Traders are often afflicted by many psychological maladies, foremost amongst them is their remarkably short memories. This is particularity true on the sell side of the industry where those flogging various products seem to have the attention span that is worse than a goldfish. Allied to this is the basic thickness some people have when it comes to understanding what they are trading. Throw all this into the mix and you have a recipe for disaster such as the one that is unfolding with inverse volatility ETF’s. Before getting into the nitty gritty of what is unfolding and the consequences for those on the wrong side of history it is worth back tracking and explaining the various instruments involved. An ETF is a reasonable easy instrument to understand – they are simply a basket of instruments that are covered under the umbrella of a fund. For example STW is an ETF that covers the S&P/ASX 200. This means that the fund owns all the shares that make up this index in precisely the same ratio’s as within the actual index. The fund then offers this basket to individual investors in much the same way that any listed company offers an investment to retail investors. So instead of buying CBA and owning shares in a bank you own STW which is a fund that invests in the index. How your investment does in reliant upon how the index performs These sorts of ETF’s are broadly known as being vanilla – that is they are basic in construction and are easy to understand. If you understand how an index fund works then you understand how this sort of ETF works.

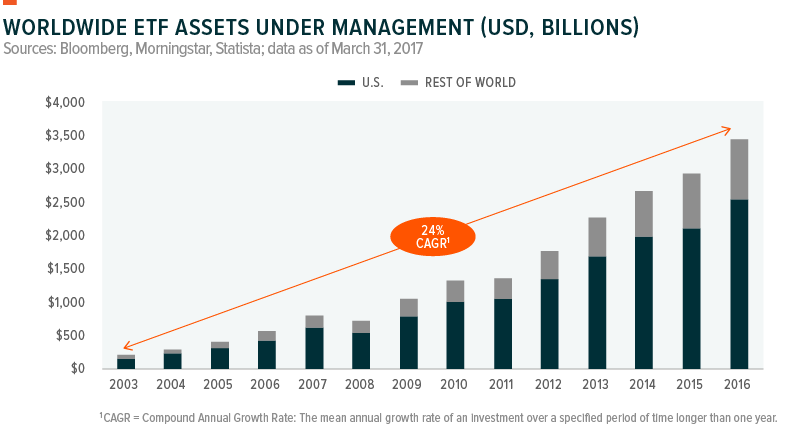

However, the folks who bring ETF’s to the market are nothing if not creative, this creativity has seen an explosion in both the number of ETF’s being created and the size of the overall market. This explosion has been extraordinary as seen in the chart below.

Source – Global X

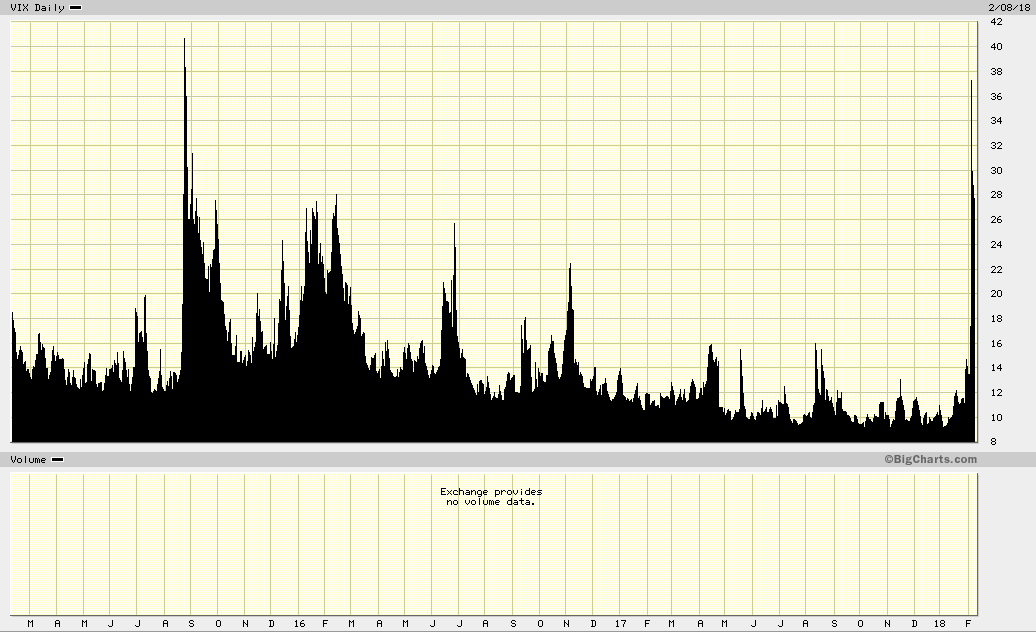

As the ETF market grew anything and everything became the subject of an ETF – it didn’t matter whether it was an index, a commodity or even a made up index. Where there was the smell of money there was an ETF provider and this is where the current apocalypse in inverse volatility ETF’s had its genesis. A volatility based ETF combines two wonderfully combustible complements – volatility and leverage in the form of having to hedge via a futures market. The recent move up in the US market has been characterised by an interesting lack of volatility – up until recently the market had gone some time without a correction of 5% or more. This complacency was best exemplified by the almost lifeless corpse of the VIX. The VIX is sometimes given the somewhat misleading name of the Fear Index. In reality it is the markets expectation of the future volatility of options traded over the S&P 500. It is possible to rearrange option pricing mechanism to generate a perception of future or implied volatility – this is important for option traders because the price of an option and volatility share a linear relationship. As an options trader – particularly a market maker who grants options getting this equation wrong can be fatal. Hence, this metric is very sensitive to changes in future perceptions of volatility. It is at this point that the notion of traders having short memories comes into play. A perception had settled into the market that since the past few months had been a time of exceptionally low volatility then the future will be exactly the same. These conditions enabled what are known as inverse volatility ETF’s to do exceptionally well. An inverse volatility ETF is exactly as the name implies – it bets on the inverse of a move. So an inverse volatility ETF is based upon the premise that you can and do profit from a low volatility environment by purchasing the ETF. The longer this environment persists the more profitable the vehicle becomes. As such these instruments were all the rage – right up until the time they imploded.

The most extreme case at present is that of VelocityShares Daily Inverse VIX which over the past three days has effectively ceased to exist.

ETF’s that rely upon moving into futures markets to hedge themselves encounter some unique problems and in the case of this ETF actually seemed to aid in their own destruction. Imagine you are the manager if this ETF and you see volatility moving against you, to compensate for this you have to go into the market to hedge your position. The problem is the very act of you doing so in a market like the VIX actually makes things worse and price moves further against you. And all this is occurring against the backdrop of a market that is already suffering from volatility spikes and seems to be in the middle of sharp correction. It is as someone who is on fire is attempting to put the fire out by pouring petrol on themselves.Who ever thought anything could go wrong with this sort of arrangement.

The destruction of VIX based inverse ETF’s has caused a great deal of consternation among various investors but there are a few things that need to be pointed out. These ETF’s did exactly what they said they would do. In times of low volatility they enabled investors to profit. Nobody whinged as XIV made its way from $20 to $150 – they are only complaining now because they made the assumption that what happened last year would happen this year without any regard to history. If you look at the chart of the VIX below you can see that it is prone to shocks. Volatility is not a static entity and when you are basing your investment decisions upon the perceptions of others and that’s all the VIX is – it is perceptions. Then you are asking to be belted at something in the future.

Simply looking at an overlay of the VIX and XIV would have told you that when volatility spikes then the value of your investment falls so you best have a plan for when that happens. Its not rocket science.

")