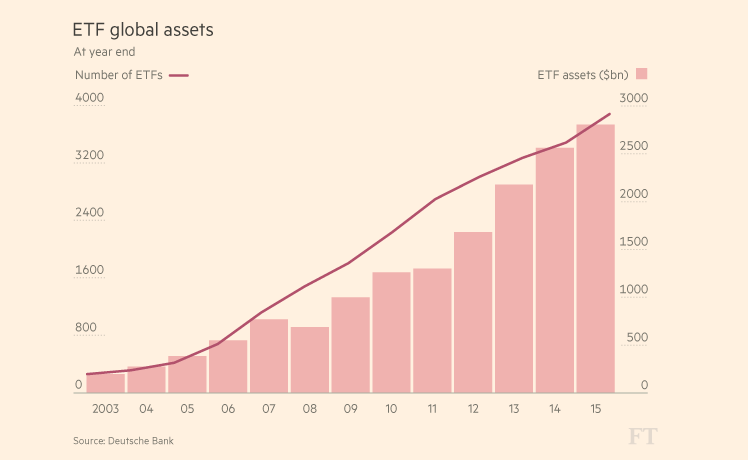

One of the joys about having been around since Adam was a pup is that you get to see lots of things come and go. On a regular basis you get to see what the new flavour of the month is and you quickly learn that there are no good or bad instruments just good and bad trading ideas. Over the past little while I have been watching the excitement around ETF’s reach some sort of gushing crescendo as apparently they are the saviour of every long term investor in the world. According to the hype all you have to do is buy and ETF and your retirement is assured. Unfortunately, one of the things you also learn with experience is that the world is a little more nuanced than that. Much of what is written about ETFs is correct – they are a simple low cost way to gain exposure to the market and their growth has been extraordinary as can be seen in the chart below.

Source: Financial Times

When we come to trade an instrument there are many facets to our decision making. Naturally we need some sort of trigger to spur us into action – this is generally some form of trading signal that has been derived from the price of the instrument itself. However, part of the trading process also involves deciding whether the environment for trading will be friendly towards us and enable us to enact all aspects of our plan in a friction less manner. It is at this point that we run into the very diverse ecology that is the ETF landscape.

Not all ETFs are created equal

In the trading process getting into a trade is generally fairly easy and the ease of entry reflects the relative lack of importance of entry as a requirement to successful trading. It is the ability to exit a trade with ease that over time determines our survivability as a trader. In setting benchmarks for the ease with which we can move into or out of positions we generally set a liquidity high water mark that has to be passed before we consider a vehicle viable for investment. This can be any number and in looking at ETFs in more depth I came across a report by a group known as Stockspot who produced a very handy little guide to local ETFs and I urge everyone to have a look at it. In their guide they rank ETFs on a variety of criteria one of which is liquidity and they set a benchmark of $500,000 per day as the minimum threshold. I find it hard to argue with this hurdle as a barrier to entry. However, I want to take a step back and look at liquidity more from the perspective of a business risk and for this I looked at AUM. From experience and observation it has hard to run a fund below a certain AUM figure – the expenses involved just don’t make it worthwhile and ETFs do face a business risk from the perspective of the mangers just quitting, which can and does happen. In addition to this you face an accessory risk with these exchange traded products and it comes from the manager inability to adequately manage their market making responsibilities.

