I came across the following definition of a trader the other day and it has been bouncing around the back of my mind ever since.

Trader/ˈtreɪdə noun: a person who loves problem solving and the challenge of competing against others

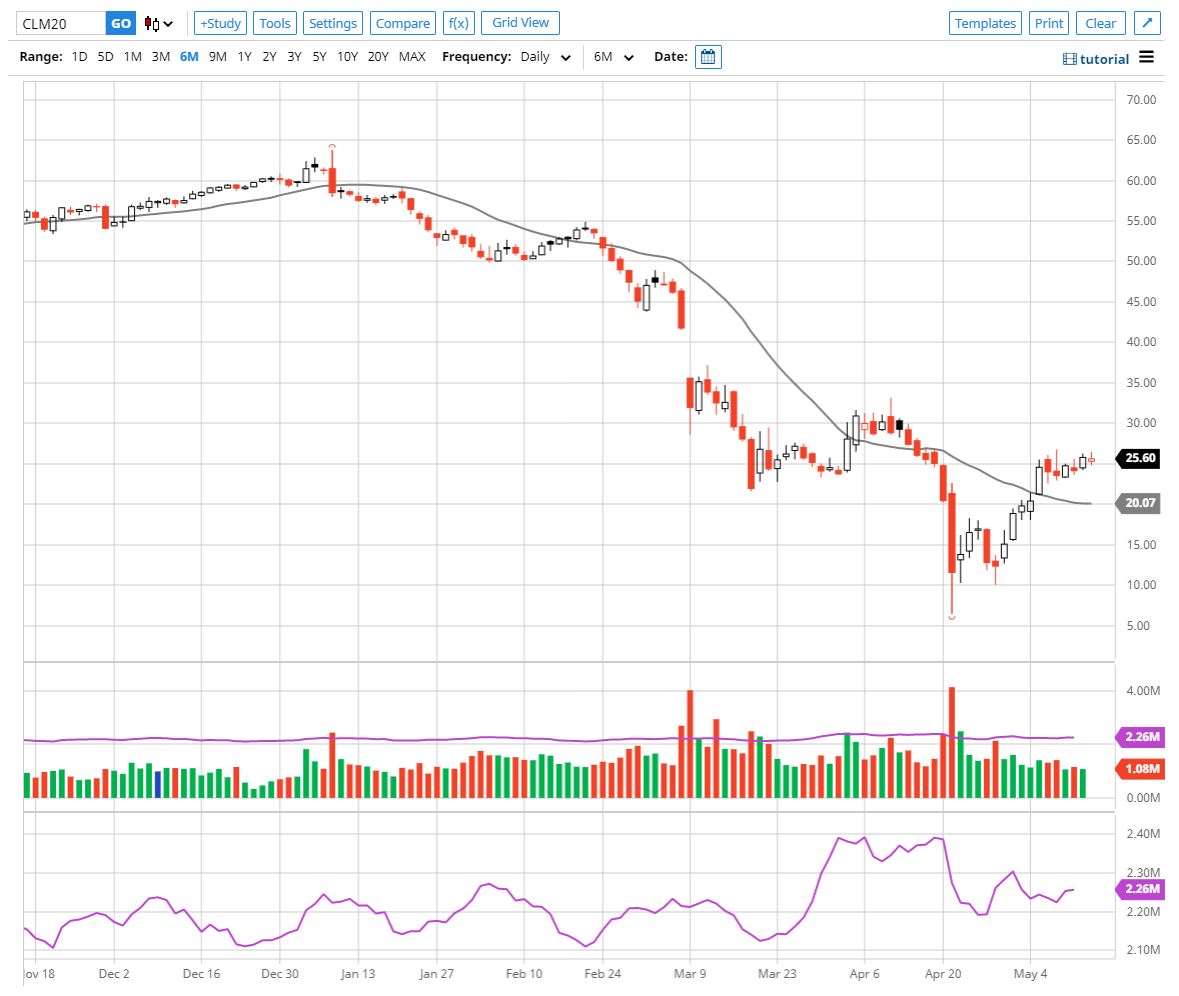

The first part I find some common ground with – there are some functional problems to be solved in trading but the largest and most important are those that reside within the trader. Let me give you a simple example. The chart below is of crude which I snipped from Barchart.com an excellent free site for various instruments.

One thing is obvious from the chart – crude has had a precipitous fall. It takes no special form of analysis to see this, any basic trend following tool you could apply would have told you that the price was in decline Add to this the knowledge that the world economy had lifted the handbrake and ground to a halt and you have no convincing reason to be long this instrument – the only logical trade direction is short anything else is delusional. Along the bottom of the chart I have plotted volume, in simple terms for every buyer there is a seller, granted in futures markets novation clouds this measure a little but in simple terms it holds true. As you can see there was no shortage of buyers. You could argue that given that this is a futures contract it may be traders to buying to close positions and that may be a valid point. But when we add in open interest we see that the number of positions open had a natural flow and hen accelerated in the first week of April. If price decreases and open interest increases then there is the strength behind the move down.

