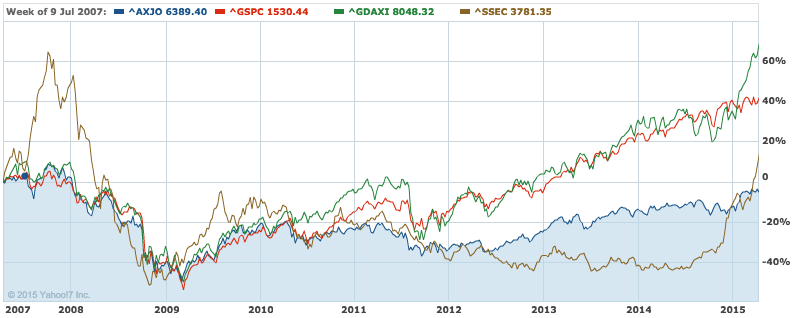

If you look at the performance of the broader Australian market since the GFC you see a market that has relative to other world markets been modest in its gains. The chart below looks at the performance of the S&P/ASX 200 against a variety of other markets. The lack of energy in the broader index is obvious.

However, markets nowadays are highly segmented into various indices, sectors and industry groups. This breaking down of markets for the most part simply generates useless data. However, it does on some occasions prove to be useful in that traders can drill down to see what is driving the performance of the market. Unfortunately, most market commentary particularly by the mainstream media doesn’t pick up on this segmentation and they merely quote what the broad index is doing. Taking a reductionist approach does tell you something about the quality and specify of a markets move. It tells you where the money is going.

Australian superannuation managers are awash with cash and it has to have been going somewhere. The chart below tells you where it has been going.

This is a chart of the ASX/S&P 20 which is much narrower index comprising the following companies. Its performance stands in marked contrast to the broader market.

AMP

ANZ

BHP

BXB

CBA

CSL

IAG

MQG

NAB

ORG

QBE

RIO

SCG

SUN

TLS

WBC

WES

WFD

WOW

WPL

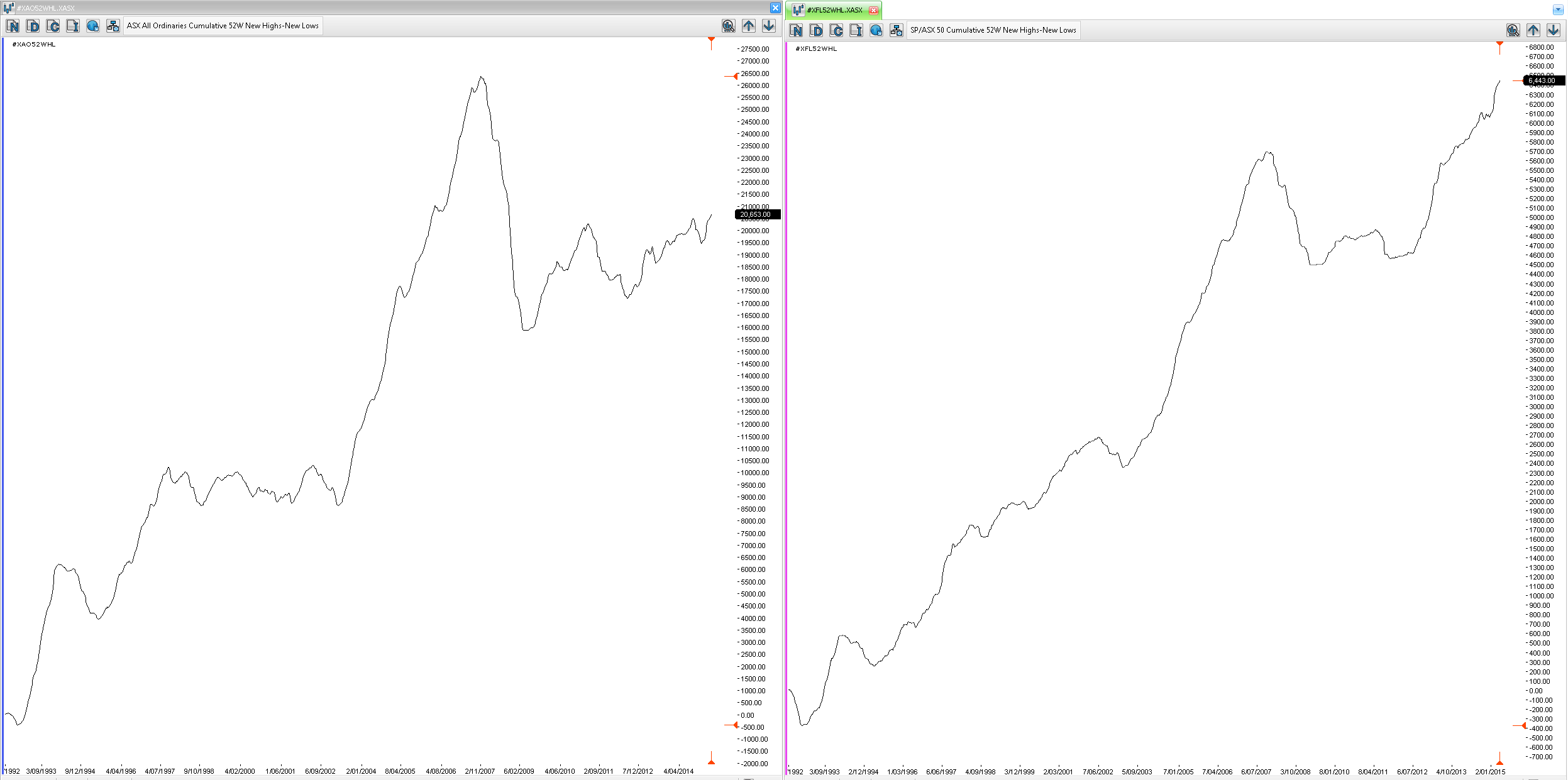

From viewing this chart it is easy to see where the money has been going. Australia has up to this point had a two speed market. The S&P/ASX 20 has been roaring ahead whereas the broader market has been meandering. This can also be seen when we examine the number of 52 week highs being made by the broad index versus a narrower counterpart. Unfortunately, I wasn’t able to drill down to the S&P/ASX20 so I had to substitute the the S&P/ASX50. Despite this use of a slightly broader index what is being conveyed to the trader is still interesting in that it again highlights the two speed nature of the market.

True stock pickers would already be alerted to this dichotomy in the market since only those stocks that are making new highs would feature in their selections. The situation would be harder for the so called value investor since it is likely that they would be buying stocks that are not moving. One of the great issues with value investing is the belief that your narrative is the markets narrative. This goes back to something I said on Talking Trading last week and that is the need to follow the money. Trading is simply about following the money – it is not about believing in your story.

")