Do you ever get the feeling that every single investment idea or movement is the greatest thing since sliced bread. What interests me is that this sort of breathlessness even inhabits what you may liberally call the more refined corners of social media such as LinkedIn. Normally you would only associate rabid fan boy behaviour with the mindlessness of things such as Twitter and whatever comes after that but intriguingly LinkedIn is among the worst offenders. My feed is full of pundits trying to pump and dump any number of things. I have lost track of the number of new mines that have supposedly set new records for recent assays.

This overhyped enthusiasm also spreads to any movement in the price of any asset they may be associated with. Generally, this is gold but it can be anything. For example, early in the month gold had a reversal off the 1675 level and this was heralded as meaning everything from the beginning of the next bull market in gold to the end of COVID to free potato cakes at the football forever. Such a move and its somewhat hysterical interpretation do warrant further investigation.

Below is a chart of gold along with ATR plotted for the period of the reversal.

Plotting any measure of volatility allows you to get a sense of the normal range of movement that may be expected by any instrument over a given time frame. Once you plot ATR you see that the reversal on 09/08 was not outside volatility expectations and a similar sharp reversal occurred on 16/06. Price has a natural movement to it and this movement is simply guided by its volatility – in the short term prices can be found anywhere within their predicted distribution, there is nothing unusual about this it occurs in all instruments over all time frames. What is important is the trend within this movement is occurring. From a technical perspective gold simply had a short term reversal within an existing downtrend. It does certainly not herald the second coming.

Plotting any measure of volatility allows you to get a sense of the normal range of movement that may be expected by any instrument over a given time frame. Once you plot ATR you see that the reversal on 09/08 was not outside volatility expectations and a similar sharp reversal occurred on 16/06. Price has a natural movement to it and this movement is simply guided by its volatility – in the short term prices can be found anywhere within their predicted distribution, there is nothing unusual about this it occurs in all instruments over all time frames. What is important is the trend within this movement is occurring. From a technical perspective gold simply had a short term reversal within an existing downtrend. It does certainly not herald the second coming.

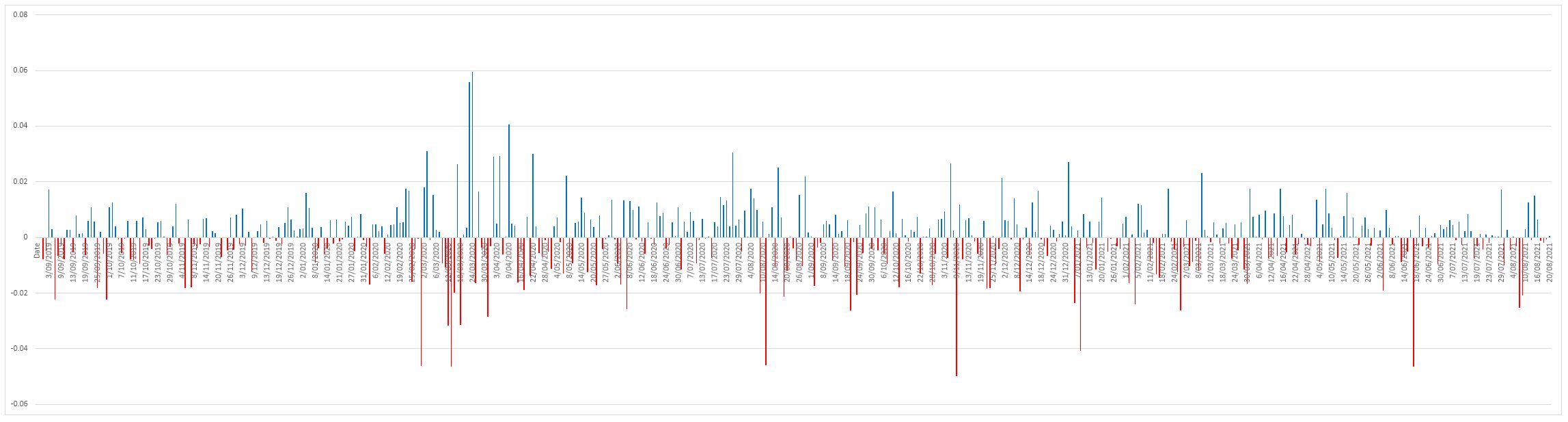

Whenever you have instruments that people have an emotional attachment to you will always get profound overstatements – this is simply people with a vested interest talking their book. This is a long established practice in investment circles. If we look at the daily returns for gold we can see that it has actually been a poor investment for the past year.

Playing with figures a little bit we get a monthly return of 0.31% and a YTD of -4.63% and a yearly return of -7.17%. Hardly anything to write home about when compared to the S&P500 which yields figures of 1.81%, 19.59% and 32.14% respectively.

Playing with figures a little bit we get a monthly return of 0.31% and a YTD of -4.63% and a yearly return of -7.17%. Hardly anything to write home about when compared to the S&P500 which yields figures of 1.81%, 19.59% and 32.14% respectively.

Trading is by its very nature an activity that can generate extreme emotions – the desire to cheerlead the investments you have is strong. Vested interest is a powerful motivator for all involved but for the ordinary investor, it means that not every action deserves a reaction. This applies equally to what you think you see and more importantly to what you are told by others.

")