One of the frustrating things about being a trend follower is that it takes time to overcome the inertia of a new system, particularly if that system is based upon slightly longer time periods such as weekly data. Part of the frustration that traders encounter is based upon the simple mechanics of how systems work. A system that is correctly designed takes its losses quickly and allows its profitable trades to simply roll along. This results in the system instantly going into drawdown and it is this drawdown that causes traders to develop friction with their system. This friction often leads to tinkering as they attempt to force the system to give them something it cannot give. This is exacerbated in times of a flat market – you cannot force returns from a market. The All Ords of late has not really been a stand out performer as can be seen from the chart below the market has been slowly grinding its way up in a broad channel.

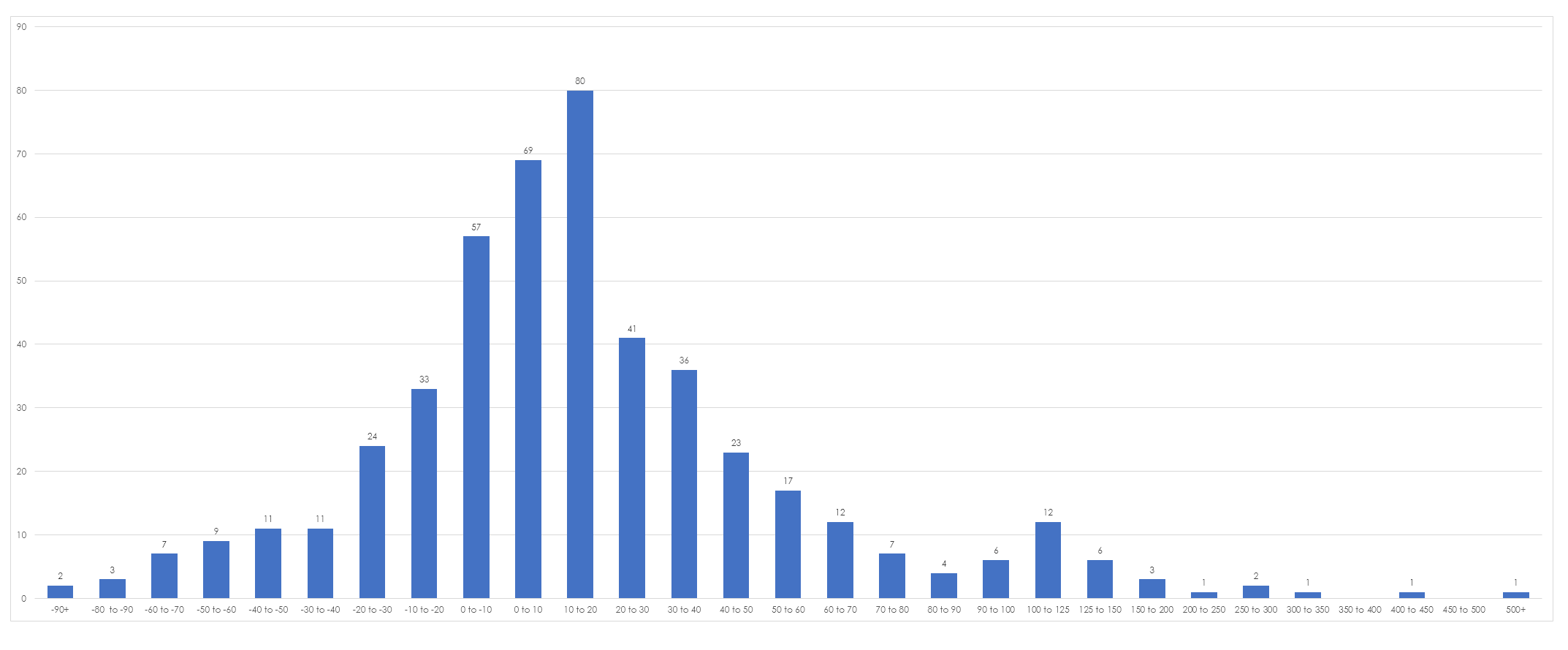

With this in mind I thought I would look at the yearly returns for the various stocks within the All Ords – so I found some data on their percentage returns and stuck it into a frequency histogram to see what the performance of individual stocks looked like.

I have a arranged the data into a serious of blocks and did a count of the number that fell into that category. I also calculated the average performance of the group which for this period stood at 17.09%. However, if I drop out the 200% and above outliers this average value falls to 13.04%. As you might have guessed the majority of values cluster around the mean with a long right handed tail. This sort of distribution is common with stocks since we have unlimited upside but limited downside – a stock cannot decline more than 100%. Our psychology dictates that we are instantly drawn to the right hand side of the chart and the extreme outliers that occurred over the past year. And as traders these are the sort of trades that we hope ours might evolve into. However, in doing so we ignore that left hand side of the chart. The majority of stocks (60%) have below average performance. You may assume as a trend follower that this is not an issue since you would avoid these large losses and poor performance by the use of stops but that ignores the reality of the actual trading process. As a mechanical trader you will not incur these losses but you will burn time wading through these non performing stocks before you hit the ones that do perform. You waste time, a little bit of money and a lot of patience dealing with this mediocre performance.

My anecdotal experience has been that trading returns are made up of a lot of modest returns and a tiny handful of trades that do very well but to get to the ones that do very well you have to crank through a reasonable number of trades and you have to keep going. This is where the notion of emotional resilience comes into its own in trading and the ability not to tinker with the system hoping that it will generate these sorts of trades. Systems dont actually generate these sorts of trades – the market does so you cannot actually build a system with the preconceived notion that it will find you trades that generate a 500% return. What the system does do is generate a population of trades, most of which will be duds and hopefully a few large winners. But in the beginning all trades look the same.