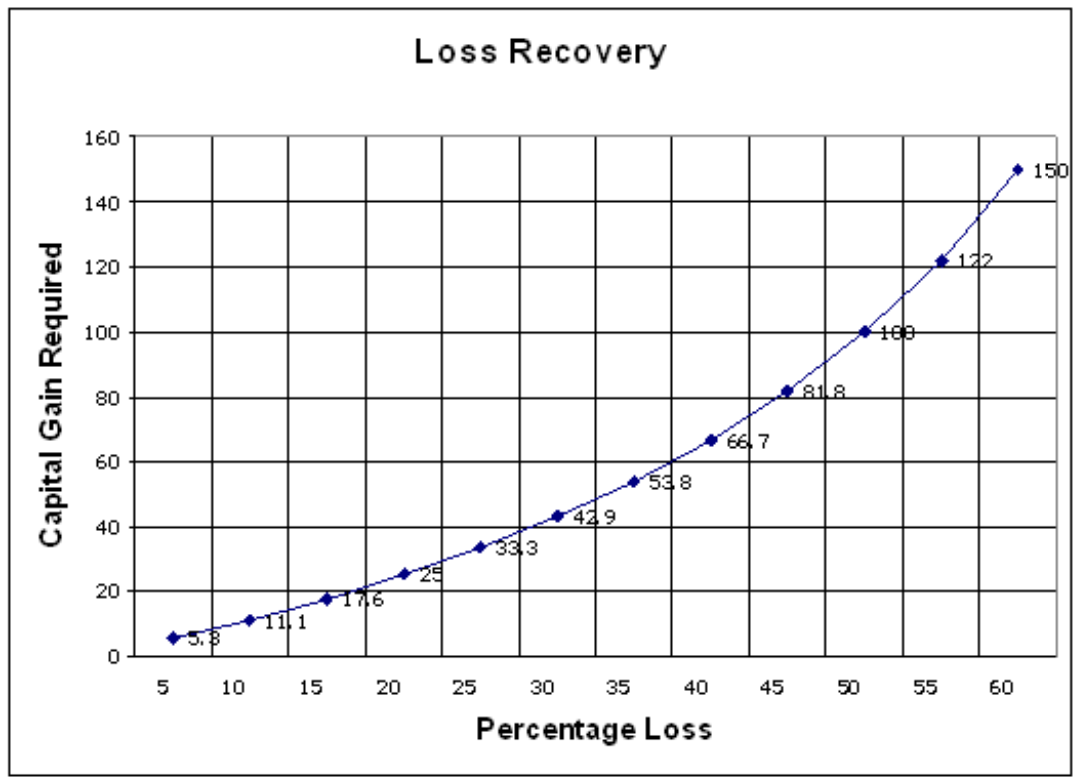

This old chestnut has raised its head courtesy of this article that dropped into my LinkedIn feed. You can read the article at your leisure if you wish. The basic conclusion it comes to is that market timing as defined by picking the perfect day on which to invest is not worth the risk.The article has what I would consider to be a methodological flaw in that its definition of market timing as picking the single best point in time to invest is incorrect. This is a common error. Market timing is defined as when not to be in the market because markets as you would expect have periods when they go up and periods when they go down. The aim is to have some form of mechanism that manages these periods of drawdown. It is important to manage these periods for a very simple reason as shown by the graph below.

Put simply a 10% loss cannot be recouped by a 10% gain on the remaining capital, it will take 11.1% to return to your starting capital. The shape of this curve is tremendously unforgiving, once losses get away from you your chances of recovery are fairly slim. The original article has several charts referencing the S&P500 Total Return Index dating back to 1989 so I have used this to assemble some data on the effect of missing periods of drawdown. The only difference in the data is that I have used monthly returns as this gives me more data points and a smoother curve so my numbers are a little different to theirs but this is an irrelevancy since we are looking at proof of concept.

