One of the good things about being in lockdown is that you get to work on all sorts of little projects and you don’t have to put up with all that pesky people stuff that I am ever so good at. The bad thing is people still send you stupid stuff – the world would be a better place if they send email and social media into lockdown for a while. One of the points I still get rubbish about is the emotional lure of buy and hold – its a bad idea that never seems to go away much like daylight saving.

The traditional argument I still get particular after I belt it in a video is that if I buy a good company in bad times then I can’t lose – this reminds a little bit about what a sensible idea it is to invade Russia in the winter but people persist with silly ideas long after their use-by date. My understanding of buy and hold is a simple one – buy a stock that you understand that has an underlying business that makes money, so let’s look at this as an idea. Within the domestic market, there is no more profitable money-making machine than our big four banks. It would not be unreasonable to suggest that they have a virtual monopoly on services and they charge what they want for those services. There is some modest competition by non-bank lenders by they are small fish.

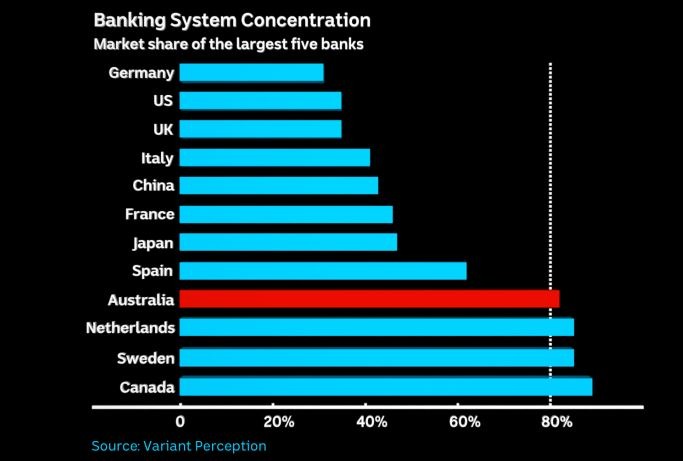

To get a sense of the size of our local banks consider the following two charts that were taken from an ABC report on the banking royal commission – Banking royal commission may crack the big four banks financial dominance.

Each is reasonably self-explanatory.

These final charts are from the RBA Banking Indicators – Chart Pack

So if I read from the top I see –

- A market segment that is hugely profitable compared to the overall economy on a world scale.

- A concentration of power or a monopoly.

- A return on equity that has been fixed for almost three decades and is considered to be good by world standards.

- The majority of their funding is zero cost since it comes from deposits which on average generate no return for the depositor.

- A reasonable fixed margin on the funding that costs them nothing.

What’s not to like.

