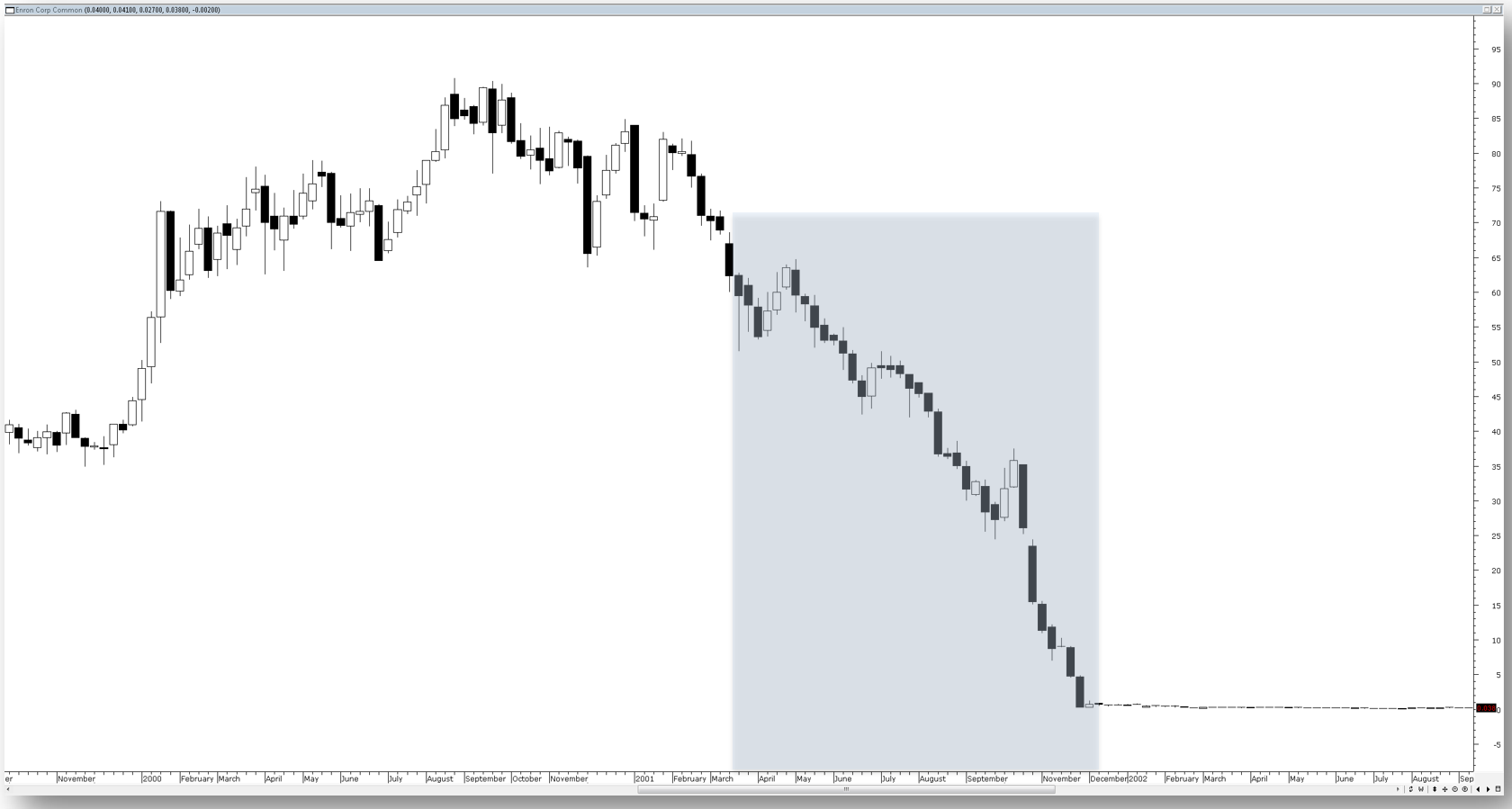

A comment appeared in relating to this piece I wrote the other day and it deserves a fuller explanation. I will state at the outside that it is my contention that if you listen to the financial media and the sell side of the finance industry you will never get anywhere. And as a first step I recommend that everyone read Where Are The Customers Yachts by Fred Schwed. Now approaching its sixth decade it is still profoundly relevant. In terms of broker advice as a source of recommendations upon which to build your wealth I thought I would look at an extreme example – Enron the US energy trading company that was in essence one giant scam. The trajectory of Enron’s share price can be seen in the chart below.

