Lately my junk mail inbox has been inundated with bits and pieces regarding ethical investment. Every now and again it seems if the investing community goes on a bit of a tear and everybody plays follow the leader. Much of what I have been receiving is based upon a paper from last year – Foundations of ESG Investing which goes onto state how a concentration by a company on Environmental, Sustainability and Governance (ESG) factors might benefit both the company and shareholders. The authors postulate the following as mechanism by which this might be achieved. –

We examined how ESG information embedded within companies is transmitted to the equity market. Borrowing the language of central banks describing how monetary policy can affect asset prices and economic conditions, we created three “transmission channels” within a standard discounted cash flow (DCF) model. We call these the cash-flow channel, the idiosyncratic risk channel and the valuation channel. The former two channels are transmitted through corporations’ idiosyncratic risk profiles, whereas the latter channel is linked to companies’ systematic risk profiles.

These three transmission channels are based on the following rationales:

Cash-flow channel: High ESG-rated companies are more competitive and can generate abnormal returns, leading to higher profitability and dividend payments.

Idiosyncratic risk channel: High ESG-rated companies are better at managing company-specific business and operational risks and therefore have a lower probability of suffering incidents that can impact their share price. Consequently, their stock prices display lower idiosyncratic tail risks.

Valuation channel: High ESG-rated companies tend to have lower exposure to systematic risk factors. Therefore, their expected cost of capital is lower, leading to higher valuations in a DCF model framework

The point about these factors is that they are all what I would call upstream factors, they relate to part of the narrative surrounding the company and whilst plausible the authors admit there is little evidence that they actually affect share prices n a positive manner.

As previously discussed, the jury is still out as to whether good ESG characteristics have led to higher stock returns.

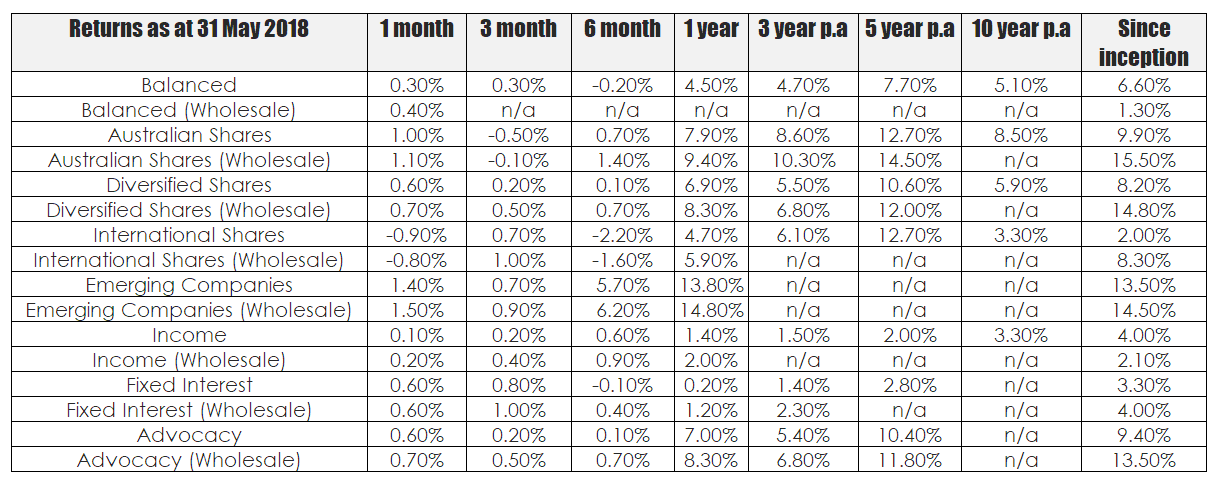

With this lack of evidence in mind I thought I would have a fossick around to see if there were any in the market place. Part of the issue would be identifying those companies which had a high ESG quotient. I thought this would be a pain in the arse so decided to look at funds which had done the work for me. Within the confines of the domestic market the oldest ethical style investing group I could find were Australian Ethical Investments Managed Funds which was founded in 1986 and offers a range of ethical style investments to members. The finding of performance figures was quite easy and I have tabulated the returns for their managed funds into a format that is more readable. The returns for their Super funds can be found here and they appear to be on par with the managed funds.

A quick glance at the figures shows that they are what you would expect from a domestic fund manager with performance seeming to lag behind the index benchmarks. It should be stated that this is not a refection on the notion of ethical investment since I think it is a good idea – it is more a reflection upon the methodologies employed by fund managers in managing their positions. So it is a strategic issue not a tactical one. Part of the issue with ethical investing from the wholesale side is simply sorting out who are the arseholes and who are not. For example Australian Ethical Investments has listed on their website that they are an investor in Facebook. I am not certain whether this has been updated in light of recent data breaches. The same is true for local domestic ethical ETF’s which note an investment in Apple and as much as the Apple fanboys would have you believe otherwise Apple is a party to worker exploitation in China.