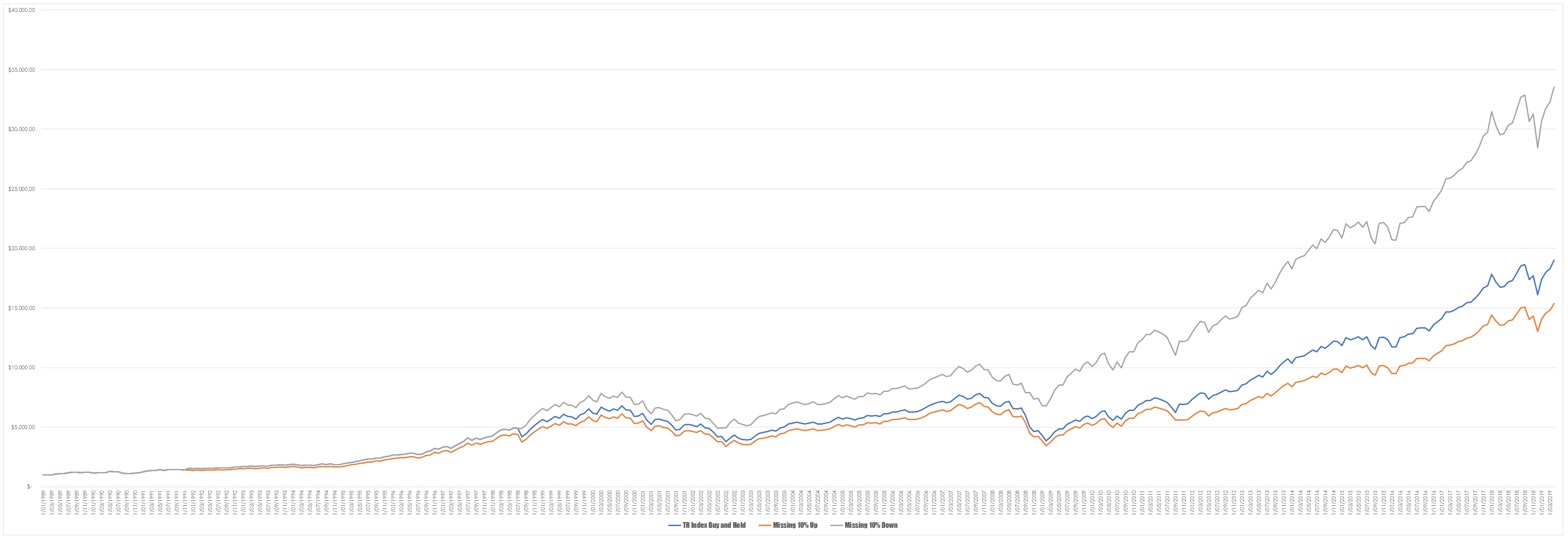

In part the argument against timing the market extends to the notion that if you are not in the market all the time then you miss the best periods – this at first glance seems to be a reasonable argument. However, remember markets go down as well as up and going down has a disproportionate impact uopn returns. Consider the graph below that looks at missing those periods where the S&P500 TR index went down 10% in a month versus going up 10% in a month.

We have a baseline in the simple return given by buying and holding the index which is shown in blue. Tracking below that is the effect of missing those months where the index went up by 10%, if I only represented these two lines you would agree that missing these periods has a detrimental effect upon performance. But this doesn’t give the full picture, the grey line demonstrates the profitability of a system that missing those periods when the market goes down by 10%. The level of out performance over the simple buy and hold is remarkable but it is also unrealistic because we cannot predict the future. We only know when these 10% months are by looking in the rear view mirror and whilst hindsight is the perfect investment tool it is also forbidden to us.

