")

One of the most interesting things about markets is that they are not an homogeneous ecology – those who lack experience in trading or investing tend to speak about equity markets as if every segment is exactly the same as every other segment. It is obvious that the market is split into segments based upon industry type – it is easy to see the dichotomy between retail, banking and mining stocks. However, this is a somewhat superficial analysis and it fails to understand some of the nuances that occur within the various indices that cover various segments as opposed to industry groups.

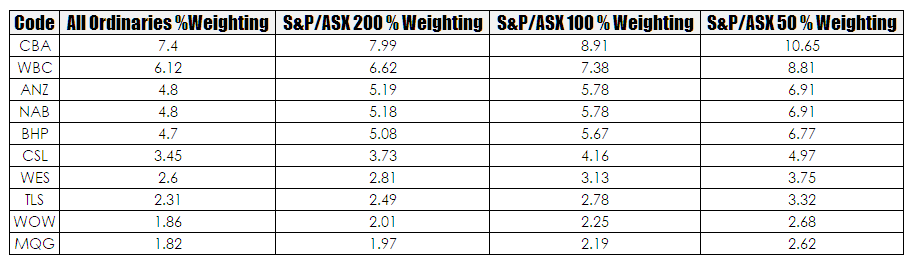

If I were to make a broad statement about the All Ordinaries since the GFC I could say that it is has been remarkably lacklustre in its performance and simply viewing a chart of the index would confirm this. However, by their very construction an index doesn’t give the whole story. In simple terms an index is a basket of stocks where the biggest stock wins – that is it exerts a disproportionate weight upon the index and therefore the trajectory of the index. In the table below I have isolated the weightings for the top 10 domestic stocks within a series of S&P defined indices.

As we become more granular in our examination of the indices the weighting of each component shifts subtly upwards. An understanding of weightings and how they shift can also have a bearing on what the index is telling you. The largest companies in Australia exert a disproportionate influence upon the index. This is to be expected and it occurs in all indices – an index is an imperfect representation of what is occurring within a market. The ultimate example of this is the Dow Jones Industrial Index which is so oddly skewed and narrow in focus as to be an irrelevancy. There is a lot of noise within an index and whilst the top 10 stocks within the All Ordinaries make up approximately 40% of the index , if we move to the top 20 stocks within the All Ordinaries this grows to just over 50% and the top 50 is just over 70%.

We can actually remove the weightings of each individual stock and have a look at the trajectory of the number of stocks going up versus the number going down courtesy of the Cumulative Advance Decline Line. If an index moves buy a given amount we dont know if this movement is due to simply one stock, a small basket of stocks or is a more broader move. The A/D Line is a simple blunt tool that is a general barometer of market health. Below I have plotted the A/D Line for the All Ordinaries, the S&P/ASX 200 and the S&P/ASX 100.

As can be seen from the above charts the narrower the index the smoother the ride – there is markedly less noise in the S&P/ASX 100 A/D Line that the All Ordinaries. This is to be expected both because of the narrower focus of the index and the nature of investment cycles. As a thought experiment put yourself in the shoes of a fund manager post the GFC where you have a constant influx of funds that you have to invest in equities. The internal narrative that you have and the one you present o anyone overseeing your activities is that you will park the cash not in the bottom 100 stocks in the All Ordinaries which are most likely rubbish and should not be listed any way but rather in the top 100 stocks. This is the often talked about flight to safety that money managers engage in when they have run out of ideas. The impact of this is quite clear in the charts above – the S&P/ASX 100 stocks began their bull run in 2013. Funds are slow to seep into other segments of the market and this can be seen in the All Ordinaries A/D Line which has been fairly bumpy over the past few years. Traditionally the extension of our flight to quality narrative is that over time money managers perceive that stocks within an index become fully valued according to their valuation metrics and they then begin to look further afield. This means they begin to look at stocks outside narrow bands such as the top 50 or 100.