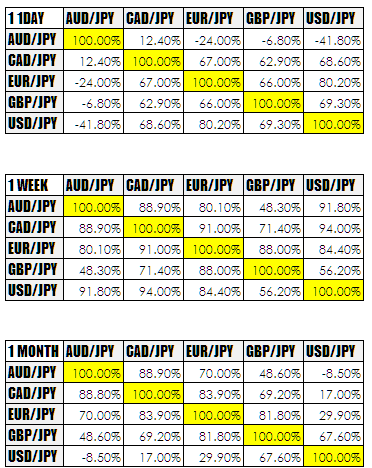

A question popped up in the Mentor Program that related to what to do when related instruments all gave the same signal, in this instance the culprit was various JPY related pairs. I had not looked at FX correlations for awhile so thought I might stick a few together and see if they told me much of a story. With a bit of dodgy-fu I cobbled together the following table which looks at correlations of JPY related pairs over 1 day, 1 week and 1 month.

When looking at correlation we are confronted with two confounding issues. The first, as is obvious from the table above is the time frame over which we look. The shorter the time frame the more we might be prone to simple idiosyncratic shocks appearing in the data. This goes some way to explaining the wild variation i correlations over very sort time frames. As with all things the more data we have the more reliable (sometimes) the conclusions we can draw from what we see.

The second issue is what sort of correlation are we looking at. The correlations above are simple price correlations – do the pairs travel in the same direction over the same time frame. A slightly more sophisticated question question is are the returns from each instrument over various time frames comparable. To answer this question requires that we look at the returns correlations of instruments. The chart below looks at the returns of JPY denominated pairs over a longer time frame.

As broad population they each follow a similar trajectory but there are some notable deviations which can probably be attributed to local factors. One of the issues that often catches FX traders is the assumption that because pairs share a currency then their movement should be identical and as we can see this is not quite true. This causes problems for what signals to take and the entire notion of diversification. Diversification is in its simplest form as practiced by the sell side of the industry revolves around things having different names but even things with similar names can be quite different.

")

How, Chris do you calculate your correlations. Do you use price, direction, both, something else?

My preferred method would be to use returns