It is much more reasonable to look at using some form of filter to decide when and when not to be in the market, irrespective of what the pundits say it is not always a good time to be buying shares. In the past I have spoken about using tools such as cumulative highs and lows to get sense of the overall health of the market. These are robust, freely available tools that do not take you too far away from price itself. Unfortunately, the church that is technical analysis has over the years become less concerned with what price is actually do and more concerned with sunspots, astrology and arguing over whether you should set your RSI to 9 or 12. In graph below I have done something quite simple – I have run a moving average through the cumulative new 52 week highs and lows of the S&P500 index, when the index has dropped below the moving average I have exited at the end of that month and then reentered at the end of the month when price has crossed back above the moving average. For those months were we have exited I have assumed a move into cash and have a nominal interest rate of 0.5% which is well below the market rates at the time but the lower rate does account for our transaction costs and any slippage that you would encounter in real life.

The out performance of missing periods when the overall health of the market is poor persists over the long term and it would have been more marked if I had used the prevailing market rate of interest to bulk up the filter systems rate of return.

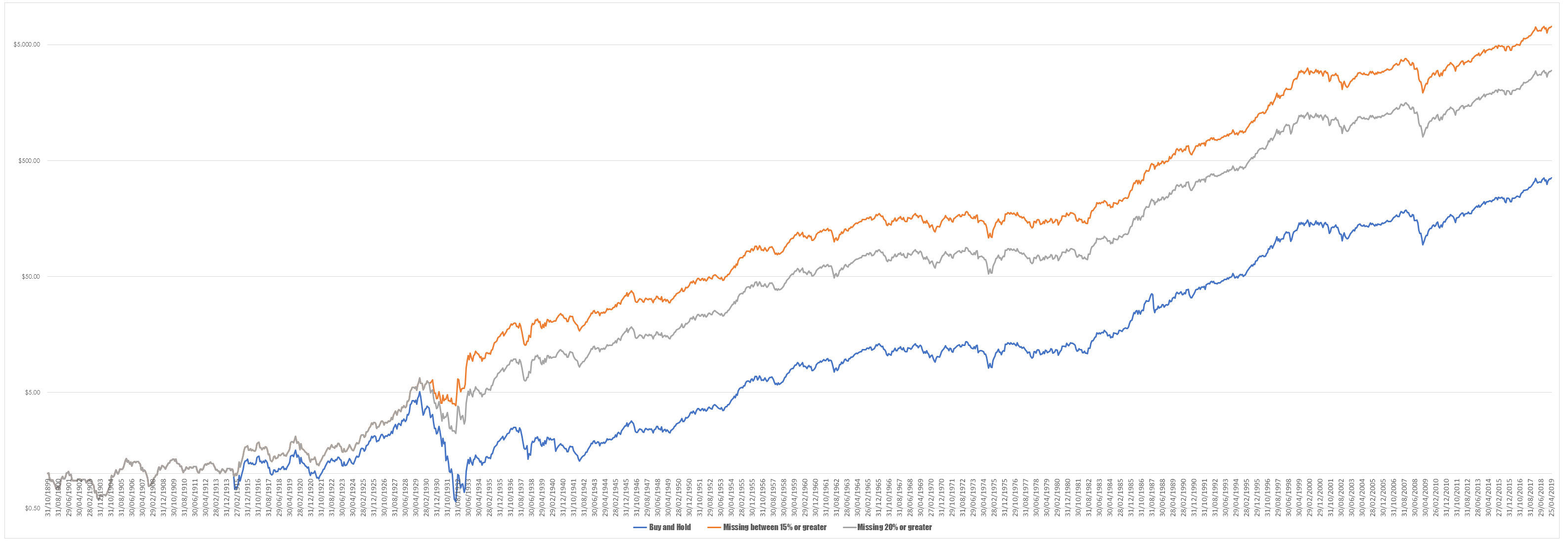

However, just to prove the point I thought I would look at the Dow because I have data going back over 100 years and since Excel was open I thought it would be fund to have a look at what the impact of missing poor periods would be, The graph below shows the impact of missing 15% and greater and 20% and greater against the baseline buy and hold model.