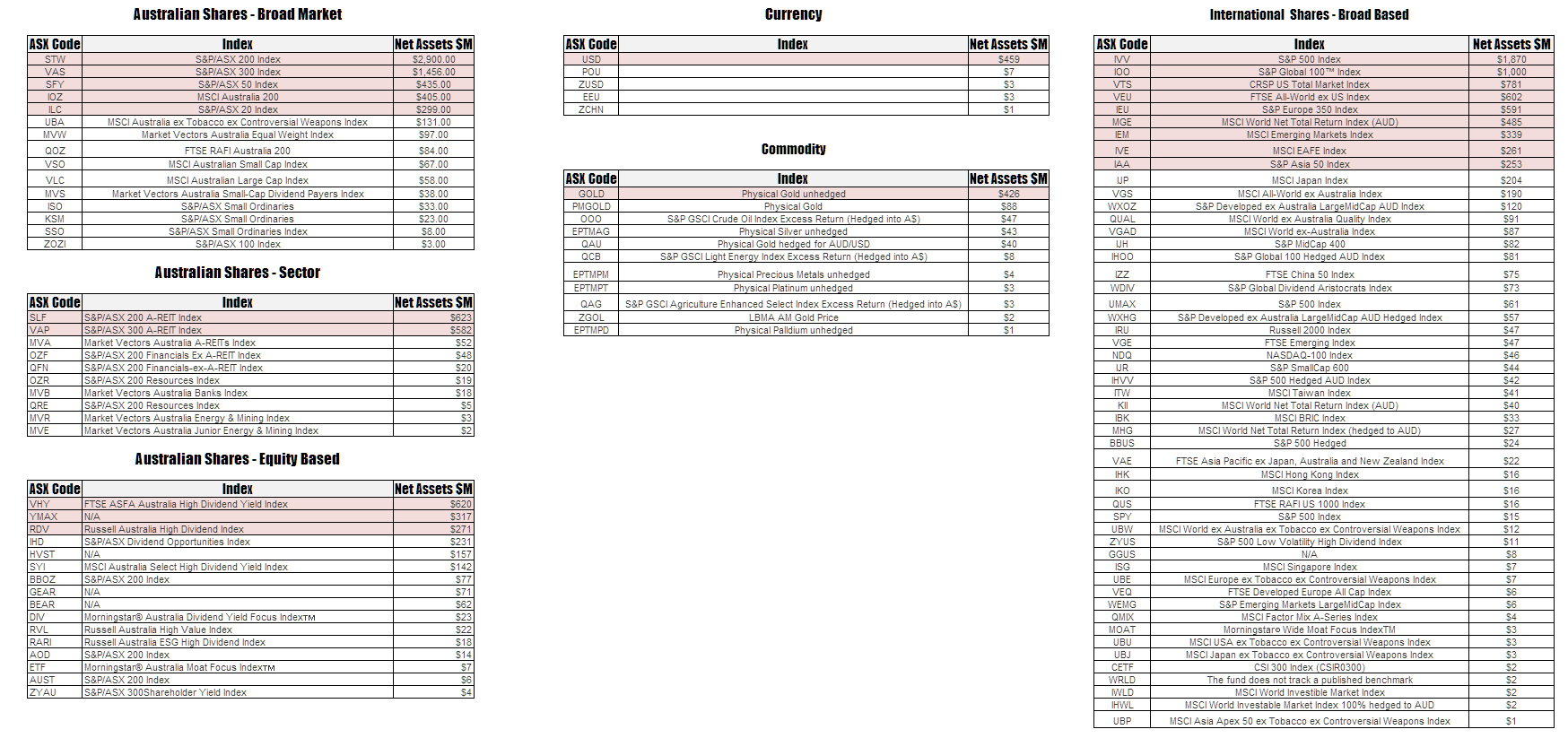

In the tables below I have ranked local ETFs on the basis of funds under management. If we use the general benchmark of $250M as a minimum then you can see that very few local ETFs hit this benchmark. The majority are way below it and a reasonable number would seem from my outside perspective to not be viable. (click for full sized image)

Beats an Active Manager

This point is true but with certain limitations – index based ETFs will beat on average a population of active managers. It is often stated that almost 86% of all active managers in the world under perform their benchmark index. Therefore, it seems to be logical to assume that investing in a low cost manner in the index itself would be more efficient and with regard to ETFs this point is true.

However, there is a small point that most miss. The ETF itself also under performs the index – this little point is glossed over by everyone. This occurs because of the nature of fees as they impact upon the growth of the ETF. Consider the chart below which compares the S&P/ASX 200 Total Return Index with the popular STW – there is a gap in their performance. This gap is a reflection of the cost of having someone else assemble a portfolio for you that matches the index.

