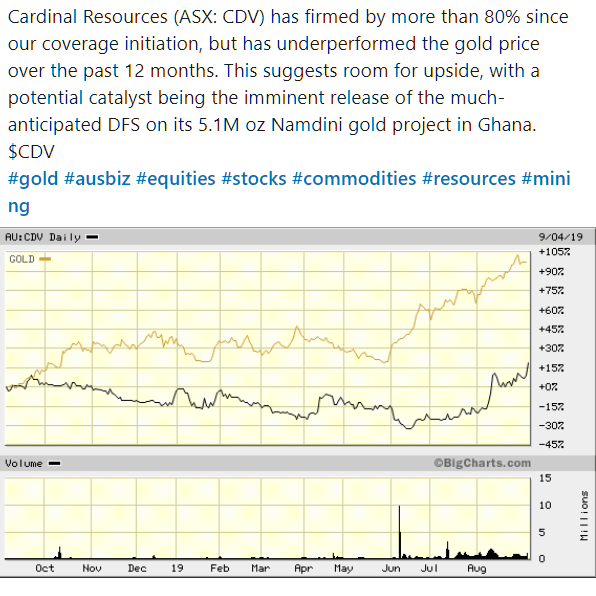

I have written before that starting date is everything when we are looking at comparing the performance of instruments. Fudging starting dates is a favourite trick of fund managers when trying to make their fund look good, they simply hunt around for a starting date that makes them look good and then runs with that. However, starting dates also causes a problem for those looking to compare one instrument with another. For example, consider the snip below from Linkedin –

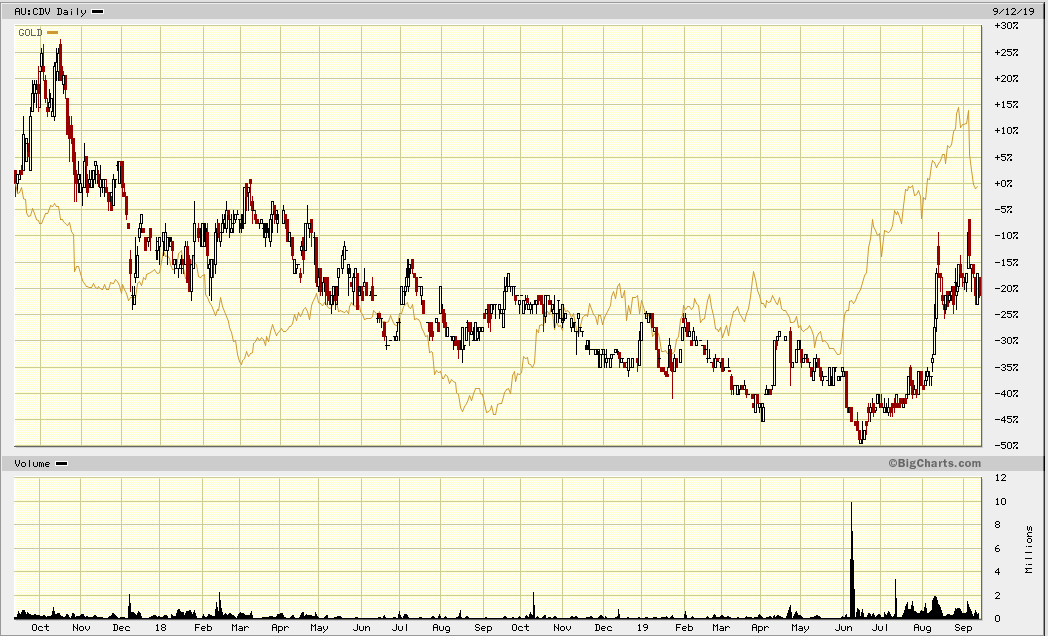

I am familiar with both CDV and gold so I went into the same charting program as the one used to generate the comparison above and had a look at a few different periods. Yhe first period I looked at was two years.

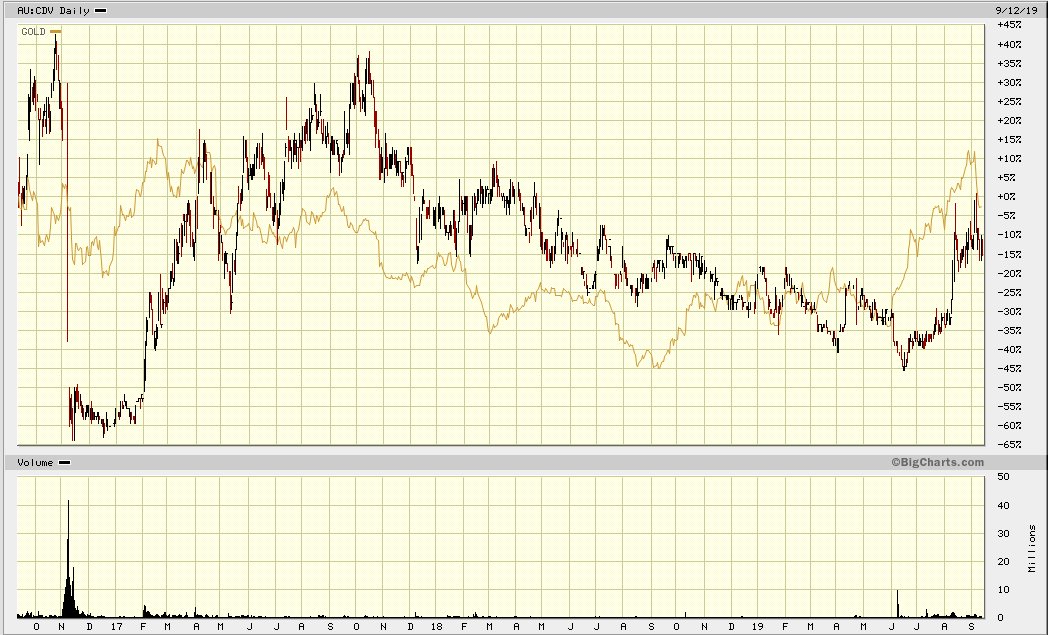

The outperformance by gold holds true over this longer period but only since 11/18 before that gold underperformed CDV. This gives a clue to what the longer-term comparison looks like and suggests perhaps a different narrative. The three and four-year comparisons are shown below.

As can be seen, CDV has for the vast majority of the period under investigation outperformed the price of gold. Therefore an alternative explanation you could generate is that the current disparity is a reflection of simple mean reversion in performance over the long term. Alternatively, the short term outperformance by gold could also be seen as merely an artefact in the data generated by the starting date. Either way, it is difficult to generate a tradeable hypothesis from the data provided.

This is the central problem with performance comparisons – they are very date dependant and if you are not careful you can be generating a false comparison that over a slightly different time period does not exist. My guess is the only way to solve this is to set a fixed schedule for comparisons say every six months and make certain that this schedule fits the time frame you are trading.