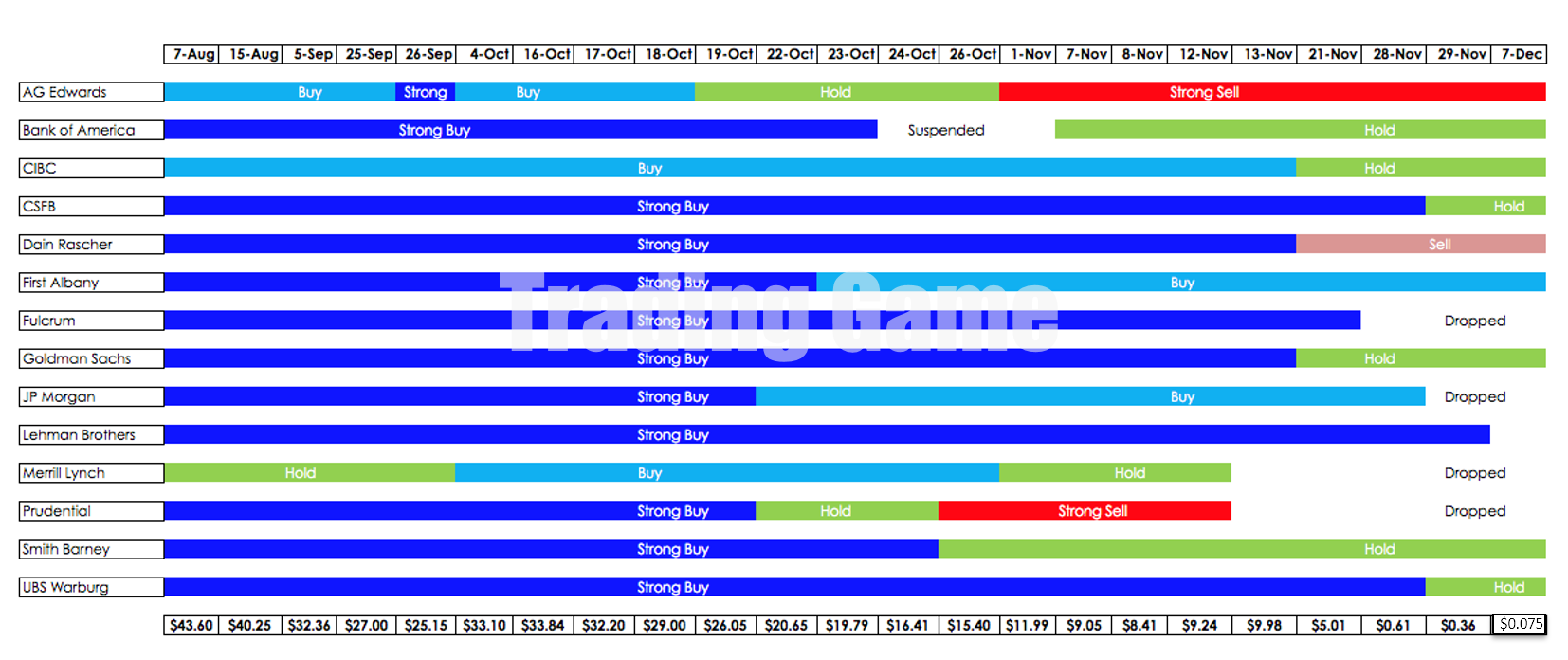

As befitting a company of Enron’s size it was covered by numerous brokers and you can see in the chart above I have highlighted the decline in Enron’s share price – this decline coincides as you would expect with it becoming known that Enron was a scam of massive proportion. The table below looks at the recommendations offered by brokers at this time. This table has a few components, on the left are the names of the brokers offering the recommendations, in the centre are the recommendations themselves. These are colour coded as to the type of recommendation and along the bottom is the price at which these recommendations were made. When viewing this table keep in mind the chart above.

