I came across a piece titled The Best Ten Years Ever and being a student of market history I took more than a cursory glance. The article is filled with some very interesting charts based around the S&P500 and a series of metrics measuring performance. Things like this appeal to me because they offer a testable metric and I thought I would have a look at the Dow since I have data for the Dow going back to 1900. This makes for a nice deep data set. I looked at the returns for each year within a decade and then generated a value for $1 invested at the beginning of that decade. My 15 minutes of playing with Excel generated the following chart.

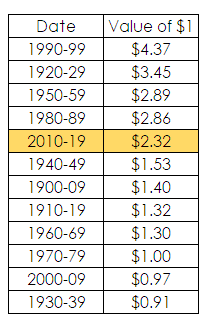

When you look at actual dollar returns a very different picture emerges – the past 10 years is far from the best decade ever using the Dow as our data source. The departure from the article in question is a little extreme and it did concern me so I included an extra year in the calculation of the last decade and it still only brings the result to $2.57. When I rank the decades according to performance we get the following.

The past decade only comes in at number five on our list with the standout decade being 1990-99. From a historical perspective what is interesting is that the decade of the GFC is on par with the decade post the 1929 crash. This gives an indication of the impact of the GFC on market returns.

This raises the question as to why the difference in conclusions when asking the simple question as to which is the best decade. In part, the answer probably lies in that we are measuring different things. I am only interested in the raw return – the journey is of no interest to me I am only interested in raw returns. How much and how quickly is what I am measuring. Undoubtedly if I was measuring drawdown and the number of new highs I may get a different result but then to my mind the definition of best is simply based around how much money do I have at the end of this best decade and is this amount more than other decades. Based upon this metric the past decade is far from the best.

")

Spot on, thanks for that. All the peripheral noise and results may be lovely data, but the whole purpose of what we are doing is what is in the bank. The only true measurable.

Cheers.