I came across this study the other day – Which Investment Behaviors Really Matter for Individual Investors? by a group at Goethe University in Frankfurt.

The aim of the study was to examine various investor behaviours and see if these behaviours had any impact if any upon investor returns. As the study points out there have been numerous studies that have looked at single variables such as overtrading, gambling like behaviours and a lack of diversification. And it is well established that many aberrant behaviours do have a substantial impact upon returns.

However, this study was somewhat more ambitious in that it looked at ten variables simultaneously. The variables they looked at were as follows.

- Portfolio turnover: Active trading volume (excluding savings plans) scaled by portfolio value as a proxy for trading activity and investor overconfidence.

- Trade clustering: Clustering of investors’ trades in time as a proxy for the absence of narrow framing (a narrow-framing investor makes investment decisions individually and not in a portfolio context).

- Disposition effect: Tendency to sell securities that have increased in value and keep those that have lost value.

- Leading turnover: Tendency to systematically trade before other investors (in the same security in the same direction)

- Forecasting skill: Ability to systematically realize excess returns on purchased securities.

- Trend chasing: Tendency to purchase funds that have recently increased in value.

- Home bias: Preference for investing in German stocks or funds with Germany as their investment theme, thus neglecting international diversification.

- Local bias: Preference for investing in local stocks (i.e., in companies with head-quarters close to the investor) or local funds (i.e., funds managed by companies geographically close to the investor).

- Lottery-stock preference: Investment in stocks with lottery-like characteristics (low price, high idiosyncratic volatility, and high idiosyncratic skewness).

- Under-diversification: Investment in only a few securities and/or highly correlated securities.

Interestingly, the study found that only two behaviours had a significant impact upon returns – lottery stocks and a lack of diversification .Removing the lack of diversification lifted performance by 4% and avoiding lottery bias lifted performance by 3.1% Lack of diversification is easy to understand since the literature on this is pretty clear. Appropriately structured diversification that is both market and instrument based both increases returns lowers the volatility of returns that a portfolio can achieve. There is no argument here.

The concept of lottery stocks needs to be explored in more depth since this is not well explained by the paper. Within trading there is a perpetual confusion between volatility and trend – the two are not the same. Volatility is a measure of the speed and magnitude of price movement, it is not directly observable and it has no bias.

This lack of bias is very important for traders to understand since it is a trap for the unwary. A key sign that someone does not understand what they are talking about is when they refer to upward volatility.

If I have a stock that is valued at $1.00 and a 30 day volatility of 20% that means that I can have a reasonable expectation that over the next 30 days the price trajectory of the stock will be found somewhere between $0.80 and $1.20. It does not mean that it will go up 20%. The natural assumption of traders is that if a stock has high volatility then it will go up by a large amount – this is an incorrect assumption.

Traders too often ignore the role of volatility within the decision making process and I think this is not only a function of a lottery bias but also a failure in understanding what an ideal move looks like. At some stage during the mentor program I always get the participants to find a stock that represents to them the ideal move. We then take this move and begin to look at the fundamental building blocks of the price action. Within this it is also necessary to look at the role of volatility – that is what is the current volatility of the stock in relation to its historical volatility. From my perspective the ideal stock move has only a few basic characteristics. And these are easy to elucidate.

- Stock is breaking out from a base.

- Volume is increasing.

- Historical volatility for the instrument is below the average historical volatility.

Note that the trend requirement and volatility requirement are separate functions – this is because as I have said they are not the same. This is despite them being treated as one and the same by most.

I think that what the paper has identified is the tendency of traders to buy high volatility instruments that are not trending. Locally we would call these dogs, my guess is that they are generally tips that either came from their brokers or alternatively their idiot brother in laws.

Intriguingly, the paper suggests that trend following is a negative behaviour or bias. I attribute this to academics simply not understanding how any form of trend based trading works and thereby falling prey to their own bias.