This dislocation in performance persists throughout all market phases. This dislocation is known as tracking error. This error is never zero and it may be positive or negative.

What you see is not always what you get

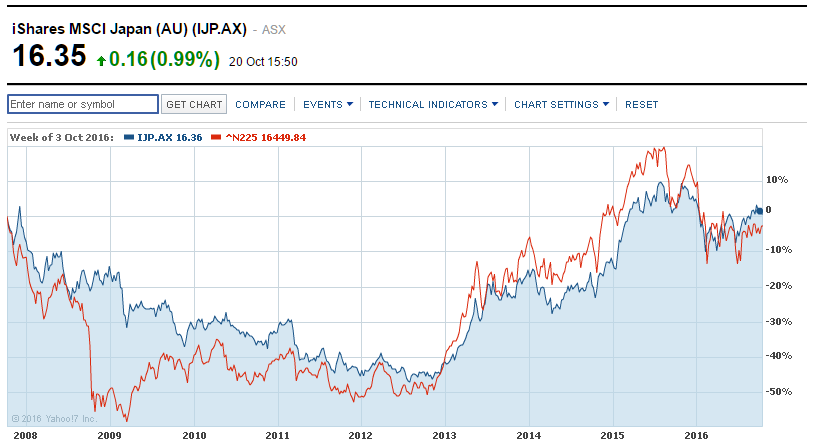

The notion of a simply buying and forgetting is not the path to riches that is portrayed. Imagine the following scenario, I take a view that is long the Nikkei and I want to exploit this via an ETF so I scan the available local vehicles and I come across IJP which I buy. Sometime later I look at the performance of the Nikkei and think I must be doing brilliantly and therefore my ETF must be doing brilliantly as well. Unfortunately, it’s not that easy.

If I had held my ETF from 2013 to 2015 I would have underperformed the market by a reasonable margin. The tracking error in this instance has come from the impact of currency fluctuations. During this period the AUD was broadly stronger against the JPY and this impacted the return on the fund. Over recent months this relationship has reversed and the fund has fared better than the index.

You don’t always just have one trade.

I am fond of saying that when you undertake any trade you are actually undertaking two trades. The first is the underlying instrument – the second is a trade on you. The metric for judging this trade is how well you followed your plan. However, with ETFs that track foreign indices the initial trade is a little bit more complex because of the impact of currencies.

For example consider the comparison between IVV.US and IVV.AU. These are essentially the same instrument but one is quoted in the US and one locally.

Despite the similarity you can see substantially different performance over the long term.

However, this brings us to a further problem which is more of a general trading problem and it has to do with the way results are presented. In presenting results the starting date is everything. In the chart above I have presented as long as view as possible. But if I compress the view to five years something interesting happens as can be seen below.

The relative performance changes with the domestic entity having superior performance and this new start date reflects the collapse in the AUD from 2013. The primary trade is simply being long the index; the secondary trade is the currency fluctuations that this trade naturally comes with.

You need to be careful in understanding where the performance is coming from. As a general rule you can tell when performance figures have been fudged because the system or idea seems to make money from day one. In reality what happens with trading systems is that they should all drawdown first and then start to climb. This occurs because well designed systems take their initial losses quickly; it then takes some time for the gains to accumulate.

It has oil in the name therefore…..

If I look at a list of the most popular ETFs by traded volume within the top five you will generally find United States Oil Fund (USO). This is by far the most popular vehicle by which people seek to gain exposure to the oil price and I am going to make one of the usual dogmatic generalised statements I am prone to make. Most of the people trading this vehicle have made an error and the error occurs in not understanding what they have bought and what it actually tracks. If I look at the definition of USO I see the following –

The United States Oil Fund holds near-month NYMEX futures contracts on WTI crude oil.

USO FACTSET ANALYTICS INSIGHT

USO, among the largest and most liquid oil“a great vehicle for riding short-term moves in crude prices” ETPs available, delivers its exposure to oil using near-month futures. USO’s huge asset base waves away closure risk, and its massive liquidity makes trading a snap. USO gets exposure to oil using derivatives, like all oil ETPs. Derivative returns can vary greatly from spot oil prices, but spot oil is uninvestable.

