Within trading there are a few implicitly stated rules – perhaps first and foremost of these is the acceptance of risk for the opportunity to profit. The balancing act between risk and reward has over the decades been fertile ground for academics to traders. Academics seek a mythical middle ground that defines an appropriate balance between risk and reward and traders more often than not simply say screw that how much can I make without blowing myself up.

To facilitate the perhaps more academic and conservative line of thinking those on the sell side of the industry always talk about safe haven instruments, when I was involved in broking stocks that fulfilled this function were called defensive stocks. The old mantra used to run along the lines of the world is going to hell find someone who makes fridges and buy them because people always need fridges. IG Markets who I have an account with recently sent me one of their monthly blurbs where they were talking about safe have instruments and they mentioned a collection that I have listed below –

- Gold

- Government bonds

- US dollar

- Japanese yen

- Swiss Franc

- Defensive stocks

I have to admit I have never been convinced about the arguments surrounding the notion of defensive plays in part because of a philosophical difference regarding the way I see trading. If markets are going to hell in a handbasket then simply leave don’t skulk around looking for something that might be battered less than the average. I do admit this applies mainly to defensive stocks – my central belief in stock selection is that it is nowhere near as important as market selection so if a market is going down all stocks within that market are tainted. My objection to seeing instruments such as gold as a safe haven come from the mania and lack of logic that surrounds gold. Gold in my eyes is merely bitcoin but without the technology backstory – both are simply speculative vehicles driven by mania and irrational narratives. In the case of bitcoin, it seems to be evenly split between those who believe blockchain is the most amazing thing since the lightbulb and those wonderful conspiracy nuts who believe that bitcoin will replace central banks. If I can digress a little bit it is here that to my eye gold and bitcoin overlap in that they are the preserve largely of the conspiracy nut – that is people who are devoid of the capacity to think logically and who see everything through the prism of an overwhelming desire for simple explanations. Couple this with a desire for group identity and you have all the makings of manic behaviour.

