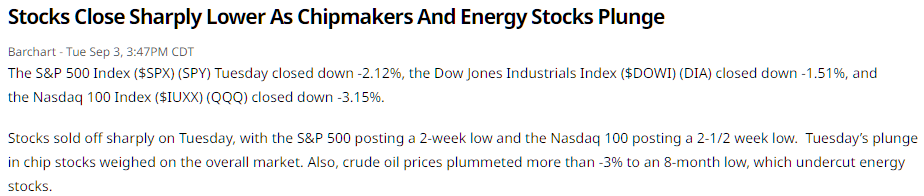

The snip below is of last night’s trading in the US along with a headline.

As you can see there is a little bit of handwringing going on. The onset of September has caused a variation of the following graph of monthly returns on the S&P500 to appear on various platforms. It shows that contrary to popular belief September and not October is the worst month for stocks – this observation has in turn caused many analysts to commit the cardinal sin of overlaying various time frames onto the current market and pronouncing that the market is going to fall by some catastrophic number.

As you can see there is a little bit of handwringing going on. The onset of September has caused a variation of the following graph of monthly returns on the S&P500 to appear on various platforms. It shows that contrary to popular belief September and not October is the worst month for stocks – this observation has in turn caused many analysts to commit the cardinal sin of overlaying various time frames onto the current market and pronouncing that the market is going to fall by some catastrophic number.

September is indeed on average a bad month for stocks. However, the fact that I have the phrase on average should immediately generate caution since averages are blunt and problematic. Consider the chart below that shows the error bars I generated for my version of the chart.

September is indeed on average a bad month for stocks. However, the fact that I have the phrase on average should immediately generate caution since averages are blunt and problematic. Consider the chart below that shows the error bars I generated for my version of the chart.

What it shows is that September could be down as much as 38.4% or up as much as 6.6%. Whenever you calculate or measure anything you need to have an idea of both the variance in your measurement and your potential for error. Without it, any chart you generate is fairly meaningless.

What it shows is that September could be down as much as 38.4% or up as much as 6.6%. Whenever you calculate or measure anything you need to have an idea of both the variance in your measurement and your potential for error. Without it, any chart you generate is fairly meaningless.

My observation is that September can be a really bad month, a modestly bad month or a reasonably good month. You won’t know until October.

")