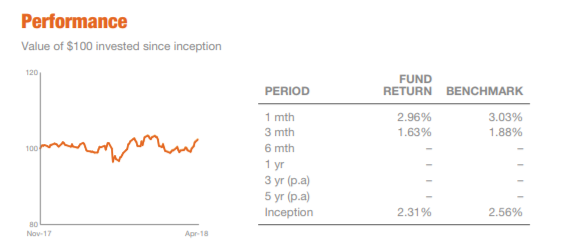

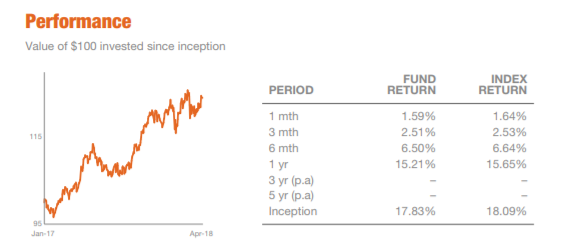

Ethics aside I want to return to the notion of returns since it all laudable to want to feel good about your investment decisions it doesn’t help anyone if you simply join the ranks of the poor. The best way to help the poor is not to be one of them. The returns for the local ethical style investments I looked at were middle of the road – they are certainly not something you will get rich over. I snipped below the performance figures for two local ETF’s – FAIR and ETHI respectively. As you can see whilst they have not been around for long they are failing to beat their benchmarks. In the case of FAIR it is easy to see why – they have too many stocks and have therefore replicated an index from which they draw a fee – it is almost impossible to beat a benchmark in such a situation.

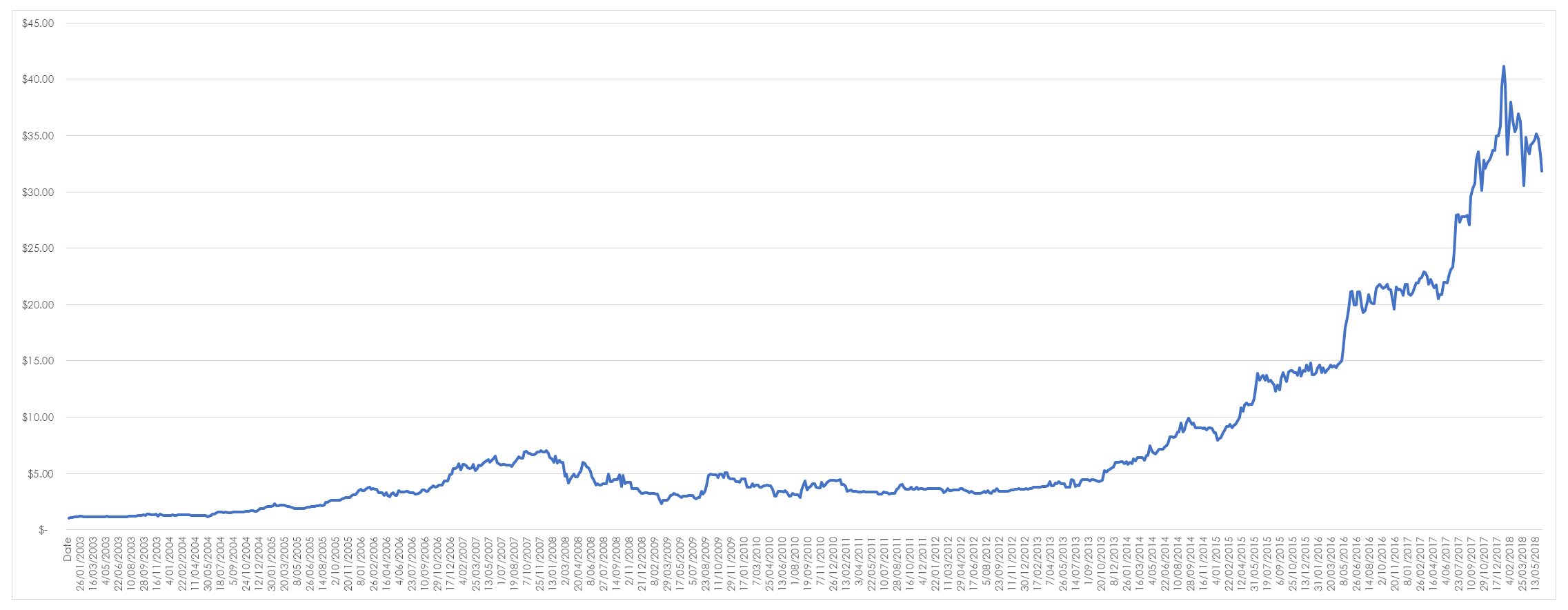

However, the situation is a little bit different if you look at the listed entity that manages Australian Ethical Investments. In doing so you see that charging a fee to manage an investment is more profitable than taking the advice of the investment firm. The chart below looks at the value of $1 invested in AEF since listing.

A quick bit of mental arithmetic shows that investing in AEF as opposed to their funds would have yielded a CAGR of just over 24%pa, which is well beyond the annual return of their best fund. However, there is a flaw in my cunning plan, the average weekly volume of this stock is 1521 shares. So the actual stock is extraordinarily illiquid which in part might explain some of its performance.

This raises the question of ethical investing as a mechanism of wealth creation and with all things the best road seems to be one where you either find a manager to invest in directly and profit from their profitability (if market dynamics allow it) or set up your own ethical screening process which could be quite simple. You simpe use the screening process that others do and exclude certain industries. In fact if I were setting up an in house ethical investing process I would download the list of stocks that ethical funds already invest in and run my scan over that.

")