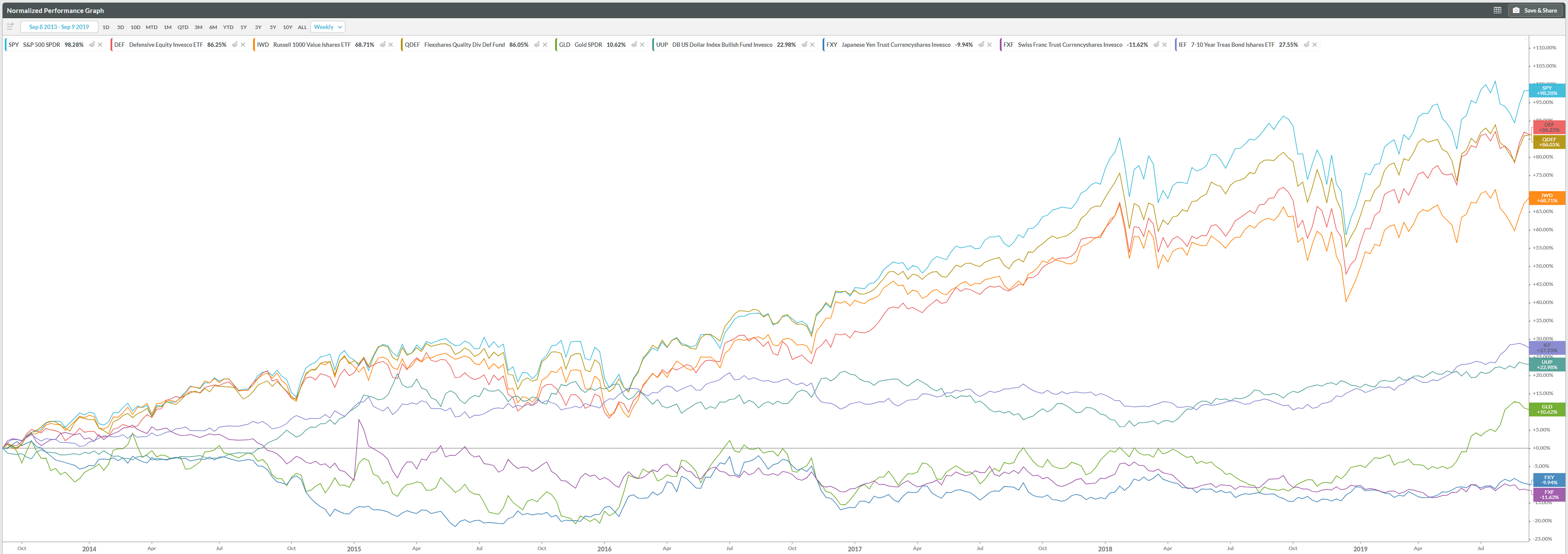

However, that is a digression. With the IG Markets article in mind, I thought I would have a look at how safe haven or defensive issues have performed versus the S&P500 over the past few years. The chart below compares the following ETFs to the S&P500 –

- DEF – Invesco Defensive Equity

- IND- Ishares Russell 1000 Value

- QDEF – Flexshares Quality Dividend Defensive Fund

- GLD – Gold SPDR

- UUP – Invesco DB US Dollar Index

- FXY – Invesco CurrencyShares Japanese Yen Trust

- FXY – Invesco CurrencyShares Swiss France Trust

- IEF – iShares 7-10 Year T-Bond

Click on the images to enlarge them.