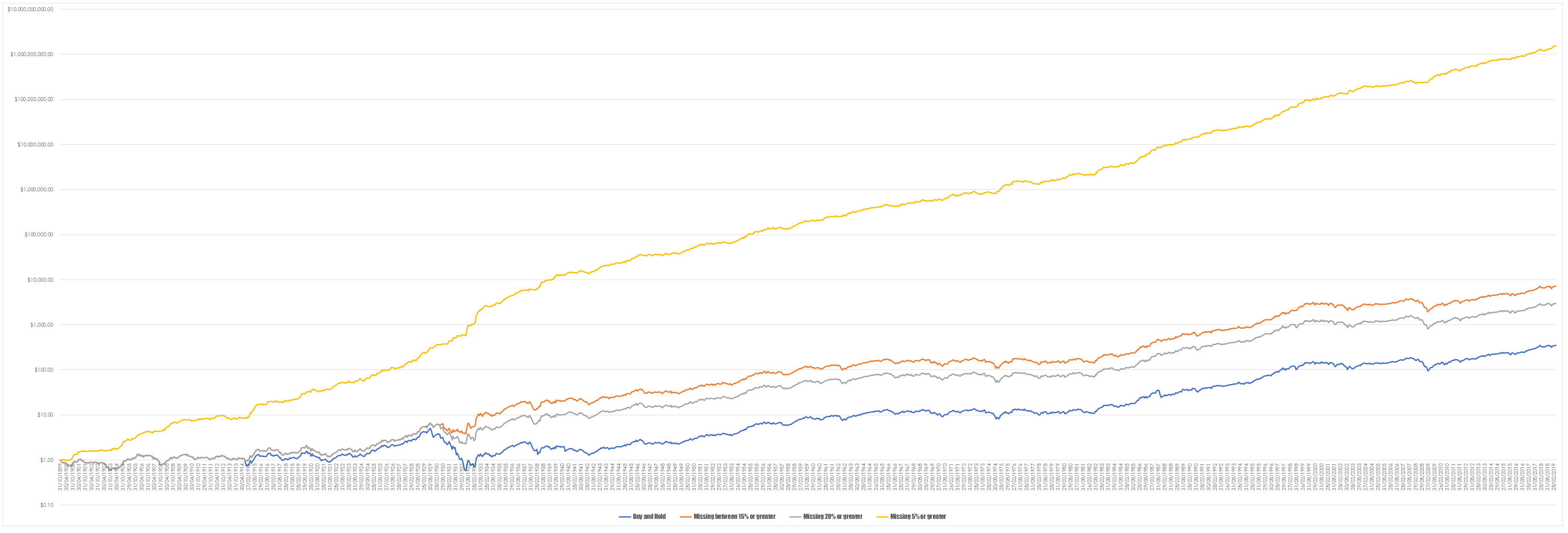

Once again there is no contest between buy and hold and trying to time the market. And since I had the data I thought it would be interesting to see what would happen if we had a crystal ball and could miss all those periods where the market declined for 5% or more in a month.

You will note that I have had to use a log scale to plot these because the buy and hold method generated $352.97 whereas the magic of missing all those periods where the market dropped 5% or more generated $1,523,816,879.42. Whilst silly in its execution in this example the point still holds true – losing money is more detrimental to an account than making money is positive to it. This is a powerful asymmetry that never goes away.

In finance there are lots of equations that traders/investors claim to be beautiful or essential to understanding how markets work. Some might cite the Black and Scholes model other cite posit the Capital Asset Pricing Model. In my world things are much simpler, if there were an equation I would want t traders to commit to memory it is the following –

G = L/(1-L)

G = gain need to recoup loss

L = loss incurred.

In decision making we are bounded by the constraints of time, quality of information and our simple cognitive powers – none of these three can be perfect. As such we are constantly making decisions on less than perfect information but this is where the prospect of reward for taking risk comes into play in trading. But if you have no money it doesnt matter how good your decision making you cannot play.

")