USO holds front-month futures contracts on WTI, rolling into the next contract every month, just like our segment benchmark. This method is particularly sensitive to short-term changes in spot prices, but can also result in heavy roll costs. That makes USO a great vehicle for riding short-term moves in crude prices, but long-term holders may want to look at other options.

http://www.etf.com/USO

There are two parts to this definition that need to be explored – the first is simple hyperbole and it is the bit that the majority of traders will focus on. In particular the following is attractive to traders –

USO’s huge asset base waves away closure risk, and its massive liquidity makes trading a snap. USO gets exposure to oil using derivatives, like all oil ETPs. Derivative returns can vary greatly from spot oil prices, but spot oil is uninvestable.

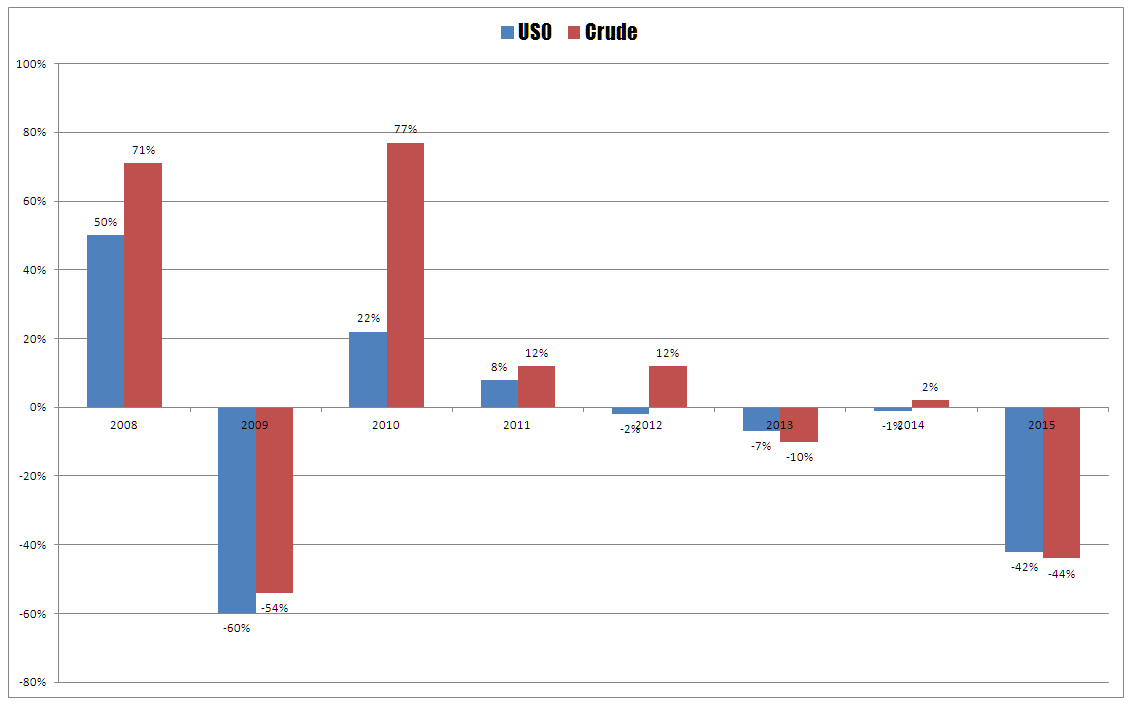

To get a sense of the problem with USO we first need to see if there is a problem, after all the marketing tells me that it is a great vehicle for riding short term moves in oil. Consider the chart below which compares the yearly return figures in the spot price of crude with those of USO.

As you can see there is a substantial difference and this difference is related to the second part of USO’s definition –

USO holds front-month futures contracts on WTI, rolling into the next contract every month, just like our segment benchmark. This method is particularly sensitive to short-term changes in spot prices, but can also result in heavy roll costs. That makes USO a great vehicle for riding short-term moves in crude prices, but long-term holders may want to look at other options.

