I do enjoy it when people email me to ask me about something they have read in the media. My enjoyment comes from the simple fact that I dont read business publications. I find them irrelevant, stupid, depressing and generally lacking in original thought. However, in the spirit of being polite I did take a look at this article from the Fairfax trash pile. The basic contention is that corporate earnings will go through the roof and that this will drive share prices through the roof. Implicit within any such article are two very basic assumptions and these assumptions are the foundations upon which this argument sits. At the heart of the piece is the assumption that analysts are capable of making accurate predictions regarding the direction of earnings. Secondly, it is assumed that perceptions of future earnings drive share prices.

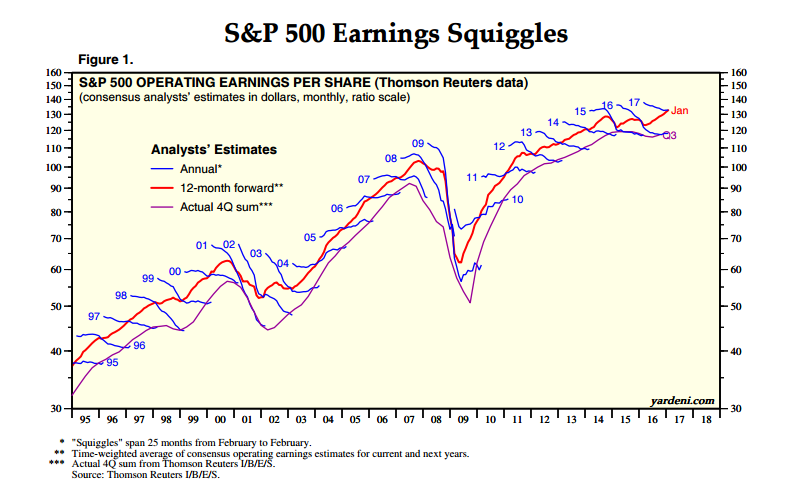

With regard to the former, the forecasting track record of advisors is poor with a tendency to consistently overestimate earnings as shown by the image below. Analysts are persistently in the grip of optimism bias when it comes to forecasting and this adversely impacts their ability to make any form of accurate forward judgement. This lack of ability is also clouded by the hubris involved in thinking that you can make an accurate prediction about anything.

Source – Dr Ed Yardeni

The psychology behind this incompetence is reasonably easy to understand once you understand the nature of the finance industry. This is the dont bite the hand that feeds you syndrome. Within the finance industry very little money is now made by the sell or advisory side of the industry. The big money has always been in corporate advising, that is restructurings, capital raising and the like. It is here that the fees total in the tens of millions of dollars. As such you dont want to offend companies that you might do very lucrative work for by telling everyone that their business is crap and that the company is run by people who would struggle to run a Mr Whippy van. It is much better to tell everyone that that the sun shines out of their proverbial and that everyone will get a free unicorn in the morning.

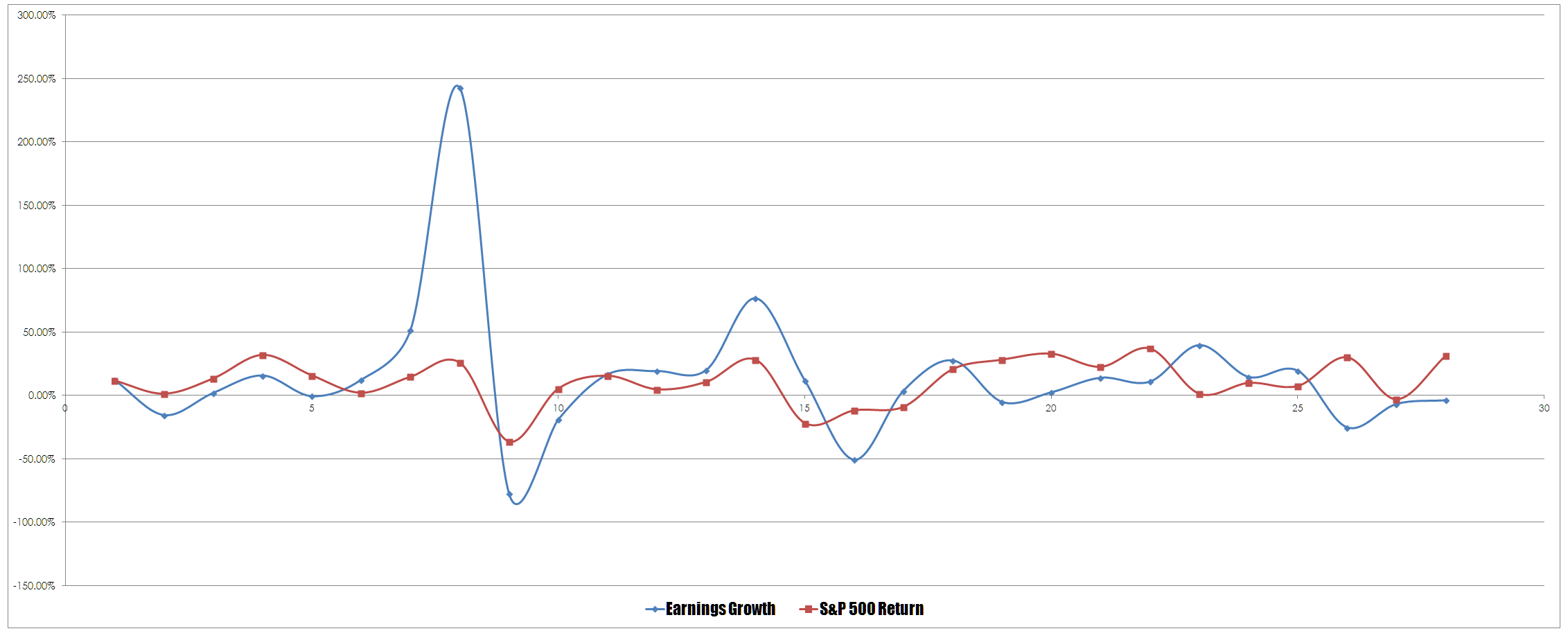

The second assumption is whether or not earnings drive share prices and this to my way of thinking is a more interesting problem since it moves into the realm of investor perception. To get a sense of this I looked at the year on year changes in earnings for the S&P 500 and compared that to the yearly return for the S&P 500 and plotted these initially in the form of a simple bar chart to get a sense of any form of relationship.

However bar charts dont really give a true sense of relationships or correlations so I plotted the data as a smoothed scattergram.

So the question is what do the squiggly lines tell me. They tell me that sometimes earnings growth and share prices move together and sometimes they dont and if I do a bit of dodgy stats-fu on my trusty old Casio I find that that changes in earnings and share price growth have a very weak correlation of 0.37. The reverse intepretation is that most of the time they dont share a relationship. But there are some caveats in generating correlations. The correlation I generated is what is known as a Pearsons correlation, this looks at the linear interdependence of variables and it can be affected by outliers such as we see in the rebound from the GFC. I also wonder about true independence between variables over time – my concern comes from the fact that markets seem to have memory and this in turn loops back to the impact of data on investor perceptions over time.

The wonderful thing about being a trader is that our perceptions and our benchmarks are very simple and they revolve around the idea of whether something can help us to make money. In this instance neither the faulty predictions of analysts nor their profoundly weak impact upon price movements convinces me that that either idea lives up to their hype.

What is “linear independence of variables?” Would the correlation of market sentiment with returns while taking in consideration of outliers be more accurate?

Pearson correlation – something new to learn. Thanks

It is an interesting thought. My concern would be how would I define market sentiment in a sufficiently robust way.