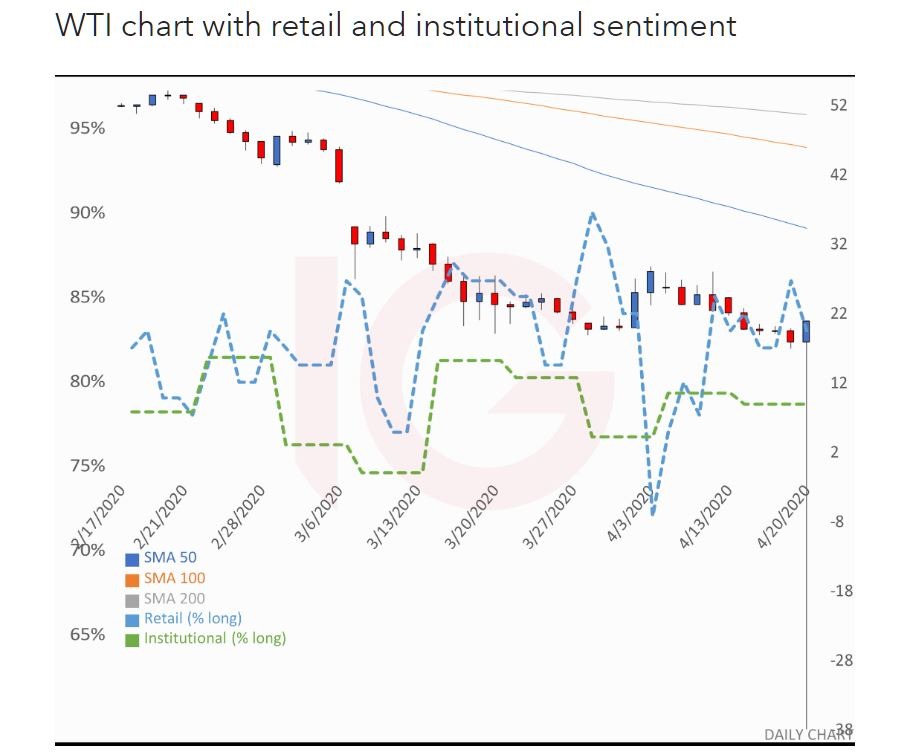

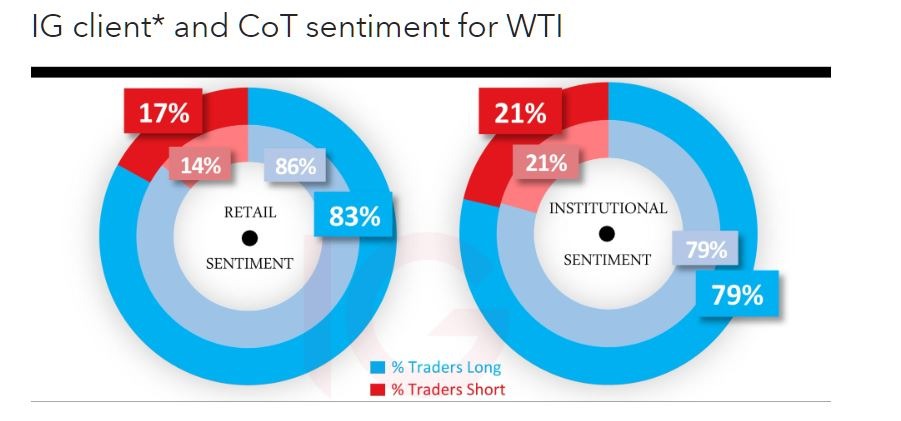

– Intriguingly most sentiment was on the long side. The following two charts were taken from IG Markets as the crash in price unfolded.

– Intriguingly most sentiment was on the long side. The following two charts were taken from IG Markets as the crash in price unfolded.

The green line highlights the percentage of institutional long positions in the market. You will note that as price crashed the level of long positions only briefly dipped below 75% and seemed to hold steady just above 80% for most of the time. The same insanity affected retail traders as well.

The problem solving is therefore not some great quantitative challenge – simple tools that are often free will suffice. The problem to be solved is you.

This leads to the notion of competition against others, there are a few problems with this both as a functional concept as and as a philosophical idea. The question arises who are you competing against. Competition against others implies that you are attempting to garner some form of superiority or supremacy in a given area. However, I would ask the question as to who is your actual opponent. You could argue that markets are zero-sum and therefore for every winner, there is a loser but this is not true in equity markets and not strictly true in other markets. If you buy a share at $3 and sell it at $5 then you might feel as if you have won something from the person who sold it to you at $3 but they might have bought it at $0.50 so in strict competition terms you are the loser because you made $2 on the trade whereas they made $2.50. So you need to be very careful about your definition of what constitutes winning and losing and if you cannot adequately define either of these two outcomes then the idea that you are in a competition with someone else collapses.

However, let’s assume that you can establish some criteria for winning and losing such as who makes the most money or who has the most fame within the trading arena. Your chances of running the worlds most successful quantitative trading firm, being a billionaire and having an equation named after you ala Jim Simons are pretty slim. Therefore you are a perpetual loser. Such comparison can do no good for the trader’s psyche as there will always be someone better than you.

Clearly, the competition is against your inner nature and the desire to do the wrong thing at precisely the wrong moment and it this competition that most traders shy away from because it is too hard. We lie to ourselves constantly and the lies we tell ourselves are the most effective because we know ourselves so well. Consider the charts above where the majority of both professional and amateur traders were long crude during the fall, consider the mental and emotional gymnastics they went through to justify these positions. If they dispassionately viewed someone else putting on the same trades in a similar scenario they would probably think they were insane. However, through the lens of their own experience and mental gyrations, they probably seemed to be the sanest thing in the world, if you asked them now as to why they were long a market that was clearly collapsing they could give you any number of justifications. Even after cratering their account they probably have any number of powerful self-justifications.

If there is a problem to be solved or a competition to be won it is undoubtedly an internal one.

")