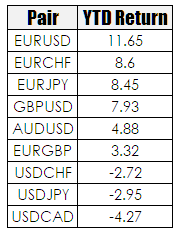

I caught a piece in Bloomberg this morning that had FX traders lamenting the lack of volatility in FX markets this year and using that as an excuse for their lack of profitability. Upon seeing this I thought to myself that this sounds awfully familiar amd it does – it is the classic I dont understand the difference between volatility and trend but it also sounded familiar to me for a reason I will come to in a moment. I decided to have a look at the returns possible on several of the FX majors and see if the first part of the observation was true, namely that there has been a dearth of opportunities for trades this year. I started off by firing up Bloomberg and looking at the YTD returns for a series of pairs – note this si simply based upon buying and holding the currency. This approach generated the following returns –

However, in FX trading it is not traditional practice to simply buy a currency and hold it; FX is the preserve of the active trader. Its 24 hour nature and extreme liquidity over almost all time frames lends itself to this sort of activity. As such I wanted to see what sort of moves were available to traders and how these compared to simply holding the currency. To do this I plotted the above pairs using a daily chart and on this chart I dropped a 3ATR trailing stop that is plotted continuously, such a tool as a wonderfully blunt trend filter – in effect it is a surrogate volatility breakout system. It produces the sort of chart displayed below –

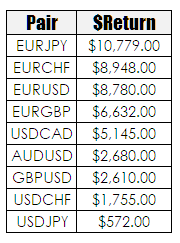

I then looked for the longest trend as defined by this method for the year. I then took the close of the first bar after a trend change and the close of the first bar after a trend change and used this as the basis for a very simple trading. I assumed that the trader was fairly traditional and traded a single 100K lot. The results are shown below –

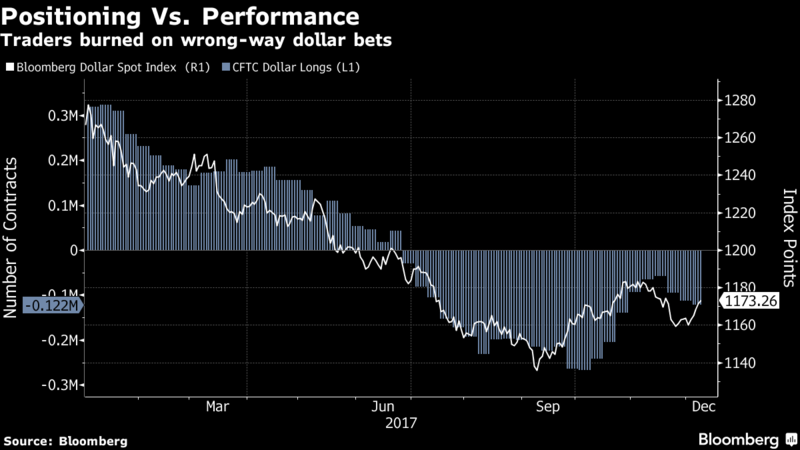

This tells us something very interesting – despite the presumed lack of volatility there were still trends that could be traded which would have generated a positive return, particularly once you factor in the leverage available in FX markets.. So the lack of volatility is convenient excuse for not really knowing what you are doing whilst still being paid a fortune to do it. The reason I offer this as an explanation is that the real reason for the failure of major FX traders this year is given away later in the article and it is defined by this chart –

Traders have consistently been on the wrong side of the trend – it is not a lack of volatility that is to blame but rather simply not understanding that if your narrative doesn’t match the markets then you are going to suffer. All that matters is that you are on the right side of the trend – everything is is superfluous. I did say earlier that the lack of volatility as an excuse sounded familiar so I did a bit of digging and found the following from 2013 –

Q1 2013 from Parker Global Strategies showed improvement in performance from currency managers for the first time in several years. The Parker FX index measures both the reported and the risk-adjusted returns of 42 global currency managers running around $43bn in assets. Despite a positive start to the year, however, the index fell 1.33% in August as the US dollar had a very strong month against most emerging market currencies – underlining that bouts of volatility remain a risk and that managers are still really struggling to identify trends with sufficient strength.

Source IPE

So here we have volatility being blamed for the lack of returns, along with the fact that it seems like currency managers never make money. But here is more, this time from 2016 –

“It was a tough environment because there was a lot of volatility in currency markets without clear direction,” said Van Luu, head of currency and fixed-income strategy in London at Russell Investments, which manages around $US244 billion. “Trends that had existed before the Brexit vote very suddenly reversed. Those are very, very sudden shifts that are not particularly amenable to many hedge-fund strategies.”

Source – Australian Financial Review

My experience over almost four decades has been that you will never find a money manager who is short of an excuse, even if that excuse runs directly counter to their last excuse.

")