USO holds front month contracts when these expire they have to be rolled over and in a market state known as contango these trades end up chasing price. To understand the idea of contango consider the prices below:

These are a series of prices for crude, as you can see the further out in time we go the higher the prices become. Contango is a natural feature of markets and doesn’t really imply anything other than market perceptions. Traders often think that contango is the normal state of affairs or reflects a normal market – this is not true. The issue for USO is a structural one, when a contract expires the next contract needs to be bought and this process is known as rolling, this rolling comes at a cost.

This lack of understanding of the mechanics of futures trading results in traders buying the wrong ETF for the right reason. In reality traders looking for longer term exposure should have opted for USL which looks to try and deal with the problem by only rolling one-twelfth of its portfolio. Alternatively, they could have opted for something a little more sophisticated such as trading XOP which handily outperforms both major oil ETFs as can be seen below. However, such a decision is dependent upon understanding the structural limitations of what you are trading.

Why has it not gone up three times as much?

The final point I want to make about ETFs is in regard to the use of leveraged ETFs. Traditionally these are ETFs whose name is prefixed by 2X, 3X or Ultra. The perception is that these vehicles will deliver a multiple of the return being generated by the underlying instrument and they can be either bullish or bearish in nature. The problem for traders comes in with the assumption that these tools can be held for more than a single day. This misunderstanding comes from failing to come to grips with what is actually meant by being leveraged and how the return is calculated. The returns are calculated on a daily basis therefore the assets of the fund are constantly being rebalanced so unless an instruments trends in the same direction day after day after day the gains made are eroded.

We arc back to a familiar refrain – if you don’t know what it is don’t trade it.

The wash up

The basic question that any trader needs to ask with regard to using any instrument is does it suit my view/approach/ philosophy and if it does can it be successfully integrated into my arsenal of instruments/techniques. As I stated in the outset there are no good or bad instruments only good or bad decisions and with instruments such as ETFs these decisions are often made on the hype of the instrument as opposed to its actual utility. For example much of the marketing around ETFs seems to fall into one of two categories. They are magic and will solve all your problems you just buy them and forget them and because they are magic you need a magic system to trade them.

With regard to the first point ETFs do fill a void in the market, they offer a low cost way of tracking an instrument when it is trending. There are limitations to this and there are potential sources of problems but if you are aware of them then they shouldn’t present any great issue. This leads to the second point about needing special systems to trade ETFs; all you need is to be able to follow a trend and this can be done with everything from a moving average to a series of new 52 week highs. Nothing special, nothing complicated.

Very informative thanks Chris ! 🙂

Chris

Thanks for the work you put into this.

Bill

Two observations, If you started early and had all your super contributions going into an ETF eg STW and not wanting to manage yourself but use that avenue thru your super fund. Then on past performance of the market it is likely you will do better than using a selection of growth or overseas investments via your super fund.

Second is if you were willing to set up a plan that actively trades the ETF STW, and you used the trend is your friend. Then with as few as 6-12 trades per year you could do even better.

But as always there is a kicker, the past is no guarantee that future results will be the same. Years of stagnation with little up trend are possible. But the results are still likely to do better than a lot of fund managers. As they say Float your own Boat.

As always, your timing is perfect. I was just doing some study on these late last week. This has helped a lot. Thanks.

Nice article Chris and thanks for the mention of our Stockspot ETF Report which we put a lot of effort into each year.

Just a note on the comparison between the STW ETF and the S&P/ASX 200 Total Return Index. The main component making up the difference between these charts is actually dividends since the total return ETF includes dividends whereas the ETF reflects the ex dividend price only. Assuming a ~4.5% yield over the past 6 years that would bring the 2 charts closer by about 27%. As you’ve mentioned, the remaining difference would be made up of a combination of tracking error and fees. Just thought I’d clarify since a 32% tracking error would be enormous for a broad equity market ETF & investors would be suitably outraged if this actually occurred.

Regards,

Chris from Stockspot