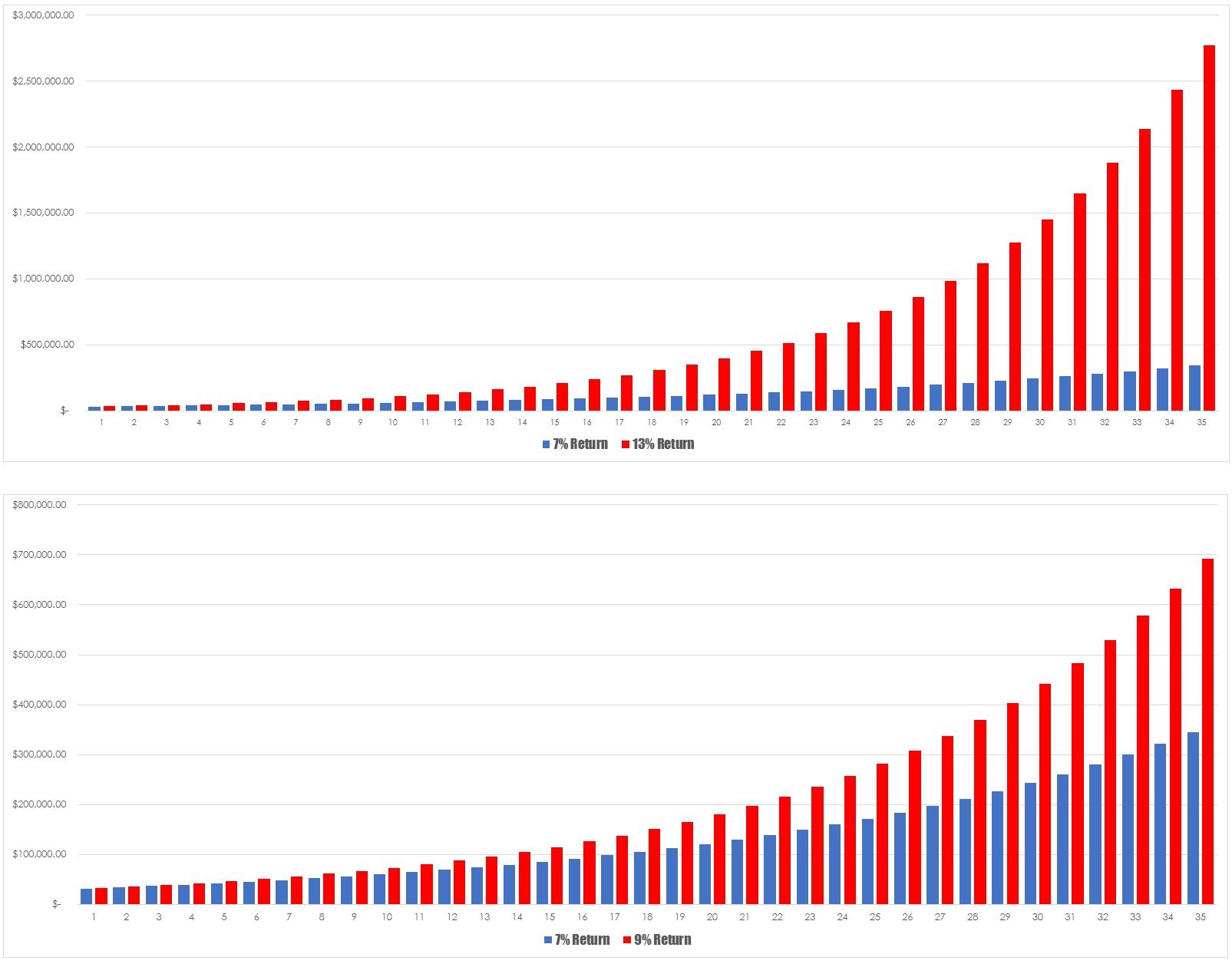

In this post, I had a bit of a dig at the self-congratulatory nature of super funds and their lack of performance. In my piece, I mentioned that the long term rate for super funds was quoted at being around 7% for the past 30 years. So I decided to see what the differential between super funds and the market was costing investors. I generated two plots, both assumed a starting age of 30 and a starting balance of $30,000. I then initially plotted the average super funds stated return of 7% against the market’s long term total return of 13%. I then repeated this exercise but used a more conservative 9% as the comparison rate.

As you would expect the difference between the 7% return and 13% return is substantial – $345,184.56 versus $2,770,347.69. In this most ideal of worlds, the average super fund has cost the investor $2,425,163.13. In the more realistic case of 7% versus 9%, this differential narrows to $346,716.95 which in real terms is still a remarkable difference in terminal return.

As you would expect the difference between the 7% return and 13% return is substantial – $345,184.56 versus $2,770,347.69. In this most ideal of worlds, the average super fund has cost the investor $2,425,163.13. In the more realistic case of 7% versus 9%, this differential narrows to $346,716.95 which in real terms is still a remarkable difference in terminal return.

Apart from being an exercise in reinforcing how compounding works – a lesson many forget it is also a salutary example of how small decisions can have dramatic long term effects.