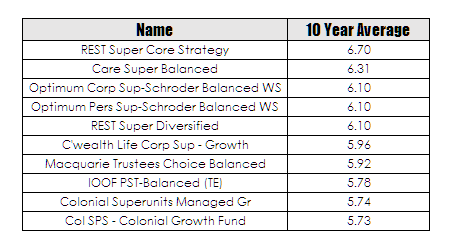

I noticed during the Olympics that an industry superannuation fund known as REST were trying to convince me how good they are. The catch cry of the ad is that investing is a marathon and not a sprint – you wont get any argument here on that point. Too many people believe that investing irrespective of the approach used is somewhat akin to winning Tattslotto. According to REST one of their funds had been ranked number one over a ten year period versus all their competitors. Bold claim I thought so it was time to fire up Google, find a source of data (Morningstar Funds Rating) and drop some data into Excel and see if this claim was true. Lo and behold it was. Their growth strategy fund was ranked number one with an average ten year return of 6.70%. I have dropped a table of the top ten funds in below.

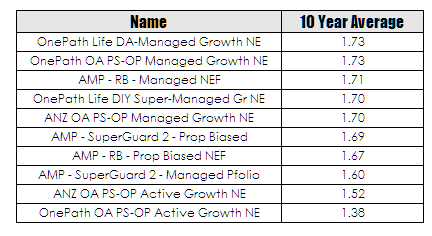

As you can they show their competitors a clean pair of heels. There is only one problem, during the same period the market returned an average of 8.1% so whilst REST’s boast is true in that they did outperform their rivals they like all of the 345 other funds in the list I have managed to under perform the market. Their claim of being number one is a little bit like claiming your are the tallest of the seven dwarfs – you may be the tallest but you are still a dwarf. Remember this is a growth fund – it is supposed to do better than the market not worse. Looking through the data I had got me thinking about the worst performing funds and I have dropped a list of these below.

As best as I can figure the average rate of inflation for the past decade has been about 2.4% so these bottom performing funds have made no return for their members. In fact about one in seven funds seemed to make no effective return over the last decade and it seems as if the most frequently occurring bottom of the league table funds are ANZ based funds.

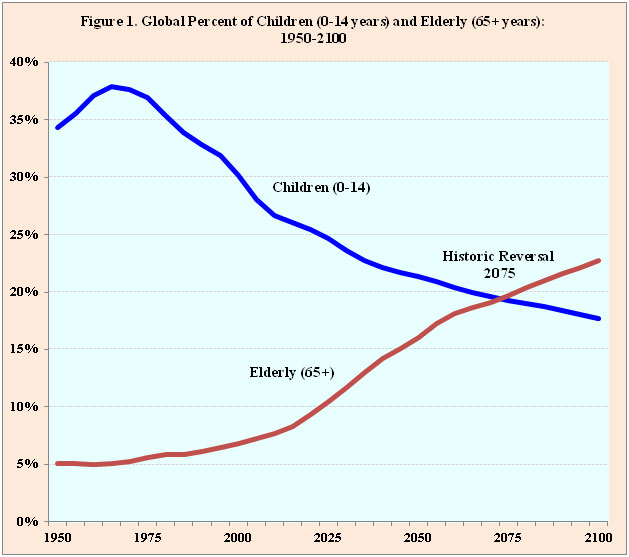

My dislike of the funds management industry is no secret. From my perspective it is hard to find an industry that is so richly compensated for being so bad at their jobs. But there is a much wider issue at play here and it relates to the distribution of the old and the young. Data released during the week from the United Nations Population Division show that we are on the cusp of an historic reversal in the ratio of those over 65 to those under 65. They estimate that crossover will occur in 2030 in Australia.

The report states –

In the year 2000, there were already 27 countries with an ageing index above 100, 17 them were in Europe except Japan. In six countries―Bulgaria, Germany, Greece, Italy, Japan, and Spain―the index was above 130 persons. In that same year, the ageing index in 18 countries, mostly in Africa, was below 10. By the year 2050, there will be more than 3 persons aged 60 or over per child (ageing index above 300) in 10 countries or areas, including 1 from the less developed regions, China, Macao SAR. In Italy and Spain, this ratio is expected to reach nearly 4 older persons per child (ageing index above 360). At the same time, the index is projected to remain under 25 (more than 4 children per older person) in 16 countries or areas, mostly in Africa.

The mechanism by which we fund our ageing population is of national importance and the current superannuation system is in no way assisting in solving this problem. It is impossible for retirees to fund their retirement if they lose decades of performance. Whilst I cannot give advice if I were employed and forced to take on superannuation I would opt for the lowest cost index linked fund I could find. Its not perfect but it is certainly better than the alternative.

In fact if it were up to me and I was feeling particularity grumpy I would nationalise the entire industry and drop everyone into a zero cost index fund.