Before I begin, I am going to pose a little test.

Imagine you are an investor who sees a fund that promises astronomical returns based upon hypothetical trades. So you fall for the marketing hype and invest by the end of year one the fund has fulfilled its promise and your account is up 100%. So far so good and you sit for another year. But year two is not so good and the fund is down 50%. You console yourself by rationalising that in the first year you made 100% so you can afford a little give back. Assuming you had invested $100,000 how much do you have at the end of year two?

The measurement of results is an area that is fraught with difficulty not least because of the desire for funds to obscure how little they make. However, it is not only professional funds that have trouble working out how much they make it is investors right across the experience spectrum. Market historians should be aware of the infamous case of the Beardstown ladies which was an investment club that met regularly in their local church basement to discuss all things investing. The group rose to national prominence after they published a book called The Beardstown Ladies’ Common-Sense Investment Guide: How We Beat the Stock Market – And How You Can Too which claimed that the club was returning 23.4% annually. Not surprisingly this led to a series of books and a speaking tour. The only problem was that the ladies did not know how to calculate returns correctly and their true returns were only 9.1% which trailed the S&P500 for the same period. Such mistakes are easy to make as people often forget to account for funds that they may have added to their account thereby inflating the actual return.

When presenting returns there are a few givens that enable the presentation of an accurate account. Most important is either a series of unit prices which are like a share price and from these can be built an equity curve. An equity curve gives you a sense of the trajectory of returns and at the same time gives you an instant idea of what the drawdown for a fund or system might be. Simply presenting a series of percentage returns either overall or for a series of hypothetical trades does not convey enough information to make an informed decision.

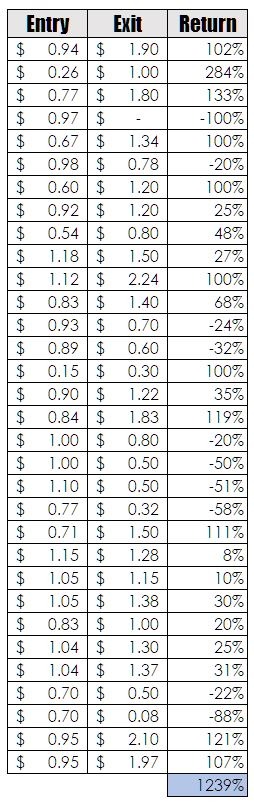

The returns below were from a posting that popped into my LinkedIn feed – I have tidied them up by dropping them into Excel. The implied claim is that if you had taken all these trades during the first half of the year then your account would be up 1239%. Certainly, an impressive claim but remember we are in the land of social media, so we have to be a little circumspect in our interpretation of such things.

Simply summing percentage returns and then saying you would have made this much in total or this much on average does not work. Let us return to the question I posed at the start. How much have you made from your fund that was up 100% in the first year and then down 50% in the second year?. So you look at the last report from the fund and they claim that they have an average return of 25% per annum, which is actually a true claim. So you assume you made 25% in the first year taking your total to $125,000 and then you made another 25% in the second year bringing your total investment to $156,250. You find your actual statement and see that you have not made a cent. The fund doubled in the first year and then halved in the second. Your $100,000 became $200,000 at the end of year one and in the second year, it halved taking you back to your starting point. But the fund proudly proclaims they make 25% per annum and they do – it’s just that this figure is a trick of statistics and is irrelevant.

Simply summing percentage returns and then saying you would have made this much in total or this much on average does not work. Let us return to the question I posed at the start. How much have you made from your fund that was up 100% in the first year and then down 50% in the second year?. So you look at the last report from the fund and they claim that they have an average return of 25% per annum, which is actually a true claim. So you assume you made 25% in the first year taking your total to $125,000 and then you made another 25% in the second year bringing your total investment to $156,250. You find your actual statement and see that you have not made a cent. The fund doubled in the first year and then halved in the second. Your $100,000 became $200,000 at the end of year one and in the second year, it halved taking you back to your starting point. But the fund proudly proclaims they make 25% per annum and they do – it’s just that this figure is a trick of statistics and is irrelevant.

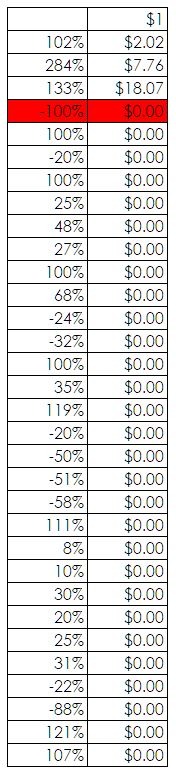

If I recalculate the returns above in the form of a unit price with a $1 starting point, then we get the following return.

After the third trade, the account blows itself up because of the 100% loss on this trade. If this were a fund or an actual trading system and results presented in the way they should be then you can see what would have actually happened.

After the third trade, the account blows itself up because of the 100% loss on this trade. If this were a fund or an actual trading system and results presented in the way they should be then you can see what would have actually happened.

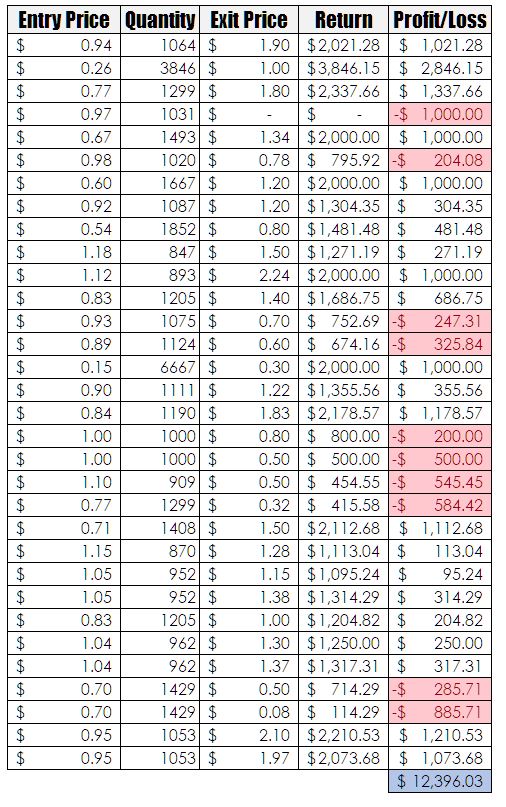

This does raise the question of is there any way that we can generate the claimed return of 1239% and there is. You opt for the unrealistic strategy of investing the same amount in each trade irrespective of its outcome. In the table below I assumed that $1000 was invested into each trade. This partitions the total loss of the account that occurs after the third trade.

As you can see we hit our magic mark of 1239% if we assume that we only invested $1000 but we had to turn over $32,000 to achieve these results – so we sort of got there but didn’t really.