As you can see for the majority of the decline Enron was either a strong buy or a buy for the majority of brokers. Even after it became common knowledge that Enron was a fraud and was under investigation by the SEC brokers still continued to recommend it. In fact as it disappeared it was still considered to be a hold. So let me state that again – even after it was known that Enron was a giant con job and was headed down the toilet brokers still continued to recommend it. The most perceptive observation on this situation was actually offered by the humourist Dave Barry –

Wall Street relies on “stock analysts.” These are people who do research on companies and then, no matter what they find, even if the company has burned to the ground, enthusiastically recommend that investors buy the stock.

Dave Barry

February 3, 2002

This quite naturally raises the question as to why this sort of thing occurs and the answer can be found in the structure of the finance industry. In very broad terms what people generally refer to as stockbroking has traditionally been split into two very broad camps – corporate advice and retail advice. Corporate advice covers high end activities such as capital raising, mergers, and company listings. Retail advice covers telling people who used to ring in to buy BHP because its a good company. Each of these arms generates a very different revenue stream for the firm, corporate advice generates fees in the millions whereas retail advice might involve an order that generates $6 in brokerage. You can see where the massive imbalance in revenue comes from and therefore you can see which side of the firm is more important. Consider a simple example, I head off to my local merchant bank/broker and I want to list my company to liberate some of the value in it and this listing will generate for the firm $5 million in fees. Naturally, if I want to list my company I need shareholders so it is the job of the retail arm to go a get them for me via selling the prospectus to them and after that via selling it to new punters via the secondary market. In terms of importance I am immensely important and my needs come first because I have given the firm $5 million, a retail investor doesn’t even give them enough for a slab of beer.

Underlying all of this is the simple need of stockbrokers to eat – stockbroking at its heart is a sales profession. If I dont sell you a second hand good in the form of a share then I dont eat. Even better if I can get you to sell one stock you own for another because then I get two lots of commission. You might think that with the advent of online trading that this situation might have evolved and changed because technology has removed the need to actually talk to someone. In some ways it has but it has also shown a new flaw in the advice model and that is in the recommendations that are generated by broking firms. If we think logically about markets then you would assume that markets are comprised of a mass of differing stocks, some doing well and going up, some doing poorly and going down and others doing nothing in particular. This is not how the industry sees markets – to them every single stock is a buy. Consider the table below which I generated a few years ago.

This chart looks at the ratio of buy to sell recommendations being offered by brokers. The lowest the ratio got was in 1983 when the industry were net sellers – this coincided with the beginning of the 1980’s bull market. Since then the industry has always been net buyers and the latest figures I could find indicate that the buy to sell ratio sits at around 100 to 1. It doesn’t seem logical that for every stock that is a buy there could only be one that is a sell. The industry is overwhelmingly biased towards the buy side.

In looking into the industry over the years the best explanation for the behaviour of its members can be found in the following quote –

“An investor might expect advice that is free of both psychological bias and self interest. Instead they discover belatedly that the advice is a mixture of wishful thinking and self- serving hype.”

Brian Bruce Journal of Psychology and Financial Markets (2002 Vol 3, No4, 198-201)

As the question as to how to navigate all of this the answer is really quite simple – do your own thinking. If you want to be subject to the whims of others then that is fine but just remember this is an industry that had to be dragged kicking and screaming into acting in the best interests of their clients.