Why Is It So Hard?

I got flicked an article from a few weeks ago from the AFR that was titled Brace for 5pc super fund returns and the cynic in me instantly assumed that the majority of funds were going to lift their returns to 5%. For some, this would mean doubling their long term rate of return which would be a welcome surprise to their investors. This does raise the question as to why funds are so bad at their job and why their employees manage to keep their jobs. Imagine being a pilot where you failed to hit the end of the runway 90% of the time you were in the cockpit – your career as an aviator would be short-lived indeed.

However, there are a few reasons why the fund management industry is so poor at what it does and the following reasons are not really in any order of importance.

- The managers have no skin in the game, that is their remuneration is not tied to the performance of the fund. In my view, fund managers irrespective of seniority should be paid a base salary that is enough to keep the lights on and the rest is in the form of bonuses linked to the performance of the fund relative to a benchmark. It is quite easy to establish these benchmarks and it is easy to defeat any short term thinking that might creep into the investment process in an attempt to game the bonus system. The bottom line is no performance no pay. Alternatively, force all employees to invest their own superannuation/excess funds into the firms own funds. That should soon concentrate the mind.

- Funds tend to rule by committee that way responsibility is abrogated to the group and not the individual. If your performance is poor then it is simply a corporate responsibility. This is also easily defeated by splitting your investment teams up and forcing them to compete with one another and once again pay is linked to performance. This way a high performing team or individual is not subject to the broader idiocy of the group.

- Re-educate staff to understand that their job is to offer raw performance, it is not to offer platitudes about the efficient market hypothesis and how hard it is to beat the market. Points 1 and 2 should also reinforce this as an overall cultural imperative. The aim should be to be noticed or your performance not hide behind the mediocrity of the entire industry.

- Hire people who do not have a business degree and whose mindset has not been polluted by either classical economics or finance theory.

- Sack all your economists or retrain them to man the pop-up coffee stand in the lobby of your office – at least that way they can do something useful.

However, I put the likelihood of any of this happening as zero since the industry is too entrenched in its own way of thinking and doing. It is impossible for them to see that other people do things not only differently but also better. If they did opt to hire people from outside the industry I have more than a few candidates I could put forward who would move things along nicely. In this weeks Talking Trading, we feature a Mentor Program graduate whose returns would embarrass any fund manager being paid a small fortune. Likewise, consider the results below which also come from another one of the program’s graduates.

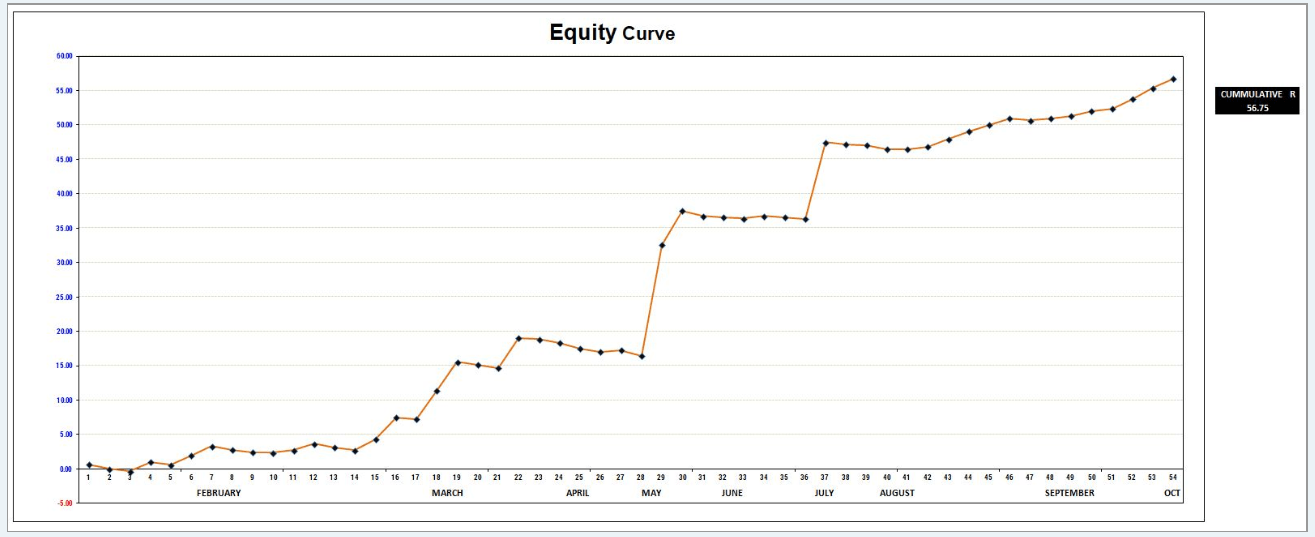

This chart looks at the cumulative R return on the account. For those who are unfamiliar with the term R, it is measure an accounts return measured as a function of its risk. R is traditionally based at 1 so if you had an account that was valued at $100,000 and you were risking 1% this $1,000 in risk is referred to as 1R. If you took a trade based upon this and the trade returned a profit of $3,000 then the trade is said to have returned 3R. The return is measured as a multiple of risk.

The cumulative R for this account YTD is 56.75. If we were to put numbers this to give it some perspective it means that if this trader had an account of $100,000 and was risking $1,000 then their account would be up $56,750 or 56.75% this year. I watched this system being developed so I am very familiar with its workings and I know that once implemented it takes a few minutes each night to run. Remember back to the opening item from the AFR where superfunds are being urged to impress upon their clients that they may be lucky to make 5% this year. It makes their returns look somewhat mediocre.

This does raise the question of what makes these systems special and the answer outside of being exceptional is not much. They are simply the result of having a system applied ruthlessly with hard work, application and a constant desire to move forward and above all not to accept mediocrity.

")