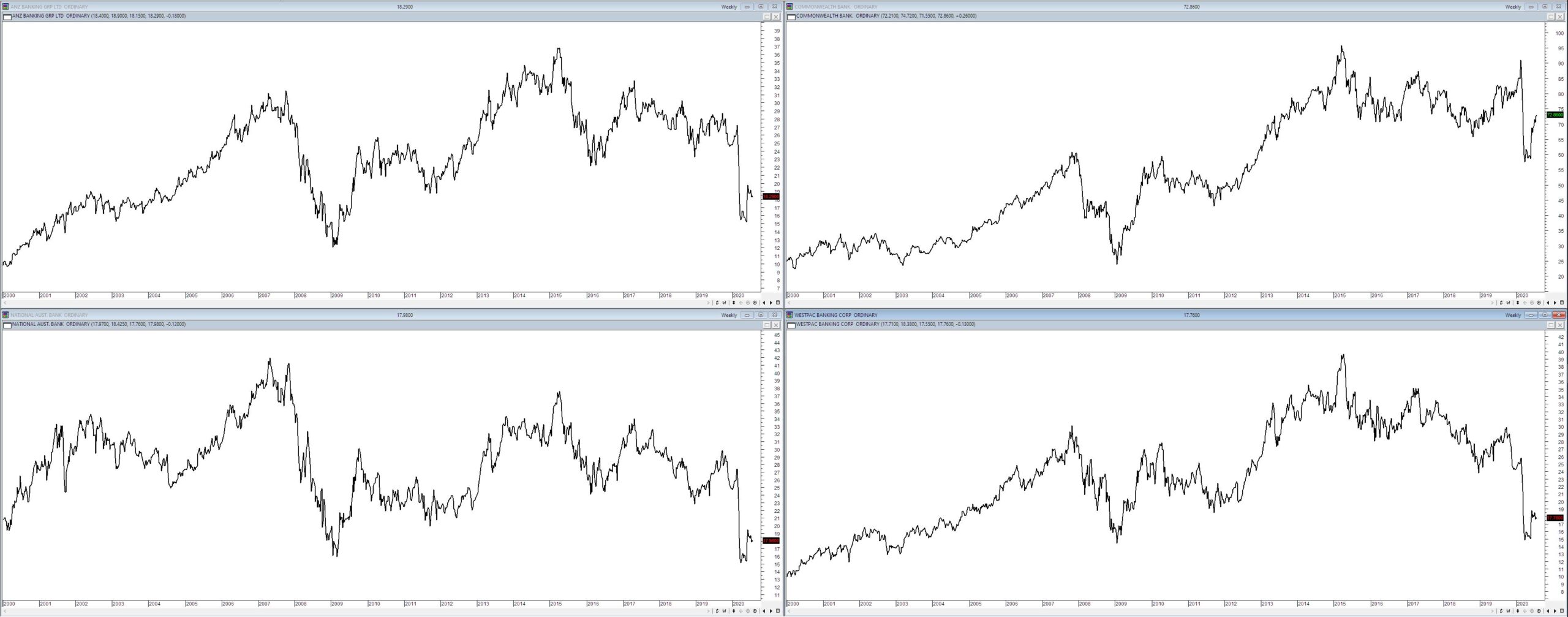

There are a few things to unpack in these first two paragraphs leaving aside the inflammatory tone and appeal to nameless shadowy forces preying on innocent investors. The point I want to concentrate on is the notion that the big four banks have been subject to relentless short selling that has driven down their prices. This seems to be the first point of error in their thinking – you cannot just wander into the market and start driving down the price of a given instrument. Short selling is already tightly regulated in the Australian market.It is instructive to look to have a look at the prices of the big four.

What is most obvious from this is the banks fall began in 2015 yet 2016 contain no such bleating about short sellers despite prices dropping substantially. In fact, if we zoom out further we see that only ANZ and WBC surpassed their pre-GFC highs.

This failure of the banks as a group to continually make consistent new highs post the GFC is as interesting as the fact that their prices peaked in 2015 and then fell sharply only to recover and then drift down in the case of ANZ, CBA and NAB. Only CBA was able to hold ground. This fact forms part of an interesting narrative around the banks.that in part revolves around the banks no longer being sacrosanct entities that were a guaranteed free ride for investors. Short selling plays no part in this narrative merely standard market forces where stocks move into and out of favour. And banks stocks are in no way immune from this behaviour. Big news for those complaining about short selling – stock prices go up and down. There is no law that says any stock must only ever go up.

The other point to note is the belief that short selling is rampant among the banks at present the following from marketindex.com.au shows the percentage of stock is noted as being short sold in the big four –

ANZ – 0.68%

CBA – 0.51%

NAB – 0.81%

WBC – 0.90%

As you can see this is hardly an overwhelming endorsement for the belief that strange mysterious forces at play deliberately seeking to impoverish your average investor. We can even look back in time at the top 10 most shorted stocks on the ASX.

Source – marketindex.com.au

During the Global Financial Crisis (GFC), we saw regulations introduced to ban the short selling of financial stocks to add stability to the financial system. Once the market stabilised and confidence returned we saw these short selling bans removed.

What is interesting in this statement is not that it is actually incorrect but rather at the bottom of the petition Australian Stock Report reference an ASIC article that states the following –

Report 302 Short selling: Post-implementation review (REP 302) also acknowledges that the measures may have contributed to some adverse market characteristics, such as reduced liquidity and increased price volatility. The measures also imposed compliance costs on many firms.

A note to people who put references in their pieces – you might actually want to read them first.

The moment short selling is banned the volatility within the market and individual stocks goes up and price discovery and liquidity go down. Both price discovery and liquidity are essential to a functioning market.

This agrees with findings from around the world.

We find no evidence that short‐sale restrictions provide support for stock prices or that they reduce volatility. Moreover, stocks subject to the short‐selling ban suffered a severe degradation in market quality. Controlling for the adverse effects of the financial crisis on markets, we show that short‐selling restrictions increase intraday volatility, reduce trading activity and increase bid–ask spreads.

Effect of the Ban on Short Selling on Market Prices and Volatility – Uwe Helmes, Julia Henker,Thomas Henker Accounting and Finance Vol.57,Issue 3,pp 727-757 2017

We find empirical evidence that the financial crisis was accompanied by an increase in volatility persistence and that this effect was particularly pronounced for those stocks that were subject to short selling constraints. We interpret this finding as evidence of a destabilizing impact of short selling constraints on stock returns volatility.

Contrary to the regulators’ intentions, financial institutions whose stocks were banned experienced greater increases in the probability of default and volatility than unbanned ones, and these increases were larger for more vulnerable financial institutions.

This mob used to have advisory services for investing, for trading and a few others.

They also used to within these services, advise recommend short selling. Go figure.

The number of recommendations were far to many for my portfolio to handle, so cherry picking left me in losing positions. Was advised to use much smaller position sizes which I did but after two years of losses decided to create my own plan and trade that. Finally in profit and with 6% up, I ceased my membership.

A few years on and they still try the sales spin to get me back. But I always counter that I am happy with my own independent results.

Looks like they are trying to reinvent themselves to get a better foothold in the market. Unfortunately the newbies like I was, will be drawn to them.

Between the royal commission and the fact that they are exposed so heavily to the real estate market while every one seems to be losing their job I think they would be quite capable of falling with or without that tiny amount of shorting