Footnote. Coincidentally at the same time I came across this article this article which dropped into a junk mail address I keep for such things.

This article contains some interesting statements.

A big myth is that investing offshore leads to better returns or better diversification. Both are untrue. There are more than enough great shares in Australia to profit from.

I am always intrigued when I see people offer such advice since it is clearly not what the evidence shows. In terms of capitalization the Australian market offers less than 2% of world equity values. We are a tiny closed system. Evidence of this is that since the GFC the US market has gone up 173%. The local market has gained about 20%.

Select eight to 12 stocks from the top 20 shares on the Australian market paying good dividends. Divide your money between them and leave the stocks in the bottom drawer, as history has proven they will grow over time. Also, remember smaller portfolios are easier to manage and represent lower risk. The more stocks you have, the more work is needed to manage your risk and the higher your transaction costs.

Interestingly, this contradicts advice given earlier in the article about learning to sell. The notion of smaller portfolios reducing risk is also wrong. The natural extension of this is that a portfolio will one stock in it should have no risk at all.

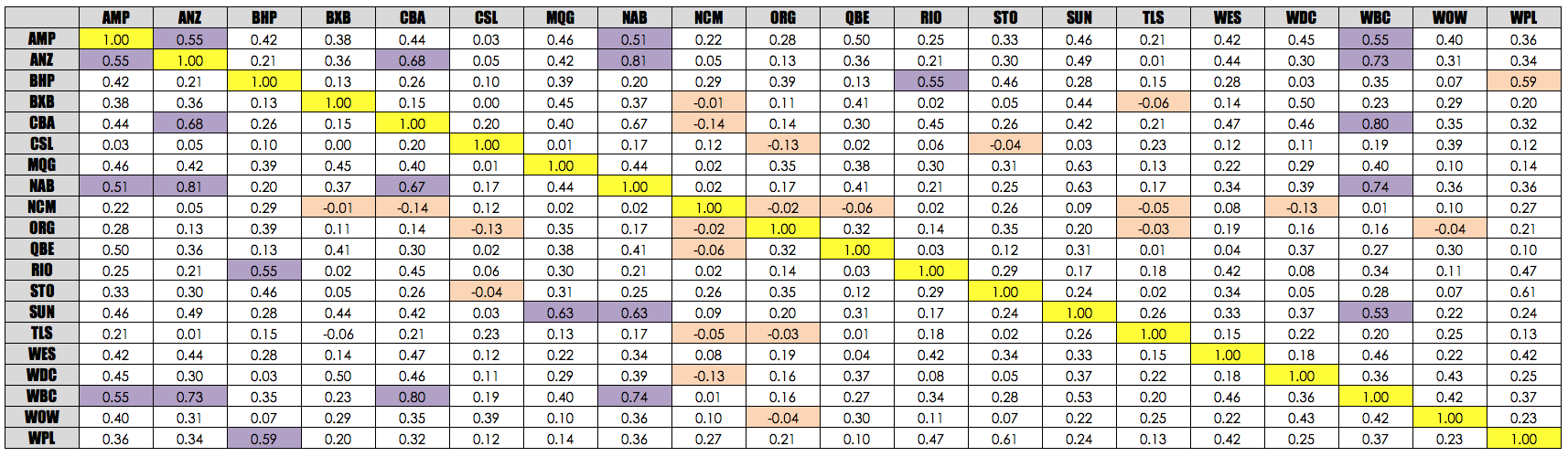

However, the biggest problem with this is that it simply ignores the notion of correlation within a closed index. Buying 8 to 12 shares within the ASX 20 is tantamount to buying the index itself. So you actually have one position. Again diversification is ignored which is fine if you are an index trader but if you are a stock trader diversification cannot be ignored.

To give you a sense of the correlations between the top 20 I have generated the following correlation matrix.

I have coloured those with a correlation greater than 0.50 in purple and those with a negative correlation in orange.

")