One of the stupidest axioms in investing is that it is always a good time to invest despite there being no evidence that this is true and substantial evidence to the contrary.

The common argument is that if you are not always invested you will miss the good days and a handful of good days make up the bulk of the gains investors are exposed to. Unfortunately, this ignores the other side of the equation – missing the bad days.

As I have shown previously, missing the bad days has a much greater impact on returns than missing the good days. There is a very simple reason for this – the relative impact of gains and losses upon an account are asymmetric. A 10% loss cannot be replaced by a 10% gain, it requires 11.1%.

Plotting this loss to recovery ratio yields an exponential curve that cannot be overcome.

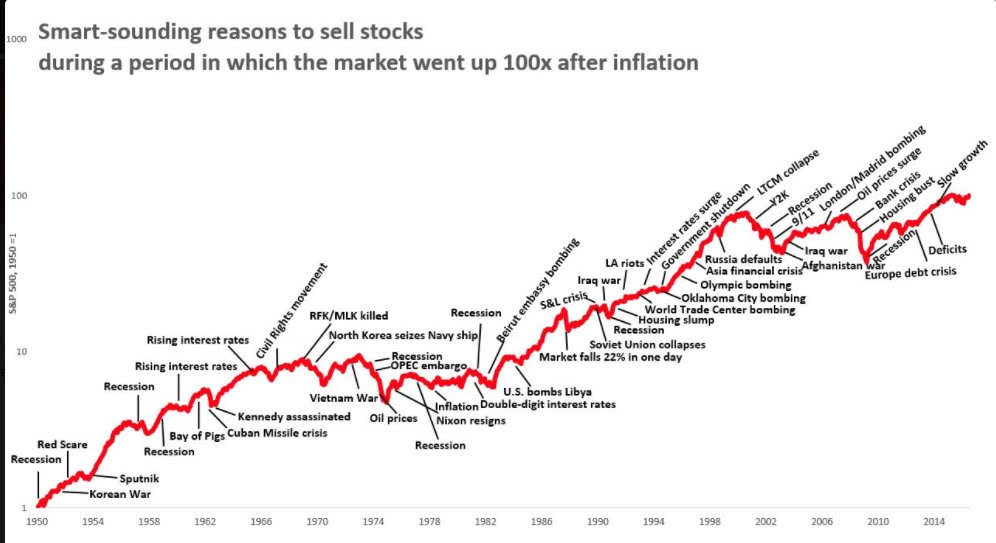

Despite this, it seems that the myth of being constantly invested won’t die. Its latest iteration appeared on my LinkedIn page last week in the form of the following somewhat fuzzy chart.

This chart looks at inflation-adjusted returns for the S&P500 and makes the claim that the market went up 100-fold despite all the apparent reasons to sell everything and run to the hills. This is supposedly evidence to always be in the market.

However, there are some annoying little problems with this chart and the interpretation that you should always be in the market.

This is a chart of an index – most people don’t own the index they own a basket of stocks. An index is a carefully curated aggregation of stocks designed to go up and thereby generate this upward bias. People who post these sorts of charts don’t seem to be aware of that simple fact.

Even if you did own the index you need to have a careful look at the scale. As I continually harp on about: scale matters. In inflation-adjusted charts the US market went nowhere between 1966 and 1996 – in adjusted terms, you have lost three decades. Even the most dedicated buy-and-hold adherents would realise that this would be devastating to an investor’s thoughts of meaningful wealth creation. The same problem arises between 2000 and 2013 where once again the market offers no real gain.

Once again the only compelling reason to always be in the market seems to exist in the imagination of pundits who lack a basic understanding of how markets work at various points in the economic cycle. There are good times to be in the market and there are bad times to be in the market.

Get the two confused and you end up going nowhere.