Last week LB spoke at the Young AICC in what was a fairly polite look at shares versus property. You can tell by the fact that I used the world polite that I obviously wasn’t speaking. After the event there were a few things I pondered on the way home. The first was my observation that I am old and have been around for a long time, as such you get a different perspective on markets of all sorts. Since I became interested in markets I have seen the following –

- The bull run of the 1980’s

- The 1987 Crash

- The collapse of the GBP and its removal from the ERM

- Japans wonderful bubble and eventual demise.

- The collapse of Barings Bank

- The Dot Com boom

- The Asian Economic Crisis

- The Dot Com bust

- The bull market of the 2000’s

- The GFC

This is the benefit of longevity, my observation of property folks is that they have only ever seen a bull market and this coloured many of the points they made. To them it was inconceivable that property could ever encounter problems. This observation is simply a function of their lack of experience and the fact that if you had bought property in Melbourne any time in the past decade it has gone up. I saw the same thing happen to traders during the Dot Com boom and every other boom I have witnessed. I had a not so close acquaintance who worked for a local branch of a US tech company who was always boasting about how easy it was to make money. All you had to do was to borrow money and buy anything with dot com at the end of the name. I asked him on numerous occasions what he would do when the music ended and he said it never would and he was too clever to be caught. A few months later the Porsche was gone, as was the big house and the Harley.

There is little wisdom to be gained in having the same experience over and over again.

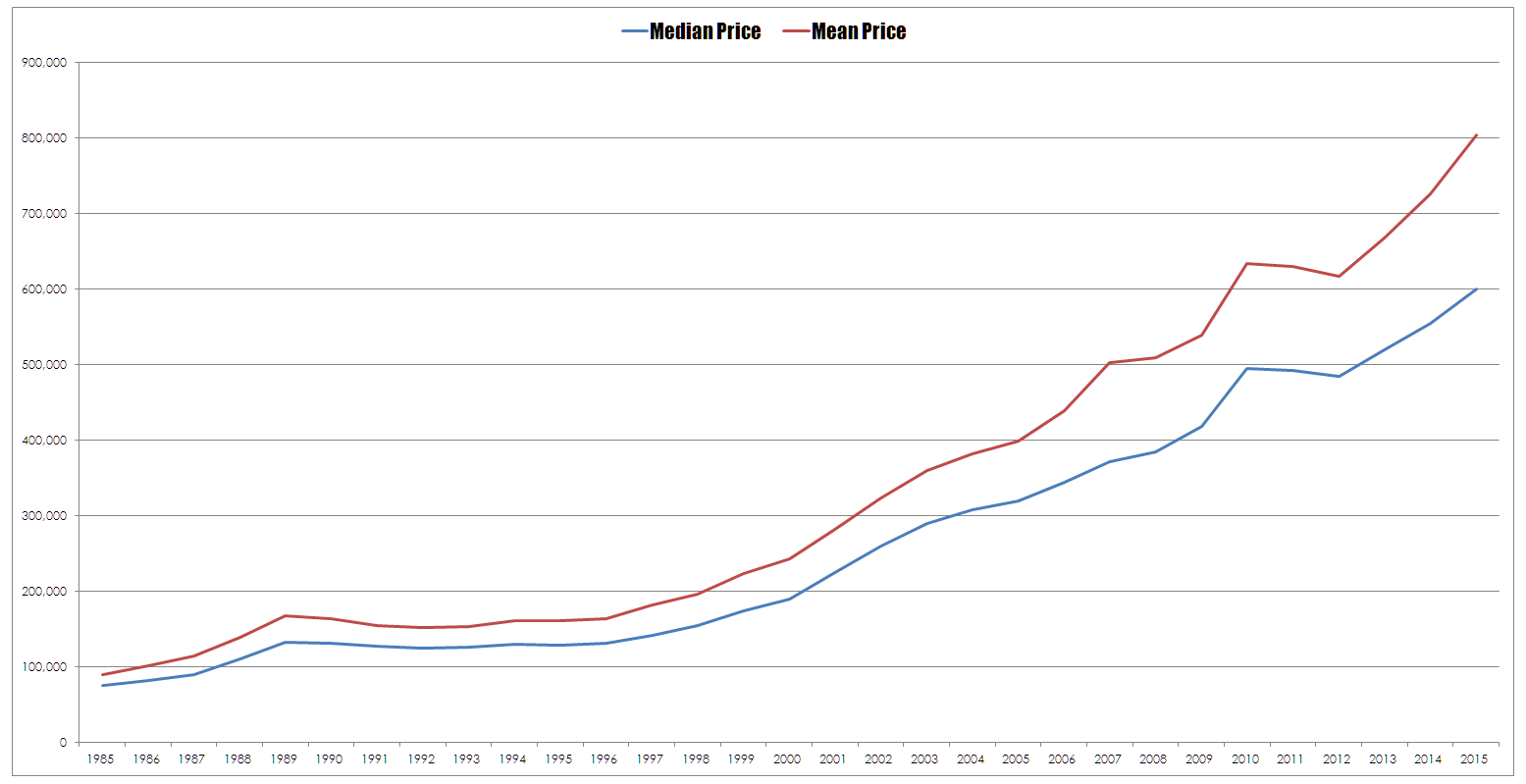

The second observation I made was the reference to the median price of houses. The use of the median as a measure where there are few outliers has always intrigued me. The statistical argument for using a median as a data point is that the average can be skewed by a few outlier values. When I was a student I had a stats lecturer who constantly laboured this point and for ever going on about the mathematician who drowned in a creek that had an average depth of three feet. When you have a series of outliers occurring with some regularity then the median is a better measure that the average. This is a particular problem in small sample sizes. However the best figure I could find said that in 2015 there were 63,133 home sales in Melbourne – this is not a small sample size.

Perhaps the answer as to why those involved in real estate choose to use the median price can be found in the picture that is presented when you compare average sale price with the average median price.

I have invested in property over an almost 25 year period , mainly in Sydney, and I can attest to lots of periods where property struggled along and achieved low or negative capital growth, sometimes for quite extended periods. From memory the early 90’s recession, periods of rising interest rates are a growth killer, the GFC period and probably a few others. At these times, the lack of liquidity of property and the relatively high overheads can be quite painful , not to mention extremely boring. Anyway , I agree with CT,most people only see the current boom , remember when the state government was offering first homebuyer grants and reduced stamp duty to STIMULATE the property market?

Humans suffer from the disease of forgetting the past so, as often is the case, are bound to repeat it; whether it’s the stock market, housing prices, gold, etc. Their mantra is always the same, “this time it’s different”.