I came across this paper the other day. The basic thrust of the paper is that populations are living longer and longer – this is really no surprise. What is surprising is this quote –

Most babies born since 2000 in countries with long-lived residents will celebrate their 100th birthdays if the present yearly growth in life expectancy continues through the 21st century

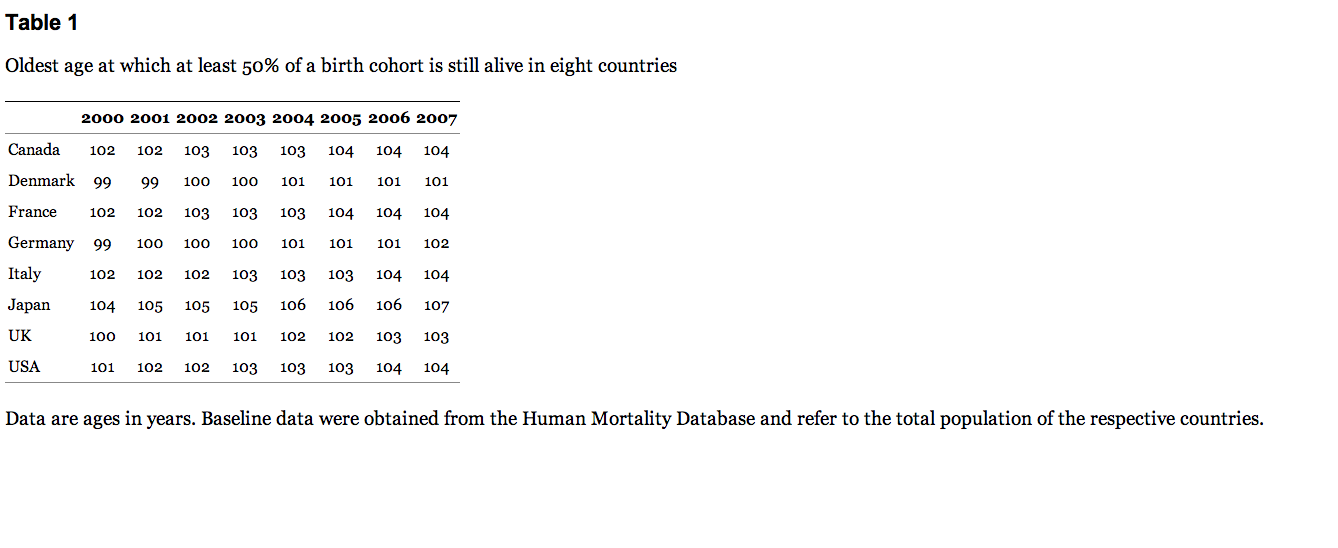

As an addendum to this projection the authors offer the following table which shows the predicted age at which 50% of all those born in 2000 are still alive.

Whether the authors assertions are correct or not, the almost linear rate at which life spans are improving poses an extremely important question. How on earth will people be able to fund such an extended retirement period?

If you retire at 60 is it mathematically possible to fund a retirement that may last another 40 years. Can a working lifespan that lasts 40 years fund a retirement that lasts the same amount of time. My initial guess is that it cannot.

As an extension of this problem Deloittes recently published a study simply looking current trends in retirement and their conclusion was that $1.5 million in super would not be enough to fund a reasonable retirement lifestyle to slightly beyond the age of 70. The reality of needing such a high super balance is in sharp contrast with the average super balance of around $70,000.

I’m not sure about the assumptions on life expectancy. Apparently the current generations are unlikely to live longer than their forebears due to type 2 diabetes among other things.

Having said that, all that means is the taxpayer burden will probably be the same although crunched into a shorter time frame paying for medical expenses rather than costs.

I think the central message is that even though you may retire your money shouldn’t. It needs to stay actively invested rather than going to cash which seems to another furphy the financial planning industry pushes around