I regularly get emailed things from S&P Dow Jones Indices – most it relates to index structure, performance or changes. Some of it is data for data sakes with no real use, but some bits are interesting from a summary perspective. I have always had mixed views about volatility and have spoken about it a few times see here and here My views are mixed because it is perennially misunderstood and it is used as an attempt to predict where markets are going. Both are irritating mistakes made by amateurs who claim to be professional.

The interesting thing about volatility is that it displays wonderful mean reversion and this is a point made tangentially by S&P when they talk about volatility returning to markets.

The VIX® returned to levels not seen in several years, breaking through 30 intraday on October 15th before falling back to close yesterday at 17.87. Both rise and fall in the VIX were precipitous and, despite returning to more normal levels, the market remains skittish.

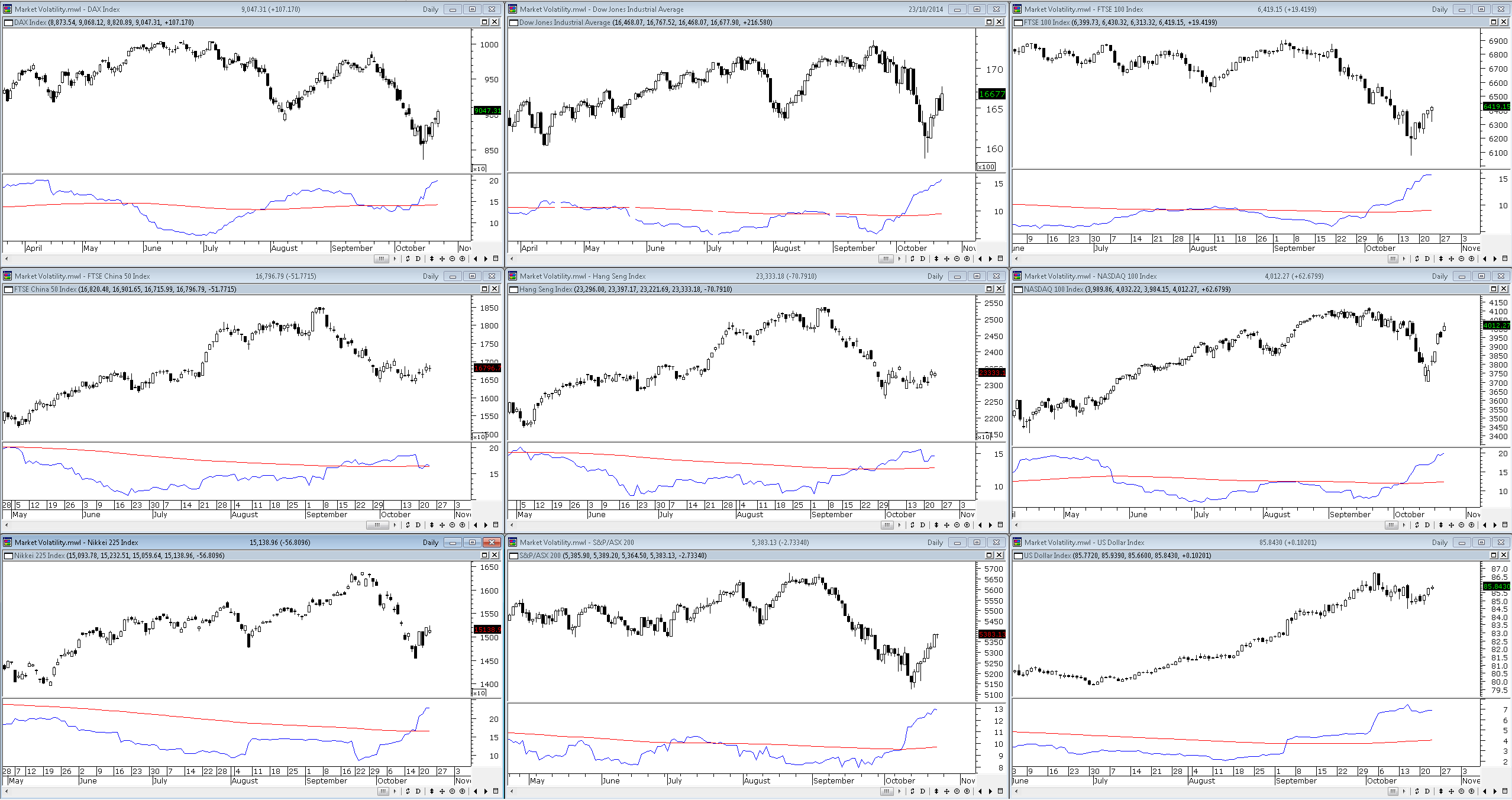

Markets have experienced periods of extended low volatility which would eventually end. The image below is of a selection of world indices with 30 HV and a 250 day MA plotted. The 250 day MA approximates the long term average volatility of each market. As you can see the rise in volatility was not universal with some markets continued to trend but doing so with only a minor increase in volatility.

(Click image for a large version)

There does however remain a central question with such data – what do you do with it and how does it affect your trading decision? For me it actually has little relevance outside of academic interest. That is not to say that I regard volatility as an irrelevancy in trading because it isn’t. I use volatility for bet sizing and for trade selection. Beyond that I feel its actual utility is limited for the majority of traders.

")