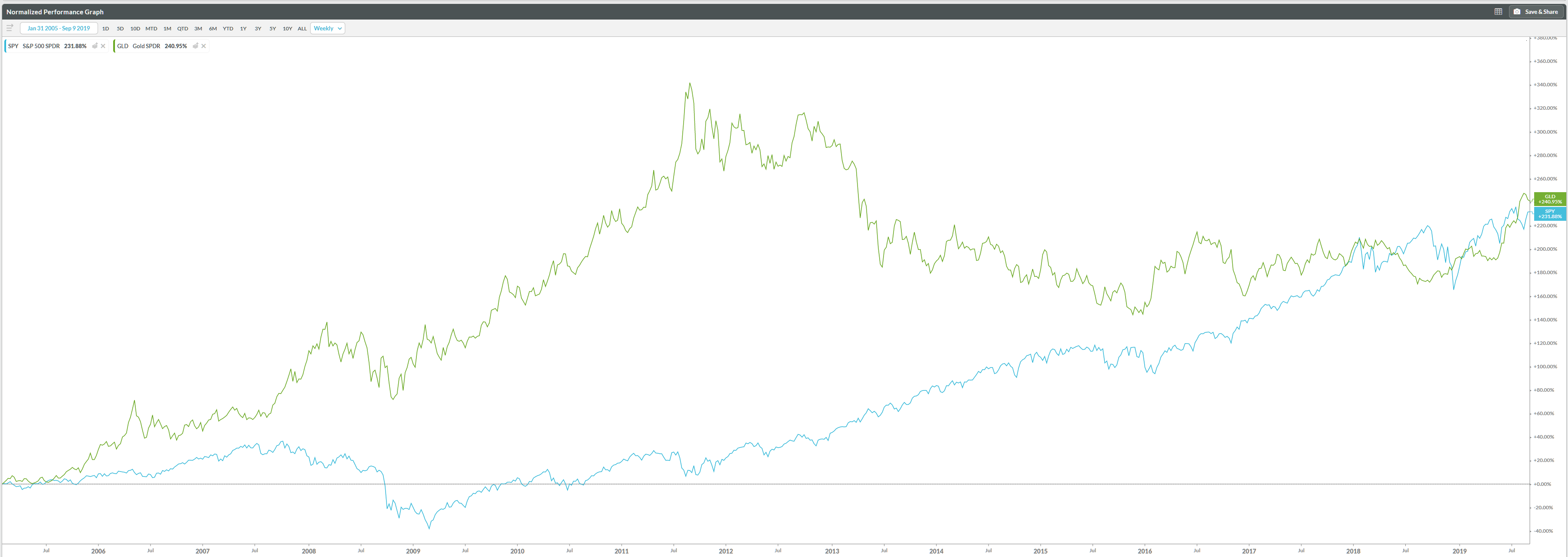

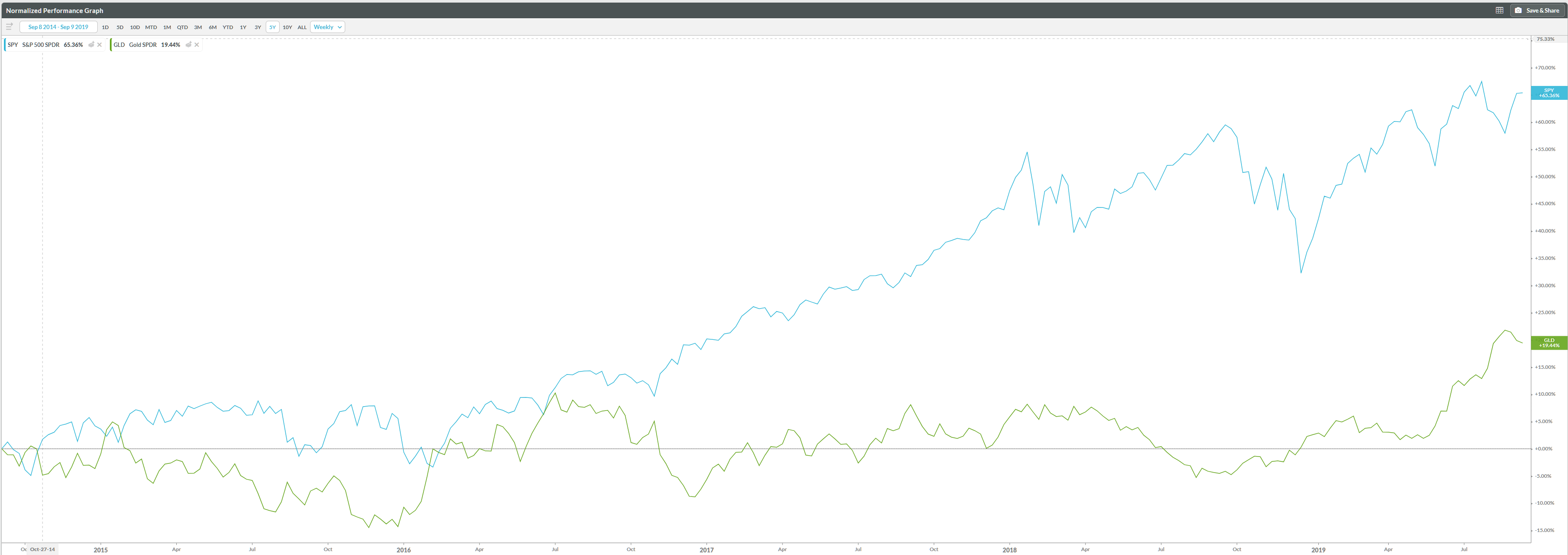

The most immediate point is that over the time frame in question simply investing in the main market index wins – our defensive plays turn out to be fairly poor. Without the closest competitors being share based ETFs that probably mimic the behaviour of the broader market. However, the comparison is a little unfair because it covers a period of a very strong bull market it is, therefore, natural to expect that a simple index play would do well. Dropping currencies in there is also a little unfair as currencies only have a bounded price range available to them. For example, you won’t go to bed tonight with the AUD @ $0.6850 and wake up in a years time and find its $6.80 as you might with an equity. FX is bounded by government intervention. This leaves the old chestnut gold which is heralded as the saviour of us all particular according to my Linkedin feed. To see how gold fared I generated the three following charts which look at gold versus the S&P500 over 15 years, 10 years and 5 years respectively.

The outcome is fairly obvious. This, however, does leave open the question of what to do when markets turn bad. That’s easy runaway.

")