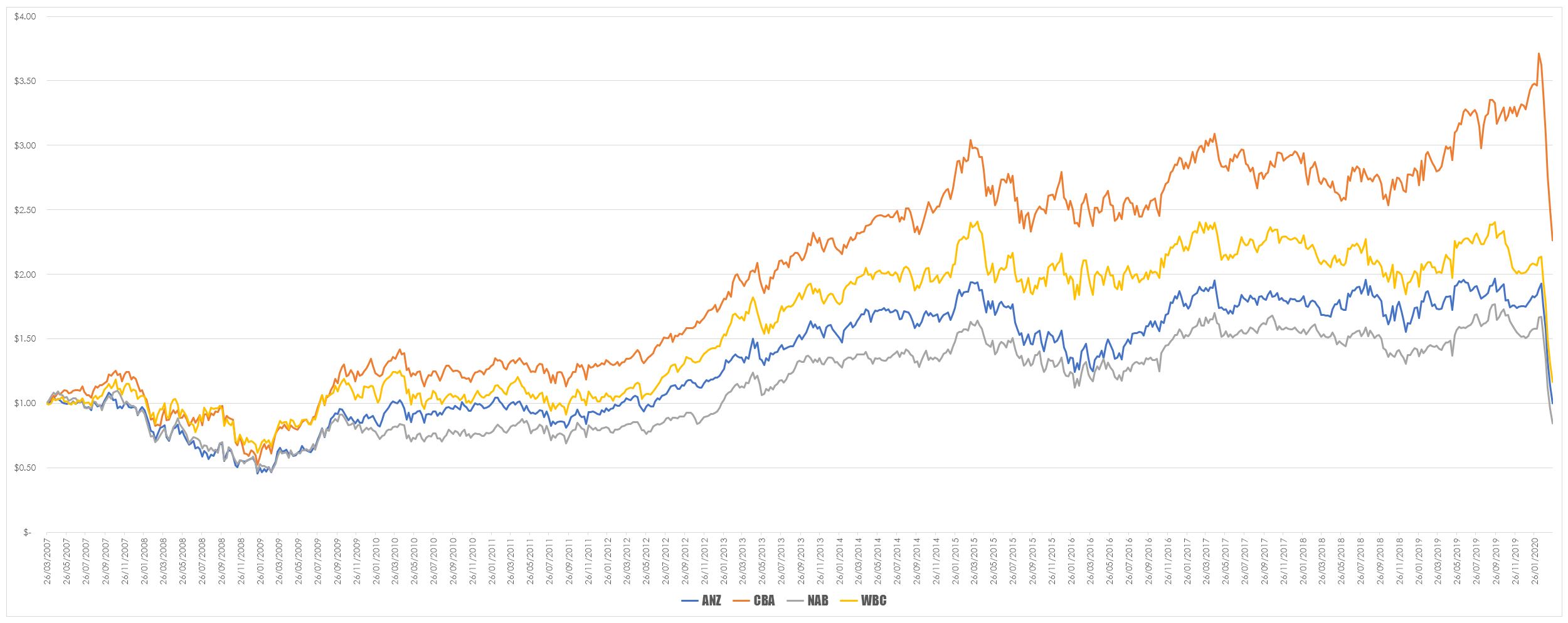

So if we take our basic premise of buying a business you understand that is profitable at a time of financial distress we get the following.

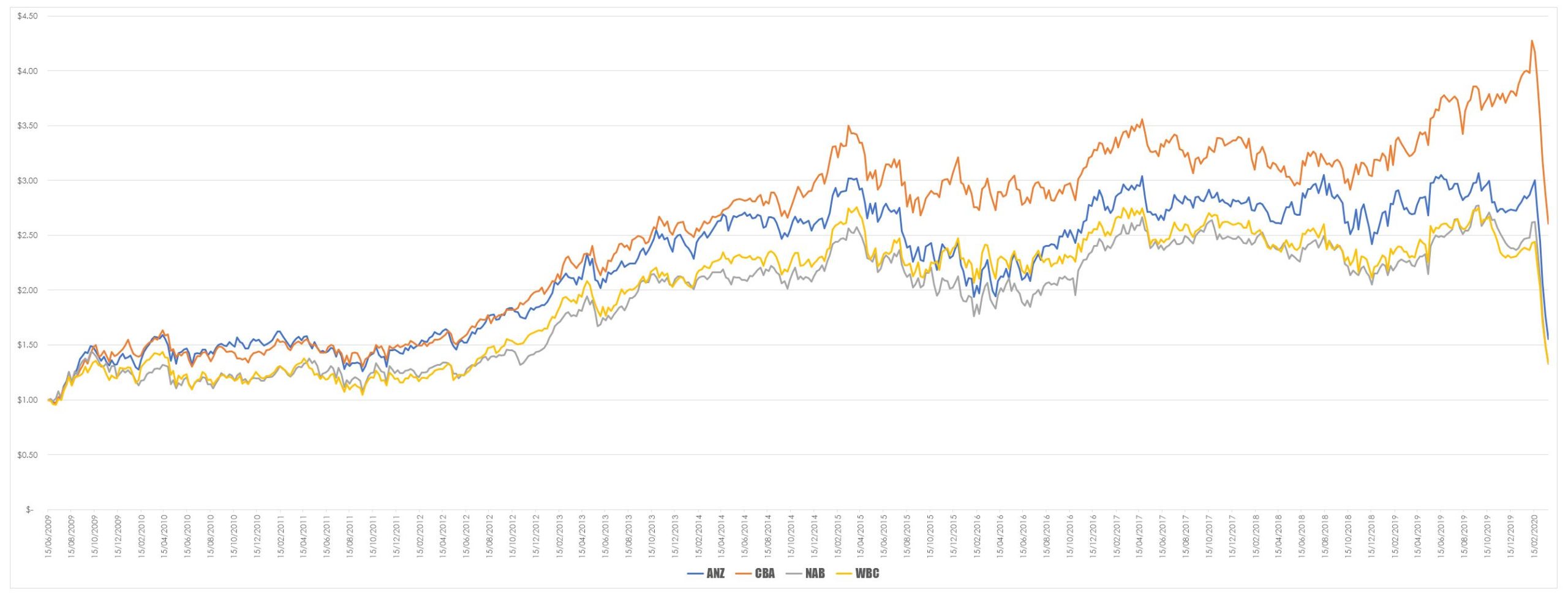

This chart shows the value of $1 invested in each of the four major banks during the GFC – it is not glorious return on performance that might be hoped for. However, it could be argued that the best performing of the banks CBA did show an almost three-fold increase in value before the current crisis hit. However, something interesting happens if we actually wait for a signal to act as opposed to simply trying to be a hero. In the chart below I have replotted the value of $1 invested but this time the starting date was when the 60-week moving average gave a buy signal on the S&P/ASX 200 Banking Industry Index.

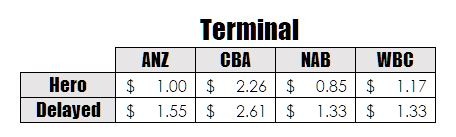

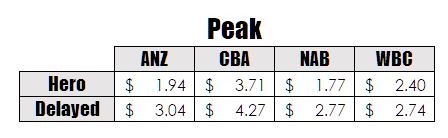

Superficially the curves look the same however there are some striking differences as shown in the two tables below.

The very simple process of delaying entry has achieved two very interesting things. The peak equity in the delayed system was higher in all four banks as was the terminal equity value. Imagine how much better it would have looked if such a system actually had some form of money management.